Aequs Ltd

India's Aerospace Factory, With a Consumer Electronics Bet That Could Change Everything

Before we begin - quick update on new features we launched at Growth Triggers.

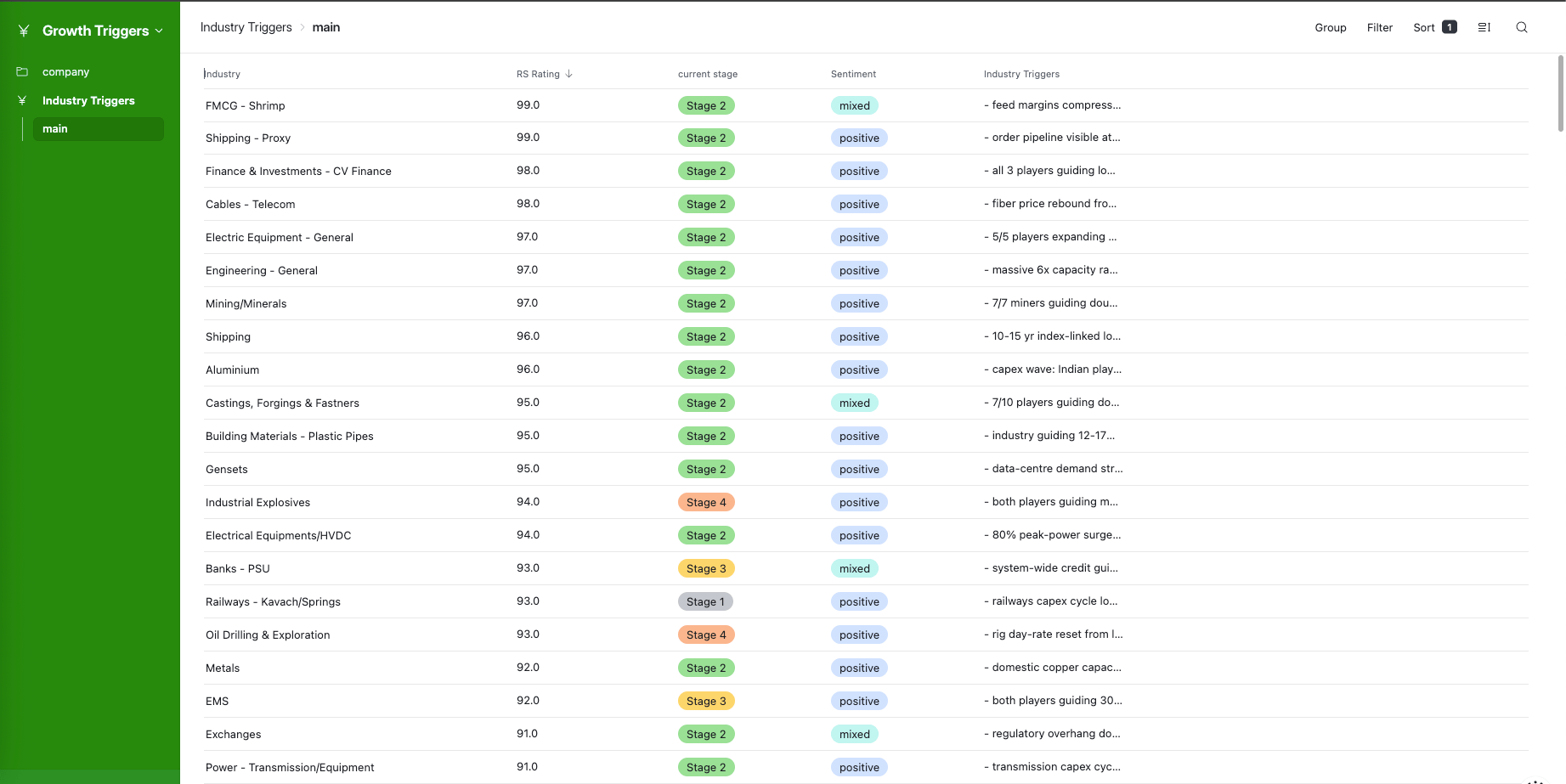

Industry Triggers (revamped)

We completely rebuilt the industry analysis from scratch. Every industry now has its own triggers pulled from the latest concalls of all companies in that sector. Instead of generic sector commentary, you get specific, numbers-backed catalysts driving each industry right now. 253 industries covered, each with sentiment ratings (bullish/bearish/mixed), RS rankings, and dominant stage analysis.

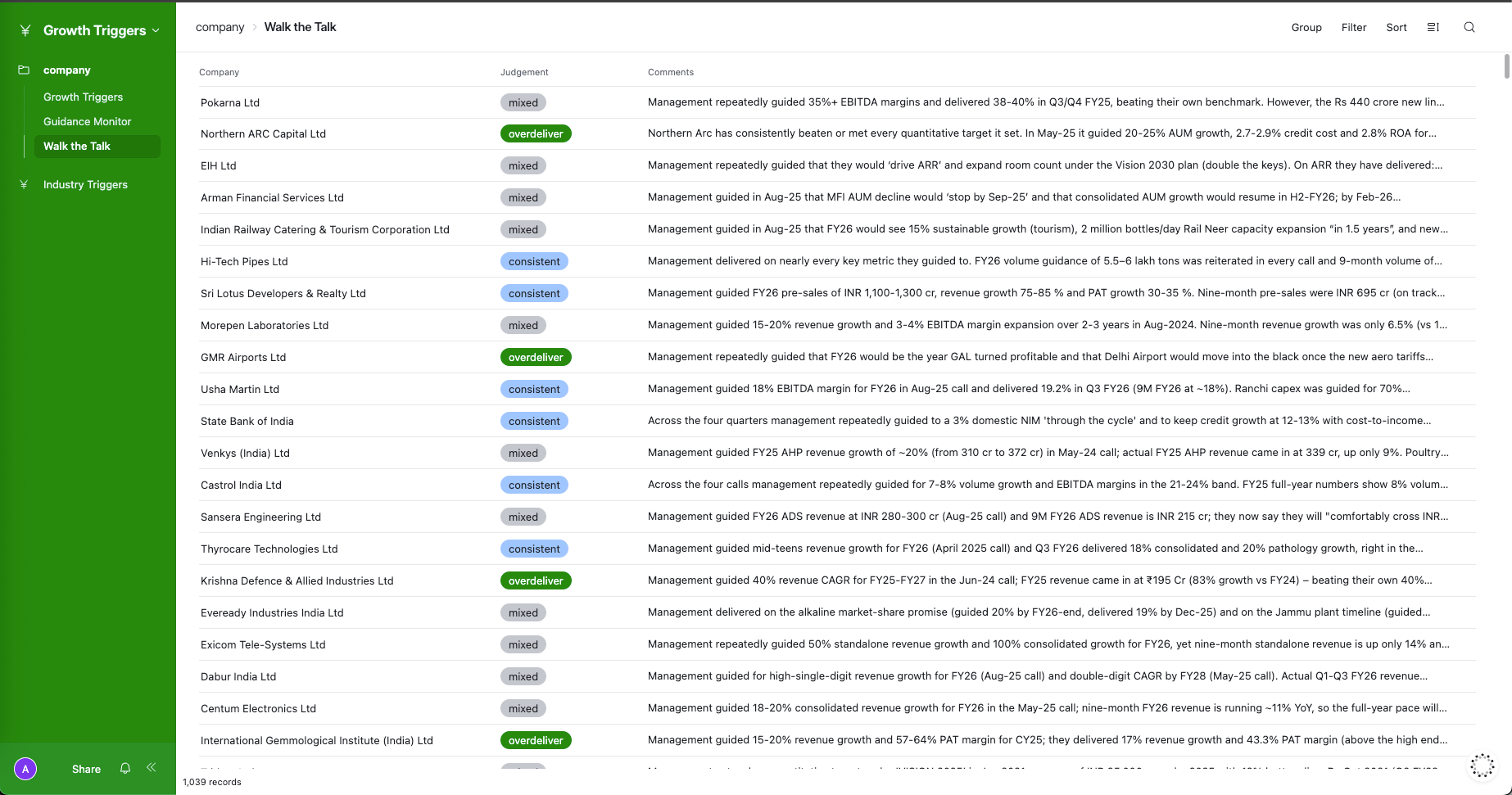

Walk the Talk (Management Consistency)

This one’s our favourite. Agents read all 4 quarters of concall transcripts for each company and check: did management actually deliver on what they promised? Every company gets rated as one of four categories:

Overdeliver - consistently beat their own guidance

Consistent - did what they said they’d do

Mixed - hit some targets, missed others

Hype Man - big promises, weak delivery

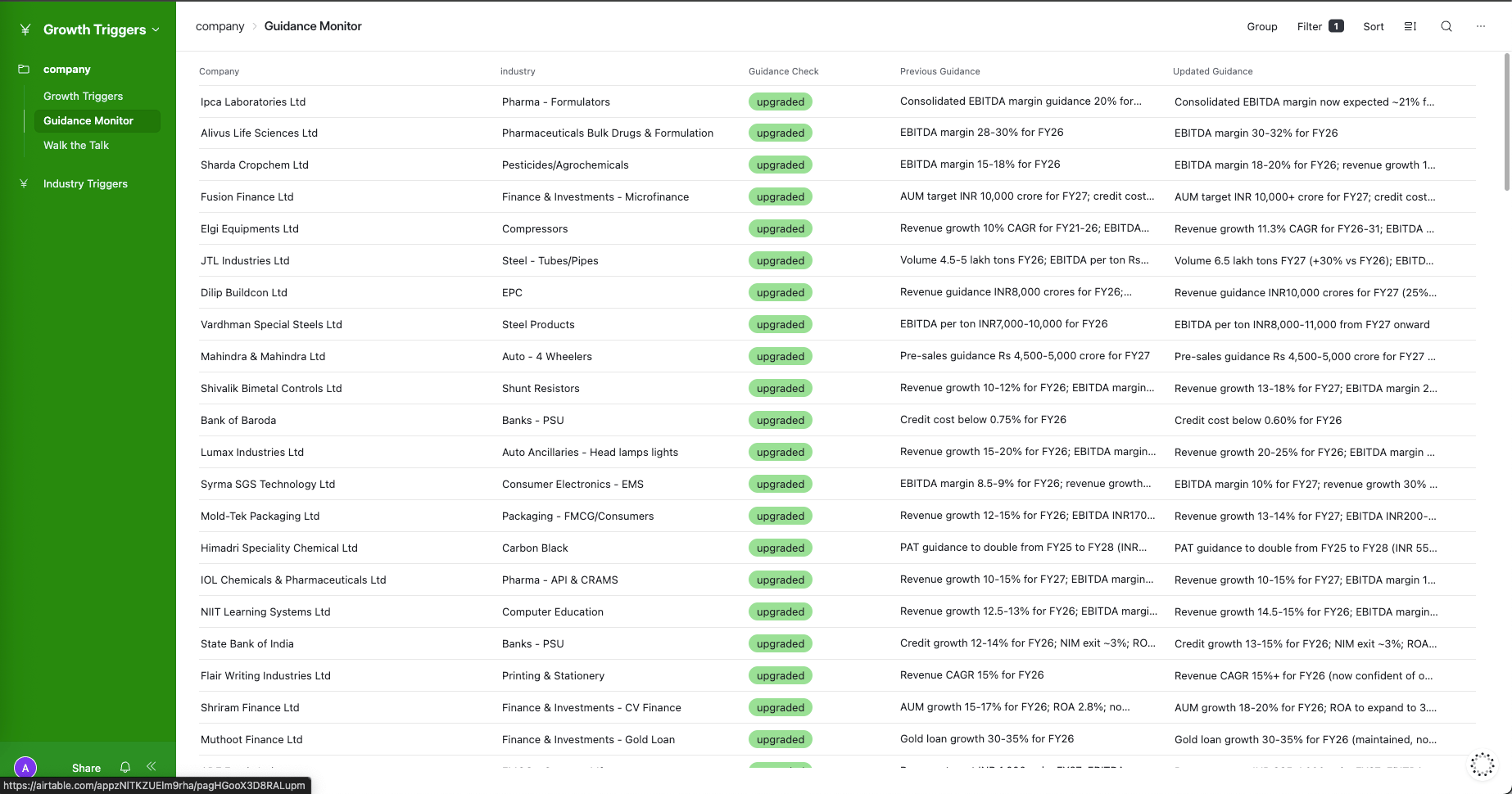

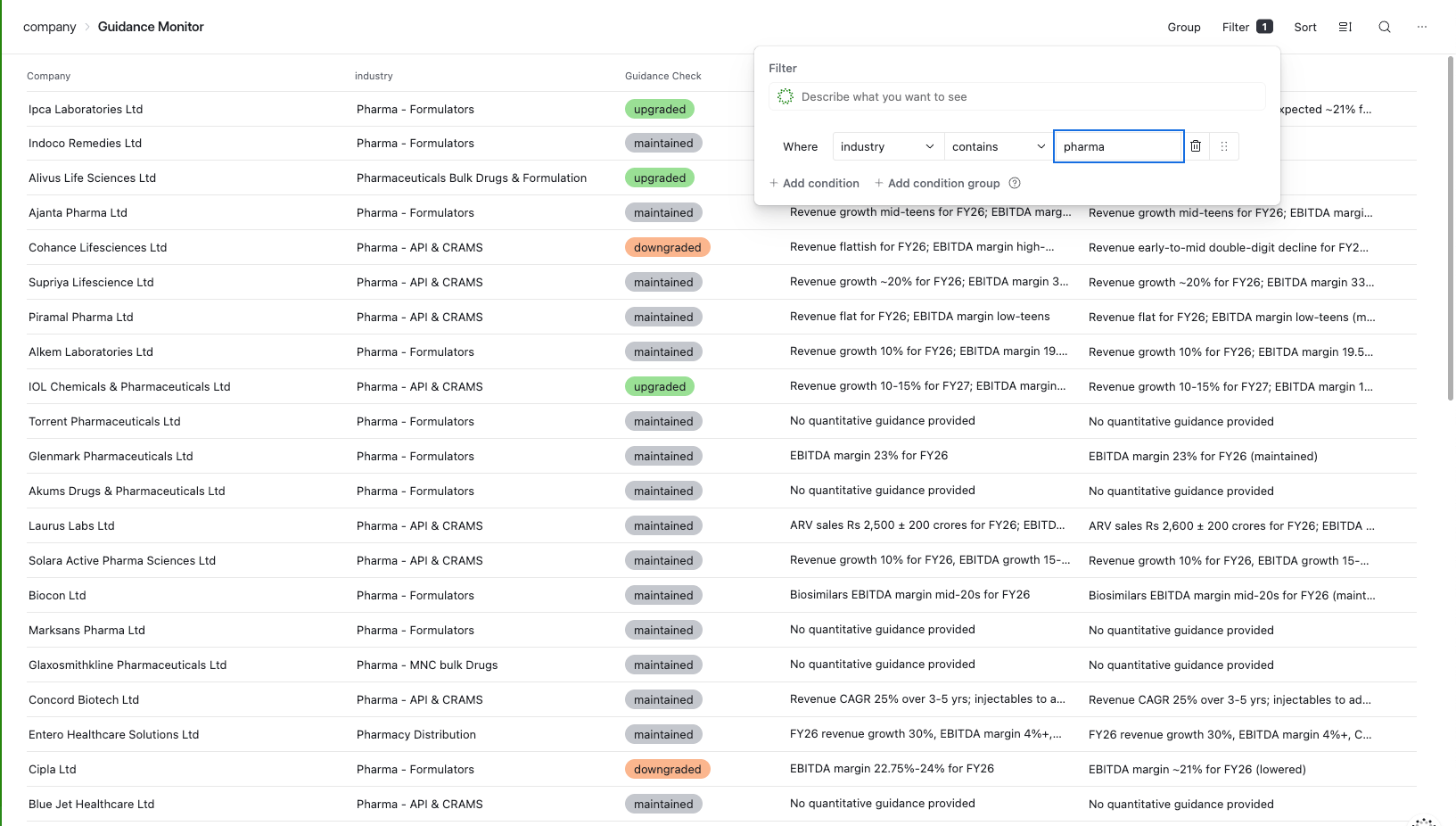

Guidance Monitor

We now track whether management upgraded, maintained, or downgraded their forward guidance compared to previous quarters. You can see both the old and new guidance side by side.

You can now filter for companies upgrading their guidance and go one level deeper to scan for industries with the most guidance upgrades.

Aequs is a precision components manufacturer. It takes raw aluminium, titanium, and steel, and turns them into flight critical parts for Airbus, Boeing, and Safran. It also makes plastic toys for Hasbro, cookware for Tramontina, and (more recently) smart device casings for a global consumer electronics giant widely reported to be Apple.

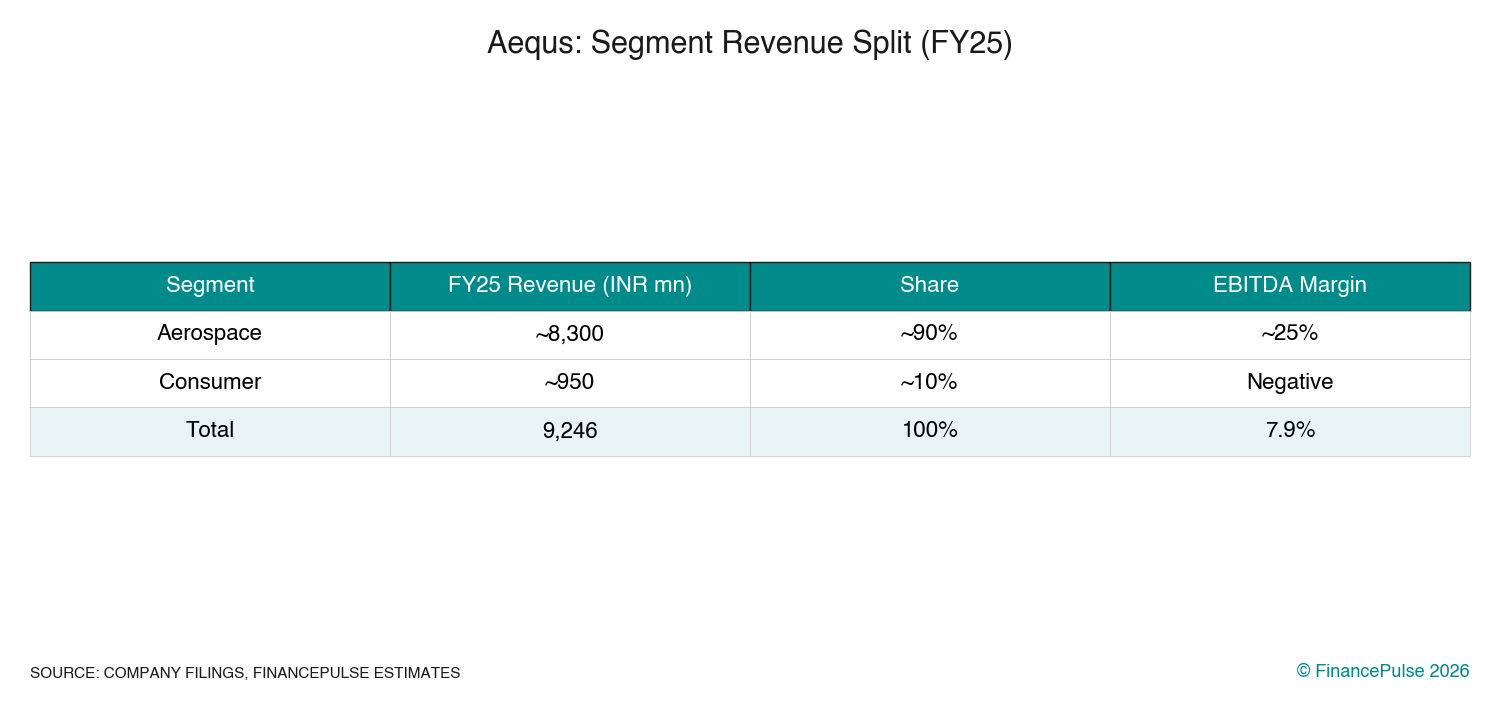

Aequs operates across two segments:

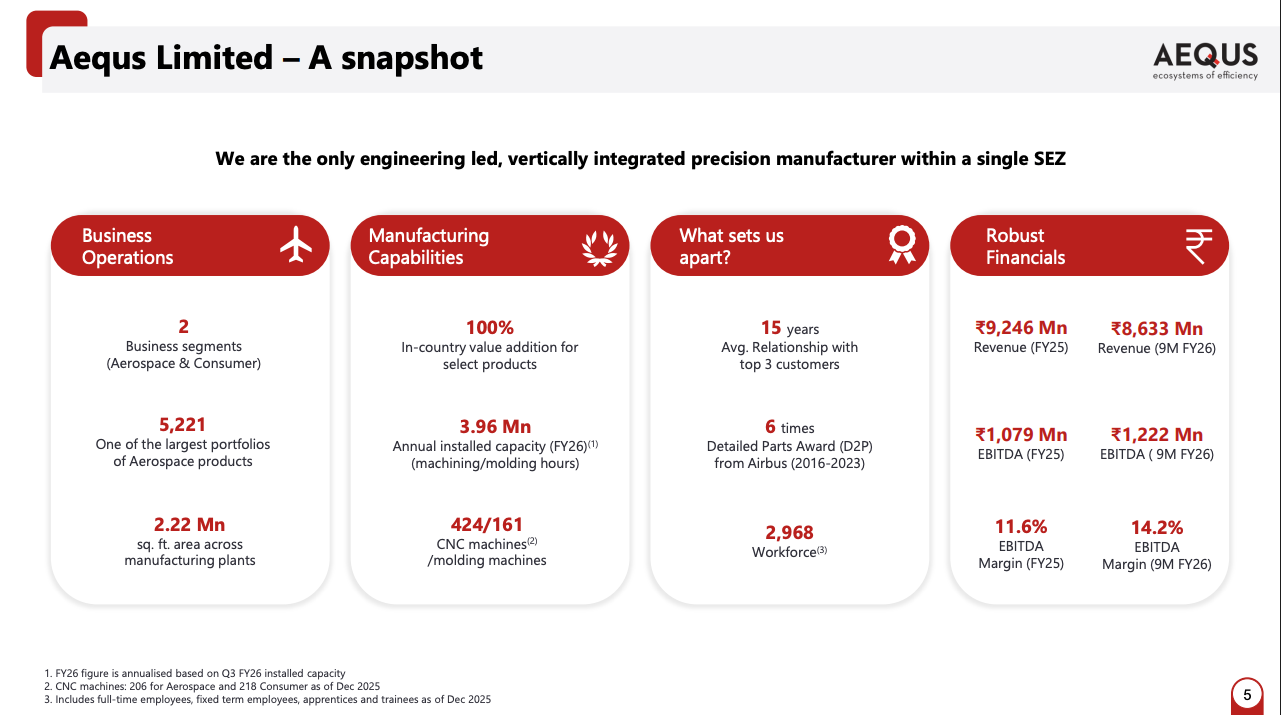

The company was founded in 2000 by Aravind Melligeri, a mechanical engineer from Mangalore University with a master’s from Penn State. He built India’s first precision engineering SEZ in Belagavi, attracted Airbus as a customer, and spent 15 years turning the company into a Tier I supplier for every major aerospace OEM. The IPO in December 2025 raised INR 922 crore through a fresh issue at INR 124 per share.

The Belagavi SEZ: A Factory Within a Factory

The core of Aequs is a 250+ acre Special Economic Zone in Belagavi, Karnataka. Within this single campus, a titanium billet arrives and exits as a finished, surface-treated, assembled aircraft component.

The manufacturing chain inside the SEZ runs in sequence:

Raw material intake (aluminium from Thyssen Krupp in Germany, Hindalco domestically; titanium alloys from European suppliers) -> Forging (SQuAD JV, 10,000-ton hydraulic press) -> Precision machining (420+ CNC machines) -> Surface treatment (API JV with Magellan Aerospace, NADCAP certified) -> Assembly (aerostructures, door panels) -> Finished goods and delivery (air cargo to customers in France, USA, Vietnam)

The distance components travel within the SEZ is under 500 meters. Without this integration, parts would travel 5,000+ km between forging, machining, and surface treatment facilities across multiple countries. That logistical compression is the core competitive advantage.

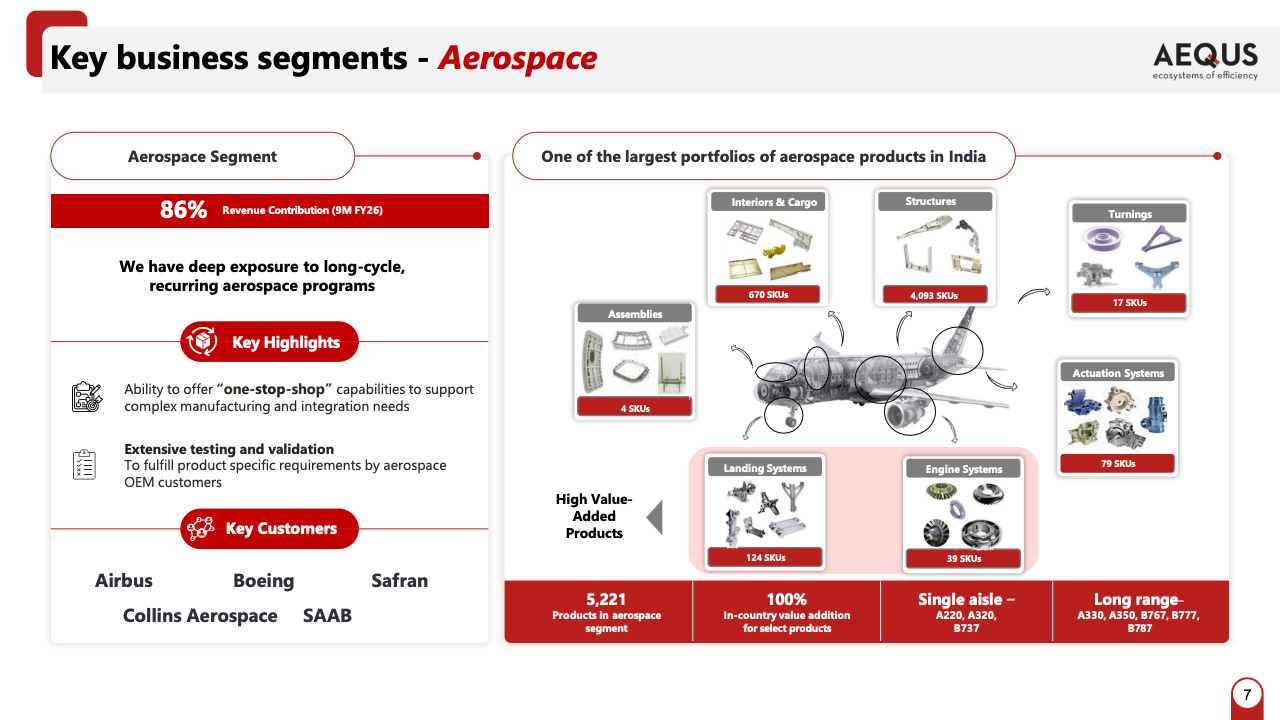

Aerospace Segment

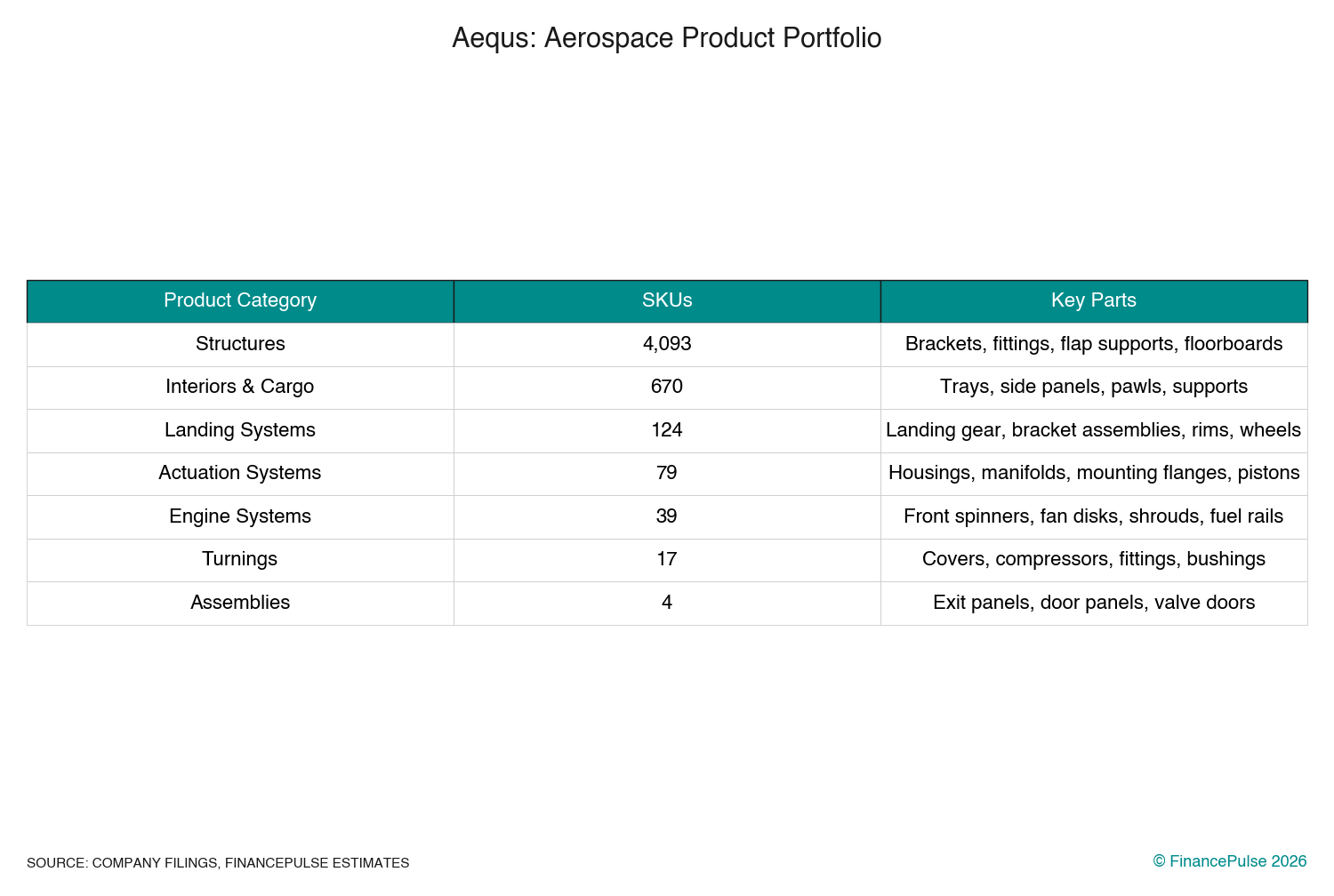

Aequs manufactures 5,200+ distinct aerospace part numbers as of 9MFY26, up from 4,500+ at end-FY25. The product portfolio breaks down as follows:

The high value items are engine systems and landing systems. An engine front spinner (a rotating component mounted on the front of a turbine blade assembly for the LEAP engine) carries more revenue per unit than a standard structural bracket. Aequs has achieved 100% in-country value addition for select products like front spinners and landing system wheels. That means no step in the manufacturing process leaves India.

Aequs supplies parts for both single-aisle aircraft (A220, A320, B737) and long-range aircraft (A330, A350, B767, B777, B787). The mix matters. Single-aisle production rates are far higher (Airbus targets 75 A320s per month by 2027), which drives volume. Long-range parts tend to be larger and more complex, carrying higher unit values.

Key Customers

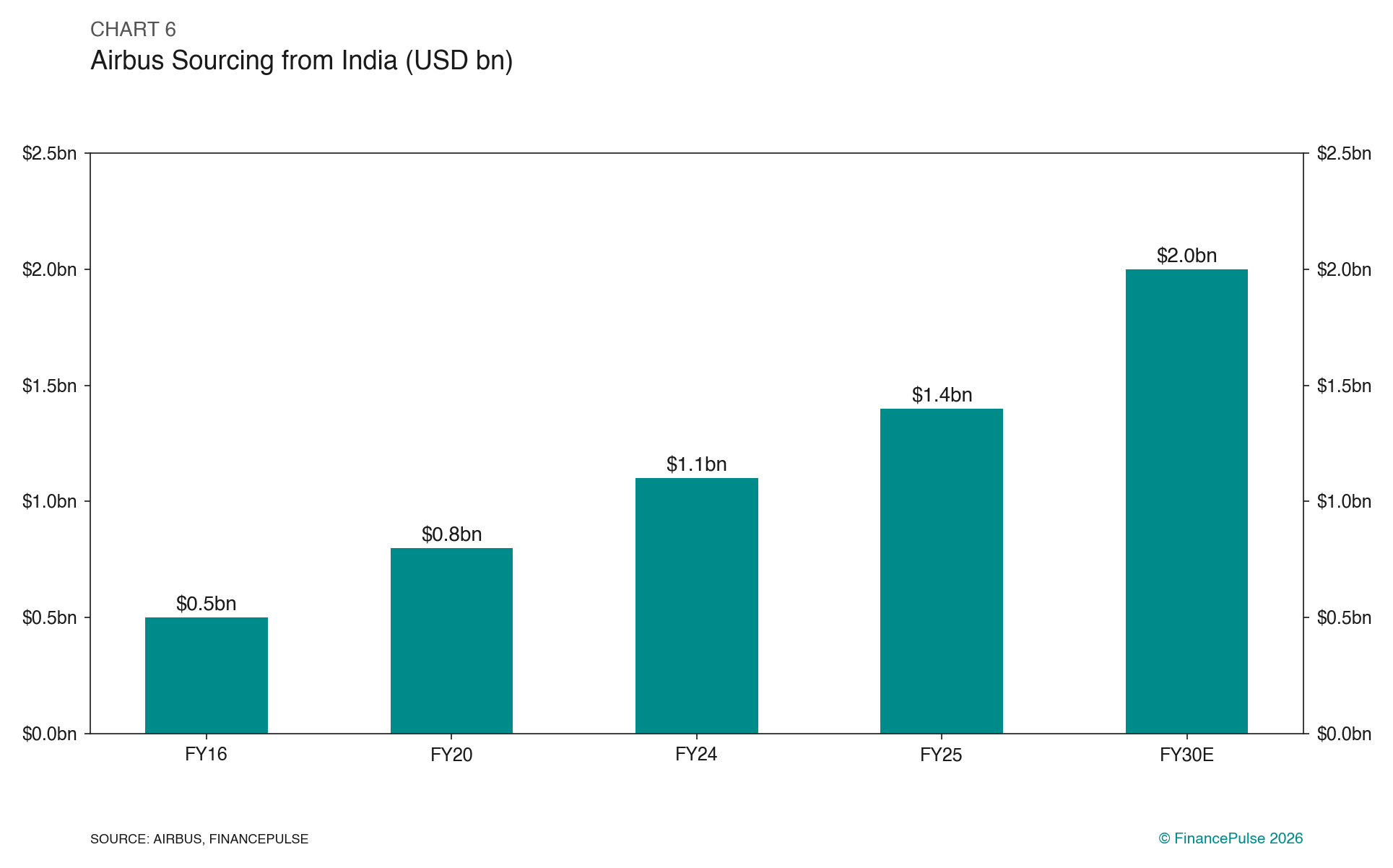

Airbus is the largest customer. The relationship is 15 years old. Aequs holds D2P (Detailed to Parts) status, awarded to only the top 100 suppliers globally. Aequs has won this award six times between FY16 and FY23. It has also received Airbus’s Ramp-up Champion award and SQIP (Supplier Quality Improvement Process) awards. Airbus increased its India sourcing from USD 0.5bn in FY16 to USD 1.4bn in FY25 and plans to reach USD 2.0bn by FY30. Aequs is one of the primary beneficiaries of this shift.

Boeing has been a customer for eight years. Aequs has been a Tier I supplier since 2017. Boeing’s India sourcing stands at USD 1.25bn annually from 300+ suppliers and the company plans to roughly double this figure. The India-US trade pact removing tariffs on aircraft parts accelerates this trend.

Safran has been a customer for nine years. Aequs supplies engine-related components. Safran is the third-largest aerospace customer by revenue contribution.

Collins Aerospace has been a customer for 10 years. Aequs services Collins from its facility in Cholet, France.

Other customers include Spirit AeroSystems, Honeywell Aerospace, Dassault Aviation, GKN-Fokker, Bombardier, EATON, Premium AEROTEC, and SABCA.

Order Book

The aerospace order book stood at USD 814mn as of 9MFY26. At an average annual execution rate of USD 200mn+, this provides roughly 3-4 years of revenue visibility extending to about 2031. The order book is growing as Aequs wins additional programme share from Airbus and Boeing.

Three factors driving aerospace growth for Aequs: Airbus/Boeing increasing India sourcing, Aequs gaining wallet share within existing customers, and the product mix shifting toward higher-value landing systems and engine components.

Key Joint Ventures

SQuAD Forging India Pvt Ltd (JV with Aubert & Duval, France): Forges small to medium-sized aero-structural parts for engines, landing gear, and braking system components. Works with aluminium, steel, titanium, and nickel-based alloys. The JV operates a 1,200-ton screw press and a 10,000-ton hydraulic close die-press. Holds ISO 9001, AS9100, ISO 14001, and OHSAS 18001 certifications. Heat treatment lines are NADCAP certified.

Aerospace Processing India (API) (JV with Magellan Aerospace, Canada): Provides surface treatment solutions including chemical processing, surface enhancement, and non-destructive testing. First unit in India to achieve NADCAP accreditation across all three disciplines. API is the approved surface treatment facility for Boeing and Airbus. Magellan and Aequs recently announced a sand casting JV as well, expanding capabilities further. An MRO (Maintenance, Repair, and Overhaul) facility is under development in partnership with Magellan, planned for completion in 2025.

Aerostructures Assemblies India (AAI) (JV with Saab AB, Sweden): Specializes in build-to-print assemblies for commercial and defense aircraft. Aequs is the first Indian company to assemble plug doors and over-wing exit doors for Airbus and Boeing. The JV is positioned to capture defense offset opportunities.

International Facilities

Cholet, France (acquired 2016 via SIRA Group): Services Collins Aerospace and Safran. Proximity to European OEMs reduces lead times and deepens customer relationships.

Texas, USA (facility established 2015): Services Boeing and Spirit AeroSystems. Approved for exports. Provides a North American delivery point for US-based customers.

Both facilities give Aequs on-the-ground presence near customer engineering teams, which helps win new programme qualifications.

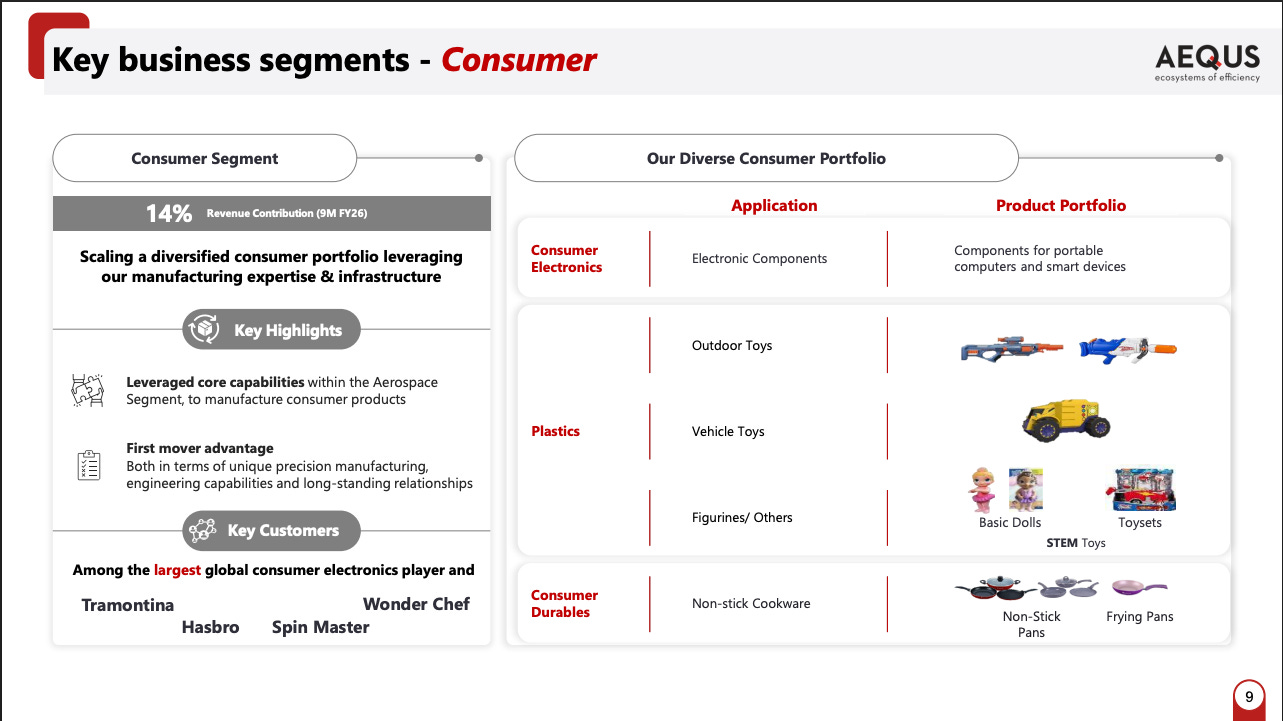

Consumer Segment: The Three Verticals

The consumer segment has three distinct product lines:

1. Consumer Electronics (the new growth driver)

Aequs has secured orders from a global consumer electronics major for manufacturing smart watch enclosures and laptop bottom casings. Media reports (Swarajya Mag, among others) have identified this customer as Apple. The parts are precision-machined in India at Aequs’s Hubballi facility (0.30mn sqft dedicated to high-precision consumer products) and then flown to Vietnam for final assembly by the customer’s existing vendors.

Production of laptop components commenced on July 31, 2025. Aequs has deployed 218 CNC machines specifically for consumer electronics as of 9MFY26. Utilisation has climbed from 19% in 3QFY25 to 31% in 3QFY26. Despatches to Vietnam are ongoing.

The customer reportedly has plans to expand production in Vietnam for smart devices. The manufacturing capacities Aequs will eventually set up in Karnataka are contingent on the customer’s demand projections. The products (mechanical enclosures) qualify for government PLI incentives, which can support margins.

This is the part of the business that draws comparisons to Luxshare in China. Luxshare grew from CNY 35.9bn in revenue in 2018 to CNY 268.8bn in 2024, a 40% CAGR, by scaling machining capabilities for a single dominant consumer electronics customer. Its EBITDA margins settled at 8-9% at scale, with ROCE above 12%. If Aequs can replicate even a fraction of that trajectory, the consumer segment alone could generate INR 10,000-15,000mn in revenue by FY30.

2. Plastics (Toys)

Aequs began making plastic toys at the Belagavi SEZ in FY16. The customer base includes Hasbro (nine-year relationship, the longest), Mattel (shipments began from 3QFY26), Spin Master (five years), and others. Products include outdoor games, darts, toy vehicles, figures, dolls, role-play toys, and STEM toys.

The toy business is seasonal, peaking in Q3 (October-December, ahead of the global holiday season). It has been volatile. FY25 saw particularly sharp swings in sales and margins. Hasbro had a product recall in FY21 due to high lead content (partly covered by insurance), though there have been no recalls in the last three years.

Manufacturing facilities for toys are at Belagavi and Koppal (0.30mn sqft). The company operates 161 plastic moulding machines (80-450T capacity), 7 blow moulding machines, and 46 assembly lines. Mattel recently closed its factory in China and is relocating manufacturing to India and Vietnam, a trend that benefits Aequs. Hasbro is also sourcing more from India as part of the broader China-plus-one supply chain shift.

3. Consumer Durables (Cookware and Appliances)

Aequs manufactures non-stick cookware and small home appliances. The key relationship is a joint venture with Tramontina, the Brazilian cookware giant with 113 years of history. This is Tramontina’s only manufacturing facility outside the Americas. The JV was formalized in June 2024.

Wonderchef has been a customer for seven years. Other customers include Borosil and Playshifu. The consumer durables business is small relative to the other two verticals and contributes modestly to segment revenue.

Consumer Segment: The Scale Challenge

The consumer segment’s core problem is under-absorption of fixed costs. At 31% utilisation (9MFY26), the segment generates negative EBITDA. Every CNC machine, every assembly line, every worker on the floor costs money whether or not parts are being machined. The EBITDA loss in consumer widened from INR 95mn to INR 159mn in Q3 FY26 even as revenue grew 157% YoY, because Aequs is still investing in start-up costs for the electronics ramp.

The capex required is large. Aequs will need to keep adding CNC machines for electronics, moulding machines for toys, and capacity for cookware.

Workforce

Aequs employs roughly 4,000+ people across its facilities. The company planned to add 1,000 employees by March 2026, including 300-400 in aerospace. A team of 300+ engineers (process, tools, and testing specialists) handles new product development, receiving customer technical specifications and simulating and industrializing products. This engineering bench is a competitive moat. Qualifying new aerospace parts takes 12-18 months of testing and certification. Once qualified, switching costs for the customer are high.

Karnataka Expansion

In March 2026, Aequs signed a non-binding MOU with the Government of Karnataka to invest INR 2,856 crore over five years starting FY26. The expansion focuses on Belagavi and Hubballi, strengthening both aerospace and consumer manufacturing capacity. This is separate from the ongoing capex for CNC machine additions and represents a longer-term commitment to the state.

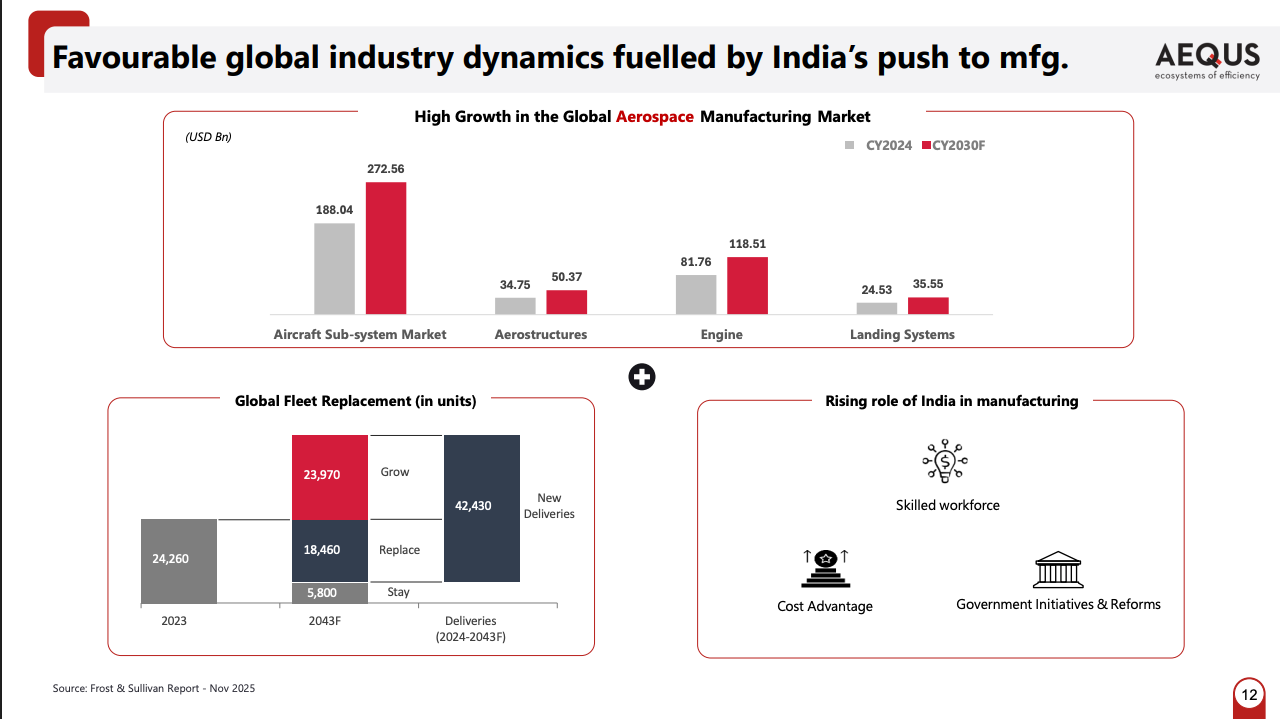

Global Aerospace Supply Chain: The India Shift

The global aerospace supply chain is rebalancing toward India. Two forces drive this.

First, production rate increases. Airbus plans to produce 75 A320 neo-family aircraft per month by 2027, up from roughly 50 in 2024. Boeing is ramping the 737 MAX toward 38/month. Every additional aircraft per month requires proportionally more parts from the supply chain. OEMs need suppliers who can scale.

Second, supply chain diversification. COVID and the subsequent recovery exposed concentration risk in the aerospace supply chain. European and North American Tier II/III suppliers struggled with labor shortages, inflation, and raw material availability. India offers lower labor costs (roughly 60-70% cheaper than France or the US for equivalent machining work), a growing pool of engineering talent, and government incentives through the SEZ framework.

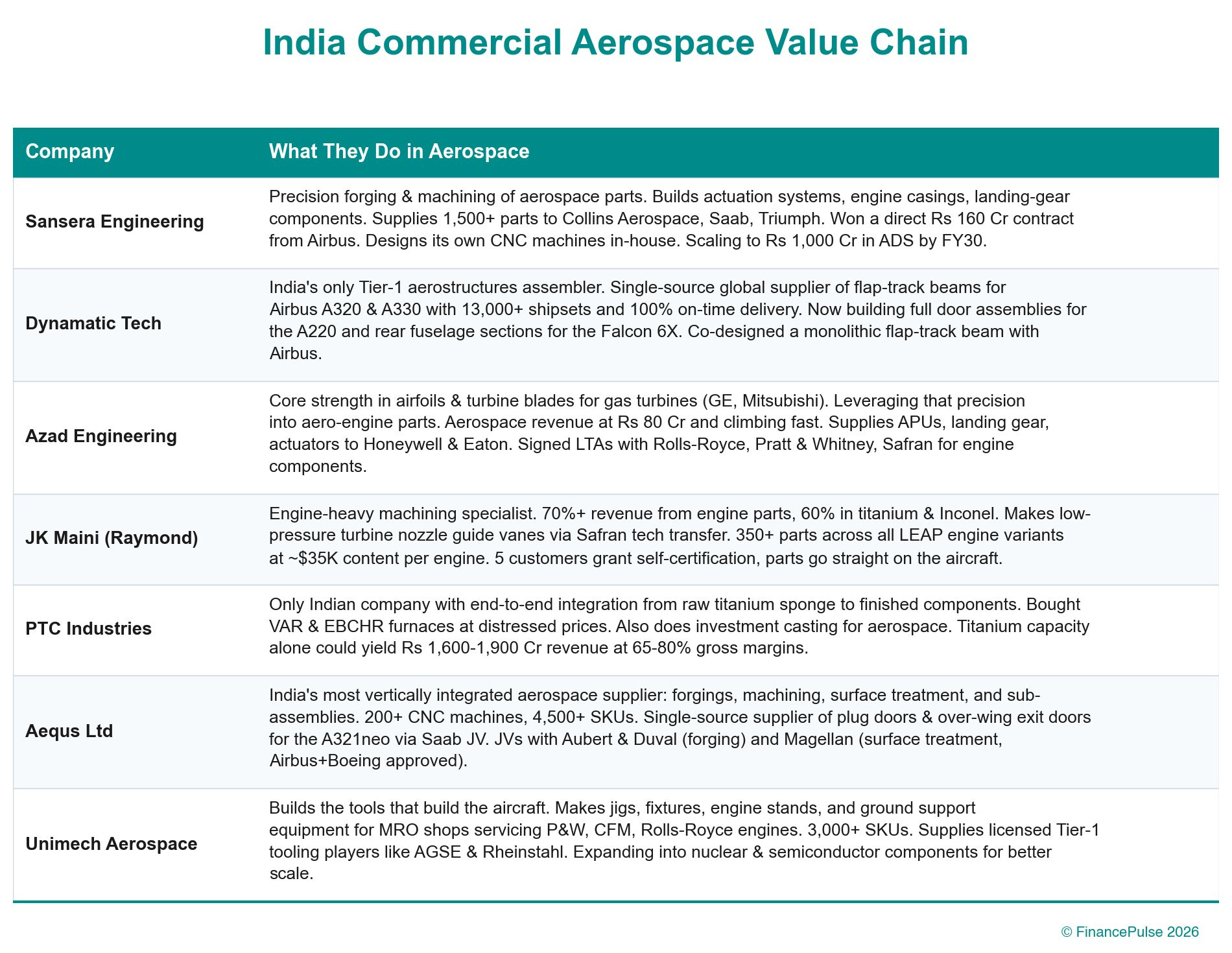

The Competitive Set in India

Aequs competes with a growing set of Indian aerospace manufacturers:

Competition is increasing, however. Airbus expanded its India vendor pool from 45 suppliers in FY16 to 100+ by FY24. Boeing sources from 300+ suppliers. New entrants are qualifying. Pricing pressure exists through annual price-reduction initiatives that OEMs impose on suppliers.

Consumer Electronics: The China-Plus-One Opportunity

The consumer electronics manufacturing shift from China is accelerating. Apple targets sourcing 20% of global iPads and Apple Watches, 5% of MacBooks, and 65% of AirPods from Vietnam. India is gaining share as well, with Apple planning to manufacture 50mn iPhones in India.

The precision machining segment within consumer electronics (casings, enclosures, structural components) carries higher margins than assembly. Foxconn and Pegatron do assembly. Luxshare and (potentially) Aequs do machining. The machining step requires expensive CNC equipment, tight tolerances, and quality systems. This naturally limits the competitor set.

Luxshare’s trajectory in China provides a reference point. Revenue grew from CNY 35.9bn (2018) to CNY 268.8bn (2024). EBITDA margins settled at 8-9% at scale. ROCE stabilized above 12%. The company was capex-intensive for years before turning consistently free cash flow positive. Aequs is at the very beginning of what could be a similar curve, but at much smaller scale and with execution risk that Luxshare, already deeply embedded in the supply chain, did not face.

Aerospace Growth Drivers

Wallet share gains with Airbus: Aequs currently supplies 5,200+ parts. The total addressable part count on Airbus programmes is many multiples of that.

Boeing ramp: Boeing’s India sourcing at USD 1.25bn is set to double. Aequs’s Tier I status and Texas facility position it to capture incremental share.

Product mix enrichment: The shift toward landing systems (124 SKUs) and engine systems (39 SKUs) carries higher unit values than structural brackets (4,093 SKUs). As Aequs wins more high-value programmes, revenue per part should rise.

MRO entry: The planned MRO facility with Magellan Aerospace adds a new revenue stream. India’s MRO market is expanding as the domestic fleet grows (1,000+ commercial aircraft on order from Airbus and Boeing combined for Indian carriers).

Consumer Growth Drivers

Electronics scale-up: The consumer electronics contract is the single largest growth lever in the business. If utilisation climbs from 31% to 70%+ by FY29-30, consumer electronics alone could generate INR 8,000-10,000mn in revenue.

Toy manufacturing shift from China: Mattel closed its China factory and is relocating production to India and Vietnam. Hasbro is also increasing India sourcing. Aequs’s existing relationships (Hasbro for nine years, new Mattel relationship from 3QFY26) position it to capture this shift.

Tramontina JV scale-up: Tramontina’s only facility outside the Americas is with Aequs. As the JV ramps, cookware exports could grow.

Key Risks

1. Consumer electronics ramp-up is the swing factor, and it’s binary. If the global electronics customer scales orders as expected, consumer revenue could reach INR 10,000mn+ by FY30 with positive EBITDA. If orders stall or the customer shifts to alternate suppliers, Aequs has deployed 218 CNC machines (at roughly INR 15-20mn each) with no revenue to absorb the depreciation. Industry commentary draws parallels with Luxshare, but Luxshare was already deep in Apple’s supply chain when it scaled. Aequs is at trial/early production stage.

2. The company will burn cash for years. Capex of INR 450-550cr annually, negative free cash flow, and rising debt are the near-term reality. If the consumer ramp is slower than expected, debt/equity could breach 1.5x by FY29. At some point, the balance sheet constrains growth.

3. Aerospace competition is intensifying. Airbus expanded its India supplier base from 45 to 100+ between FY16 and FY24. Boeing sources from 300+ Indian suppliers. New entrants like Azad Engineering, Unimech Aerospace, and PTC Industries are qualifying for programmes. While Aequs’s integrated capability and D2P status are difficult to replicate, OEMs actively pursue price reductions from existing suppliers.

4. Customer concentration. Airbus is the largest customer by a wide margin. Any disruption to Airbus’s production plans (supply chain delays, regulatory issues, demand slowdown) would flow directly through to Aequs’s revenue.

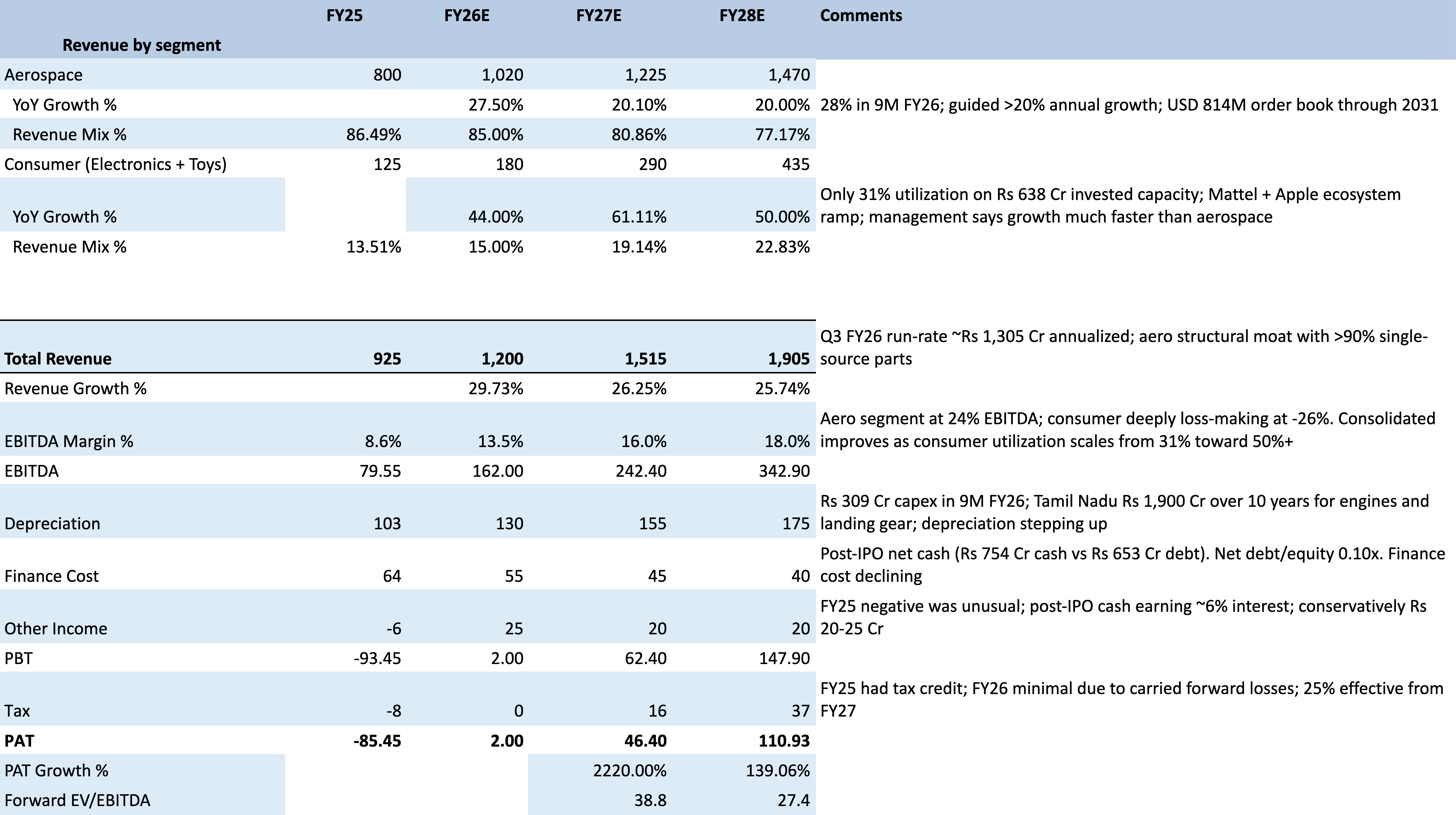

Valuation

TLDR on Aequs

Only precision component manufacturer in India with fully vertically integrated aerospace ecosystem within a single SEZ

Over 90% single-source (sole supplier) parts in aerospace - strong competitive moat with 5-7 year contracts

USD 814M aerospace order book (TCV) through 2031, continuously replenished via RFP pipeline

aerospace segment EBITDA margin at 24%, sustainable at 20%+ per management - well above consolidated due to consumer drag

consumer electronics capacity (Apple ecosystem + Mattel + Tramontina) at only 31% utilization on Rs 638 Cr invested - massive operating leverage as volumes ramp

Tamil Nadu MoU for Rs 1,900 Cr over 10 years targeting higher-value landing gear, engine, and systems components - move up aerospace value chain

SQuAD JV with Aubert & Duval for 10,000 ton hydraulic closed-die forging press - unique forging capability in India for aerospace

post-IPO net cash balance sheet (net debt/equity 0.10x) provides runway for capacity expansion without dilution

India currently only 2% of global aerospace supply chain vs 10% target - structural tailwind for domestic precision manufacturers

Airbus D2P (Direct-to-Partner) status since 2016 - preferential access to new contract opportunities

expanding from aerostructures into higher-margin engine and landing gear systems - content per aircraft increasing

defense UAV JV with Accel India and Vagus Defense for indigenous drone manufacturing - India defense budget capex up 30% for FY27

management targeting long-term 50:50 balance between aerospace and consumer revenue - consumer at only 14% currently

Awesome report