KSH International

India's only approved wire for 400kV HVDC transformers.

Before we begin - check out Growth Triggers & for more of me follow on X (Twitter)

KSH international makes the wire that sits inside almost every large electrical machine in india. When a power transformer steps up voltage to transmit electricity across the country, or a traction motor pulls a locomotive, or an alternator generates power inside a wind turbine, there is winding wire at the core - copper or aluminium conductor, precisely insulated, wound thousands of times into a coil that creates the electromagnetic field that makes the machine work. KSH makes that wire.

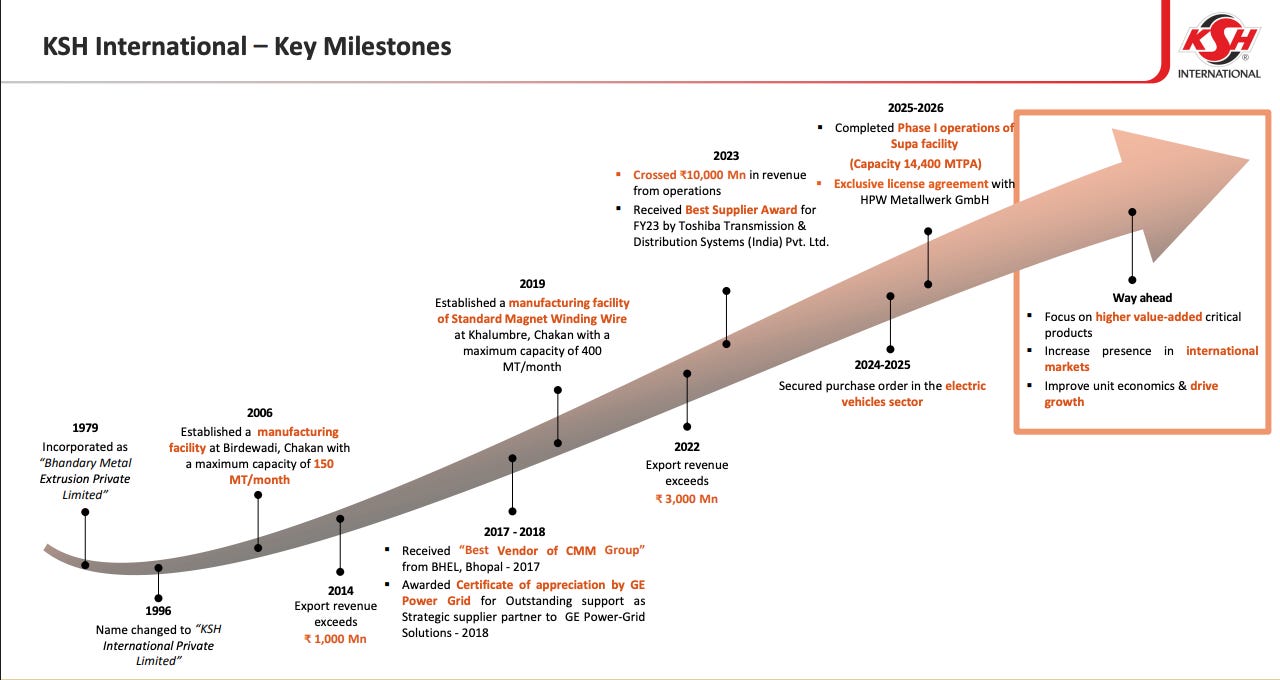

The company was originally incorporated in 1979 as bhandary metal extrusion private limited in maharashtra. it began commercial operations in 1981 at taloja in raigad district, manufacturing the most basic form of magnet winding wire - paper insulated rectangular copper conductors - for transformer makers. For the next two decades the business was privately held and relatively modest. The pivot that defines the company today happened in 2006, when ksh pioneered the indigenisation of continuously transposed conductors (ctc) in india. CTC is a high-complexity, high-value product used inside large power transformers, and until ksh built the capability, india’s transformer manufacturers depended on imports. This decision to move upstream in complexity was the defining strategic bet of the company’s history, and it is the source of most of what distinguishes ksh from standard wire manufacturers today.

The company was renamed ksh international in 1996, a reflection of its growing export ambitions. By fiscal 2025 it had become the largest exporter of magnet winding wires from india by export revenue, according to care ratings. It listed on the nse and bse on december 23, 2025, via a rs 626 crore ipo.

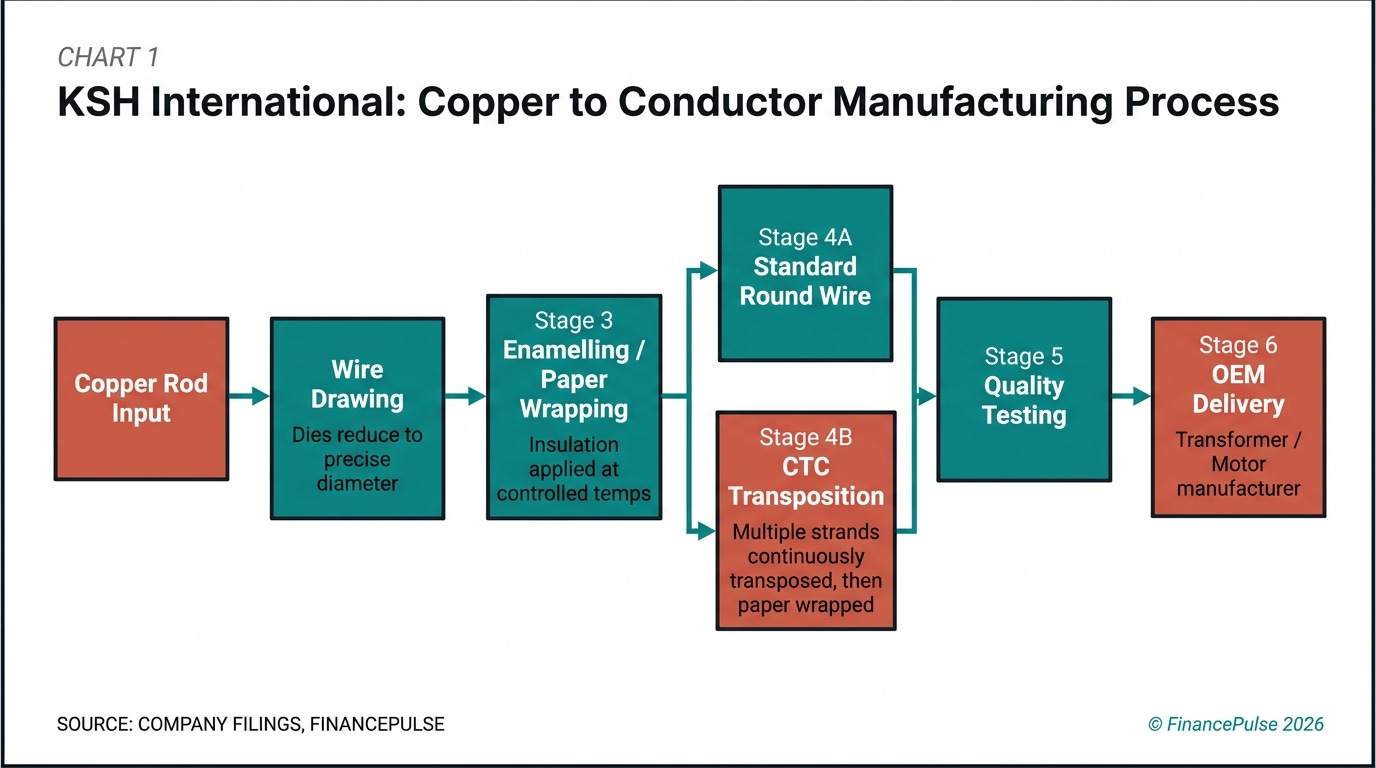

The business model goes like: ksh buys copper rod and aluminium rod as raw materials, draws them down to precise dimensions, applies insulation layers - enamel coating, paper wrapping, or complex transposition - and sells the finished conductor to OEM customers who wind it into their electrical equipment. The margin profile depends almost entirely on how complex the insulation and processing is, not on the metal itself. Copper prices are passed through to customers, and the per-ton economics that management tracks - ebitda per metric ton - is the real measure of whether the business is improving.

What ksh actually does, in a technical sense, is manage the gap between raw copper and a precisely engineered conductor. A standard round enamelled wire involves drawing copper rod through progressively smaller dies and coating it with enamel at controlled temperatures. a continuously transposed conductor involves assembling multiple individually enamelled rectangular strands, transposing them continuously through a mechanical process so each strand occupies every possible position in the bundle, then wrapping the bundle in paper tape. The transposition eliminates circulating currents in large transformer windings, reducing electrical losses. Getting the transposition geometry right, consistent across thousands of meters per production run, requires process control that took ksh nearly two decades to develop. The company can currently produce ctc strands from 5 to 47 in number, in widths from 3 to 12.5mm and thickness from 1.1 to 3.2mm, with up to 24 layers of paper insulation. No other manufacturer in india matches this specification range in ctc.

The customer problem ksh solves is simple to state but hard to serve: oems building power transformers, generators, and electric motors cannot buy off-the-shelf wire. Every winding requires a precise conductor cross-section, insulation specification, and mechanical tolerance. ksh custom-engineers each order to the customer’s drawing. this is not commodity distribution - it is engineered manufacturing to specification on a per-order basis, which is why the company has managed over 90% repeat customer revenue.

Business Segments

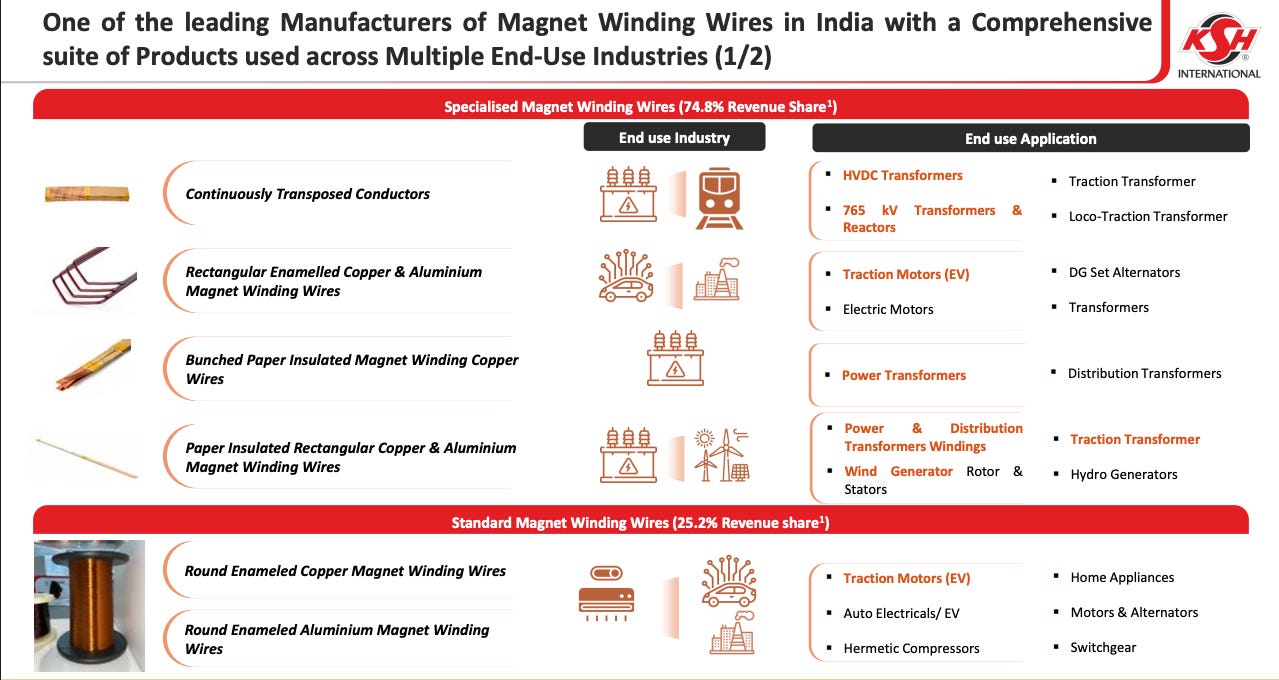

Specialized Winding Wires

Specialized wires contributed approximately 75% of ksh’s total revenue in q3 fy26, growing 61% year-on-year in that quarter. This is the higher-complexity, higher-margin half of the portfolio, and it is what distinguishes ksh from commodity wire producers.

Specialized wires consist of continuously transposed conductors (ctc), paper-insulated rectangular copper and aluminium conductors (picc/piacc), and wrapped rectangular wires. ctc is the flagship. it is used in the high-voltage windings of large power transformers - typically above 10 mva in size - where eliminating eddy current losses in the windings matters enormously. In hvdc (high voltage direct current) transformers, which operate at 400kv and above and are used in india’s long-distance power evacuation projects, ctc is mandatory. ksh is the only indian company approved to supply wire for 400kv hvdc transformers, which means it has no domestic competition in this segment. The approval from pgcil, the entity that builds india’s national transmission grid, took years of qualification and testing.

The mechanism of the hvdc advantage is worth understanding. india is building multiple hvdc corridors to move solar power from rajasthan and gujarat to load centres in the north and east. every hvdc converter transformer in these corridors uses ksh’s wire. these are large, high-value orders placed by companies like hitachi energy india, ge vernova t&d india, and bhel. As of q3 fy26, ksh had received cumulative orders for 37 hvdc transformers, all to be supplied over 12-18 months. These orders are sticky because a transformer oem that qualifies a conductor supplier for a specific transformer rating does not switch mid-project. the re-qualification process is expensive and time-consuming.

PICC (paper insulated copper conductor) serves similar customers - power transformer and reactor manufacturers - but at lower voltage classes. It is the conductor used in transformer windings below hvdc grades, and it is simpler to make than ctc. ksh is approved for picc supply to pgcil, ntpc, npcil, and rdso. The rdso approval is specifically for traction transformer applications in locomotive drives - a growing segment as indian railways electrifies.

The specialized segment also includes wrapped rectangular wires with fiberglass or other specialty insulation, which find use in generators (turbo and hydro), windmill generators, and niche industrial applications. ksh makes specialized stator coils and rotor bars for windmill generators as well.

Standard Winding Wires

Standard Winding Wires - primarily round enamelled copper and aluminium wires - constituted approximately 25% of ksh’s revenue. These serve a different customer set: manufacturers of motors, alternators, gensets, compressors, home appliances, refrigeration equipment, and automotive electrical components.

Round enamelled copper wire (ewcr) is the most common form of magnet wire globally. ksh draws copper rod down to fine gauges, applies enamel insulation in a continuous pass-through oven at controlled temperatures, and spools the finished wire for delivery. The applications range from transformer low-voltage windings to motor armatures to alternator windings in gensets. A genset manufacturer building a 100 kva alternator specifies a particular wire gauge and enamel class; ksh delivers to that specification.

Round enamelled aluminium wire (ewal) is used where weight reduction matters - in compressors, refrigeration motors, and certain large motor applications. Aluminium is 60% lighter than copper for equivalent cross-section but has lower conductivity, so motor designers use larger cross-sections. The economics work when the weight saving justifies the design change.

Standard wires are more commoditised than specialized wires - competitors like precision wires india, ram ratna wires, and vidya wires all produce similar products. ksh competes here primarily on reliability, proximity to customers (both maharashtra-based facilities are within 250km of major oemclusters), and the ability to supply both standard and specialized wire from a single vendor relationship.

Manufacturing Facilities:

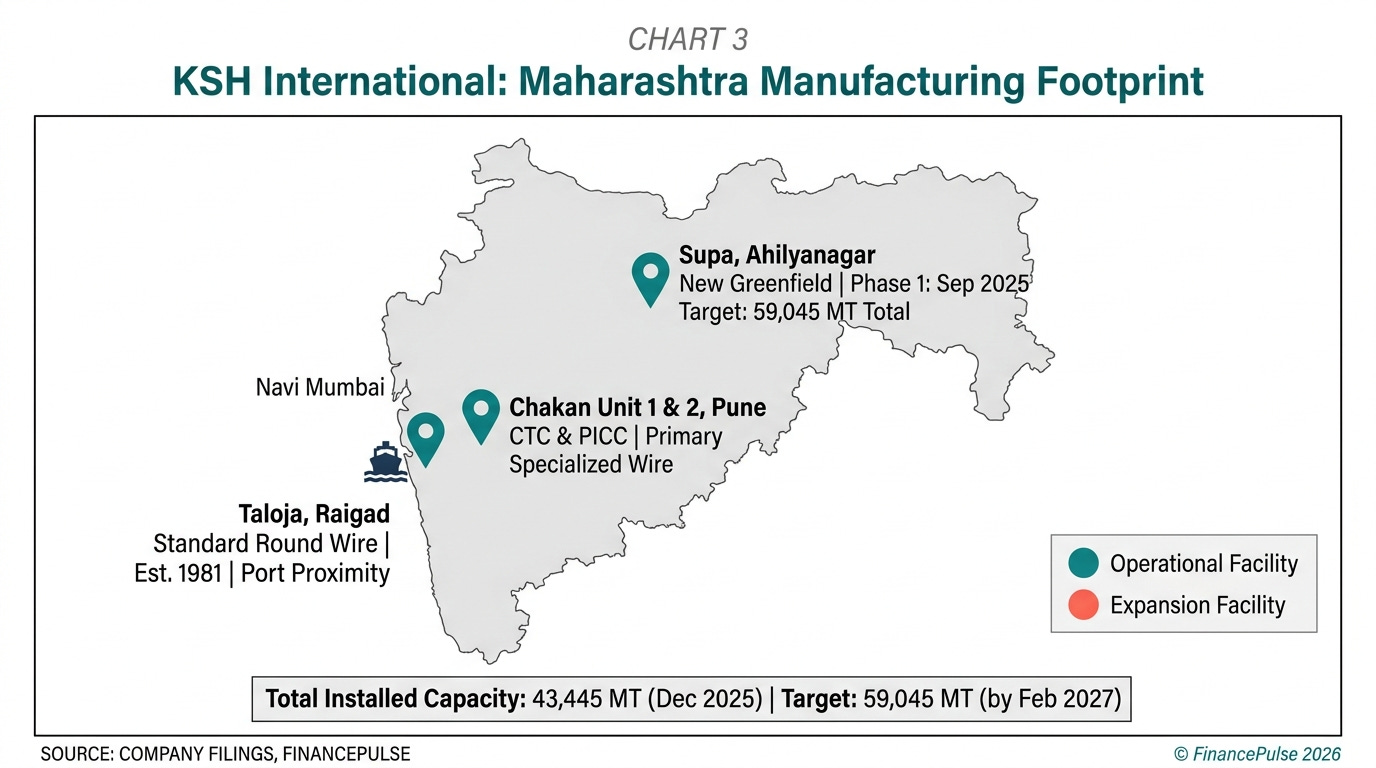

KSH operates four facilities, all in Maharashtra:

Chakan unit 1 and unit 2 (pune, maharashtra): The primary manufacturing base for specialized wires including ctc and picc. Located in chakan industrial zone, which sits within 50km of bharat bijlee, hitachi energy india, siemens energy india, and other key customers. Two separate plants at the same location, with combined annual capacity that forms the bulk of the pre-supa footprint.

Taloja unit (raigad, maharashtra): The original 1981 facility. Located in taloja midc near navi mumbai. Proximity to jawaharlal nehru port allows efficient import of copper rod and export of finished wire. This facility primarily handles standard round wire production. The port proximity is a genuine cost advantage - copper rod arrives from international markets, and wire is exported to 24 countries, so port distance directly affects working capital (copper in transit) and freight costs.

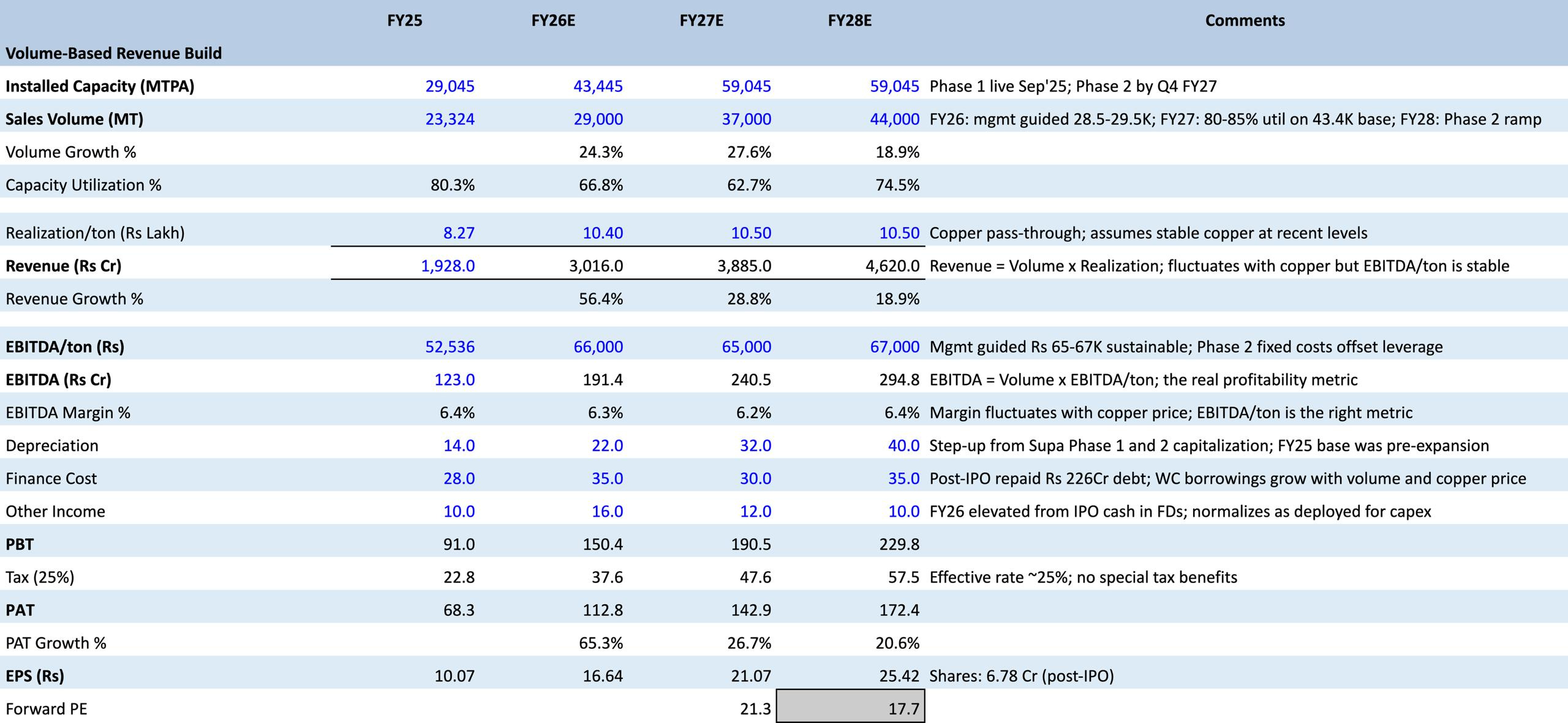

Supa unit (ahilyanagar, maharashtra): The new greenfield facility commissioned in phases. Phase 1 operations began in september 2025, adding 12,000 mt of capacity. By q3 fy26 (december 2025) a further 2,400 mt was added, bringing supa capacity to approximately 14,400 mt. Total capacity across all four facilities was 43,445 mt as of december 2025. Management guided 59,045 mt total capacity within 14 months from q3 fy26, implying approximately february 2027 completion for full supa ramp.

The combined installed capacity of 29,045 mt at the three older facilities operated at 80.7% utilisation in fy25. The supa addition more than doubles total capacity over the two-year ramp-up period. The capital expenditure for supa was approximately rs 90 crore for machinery, partly funded by the ipo proceeds of rs 420 crore (the remainder was applied to debt repayment of rs 226 crore, completed in december 2025, and general corporate purposes).

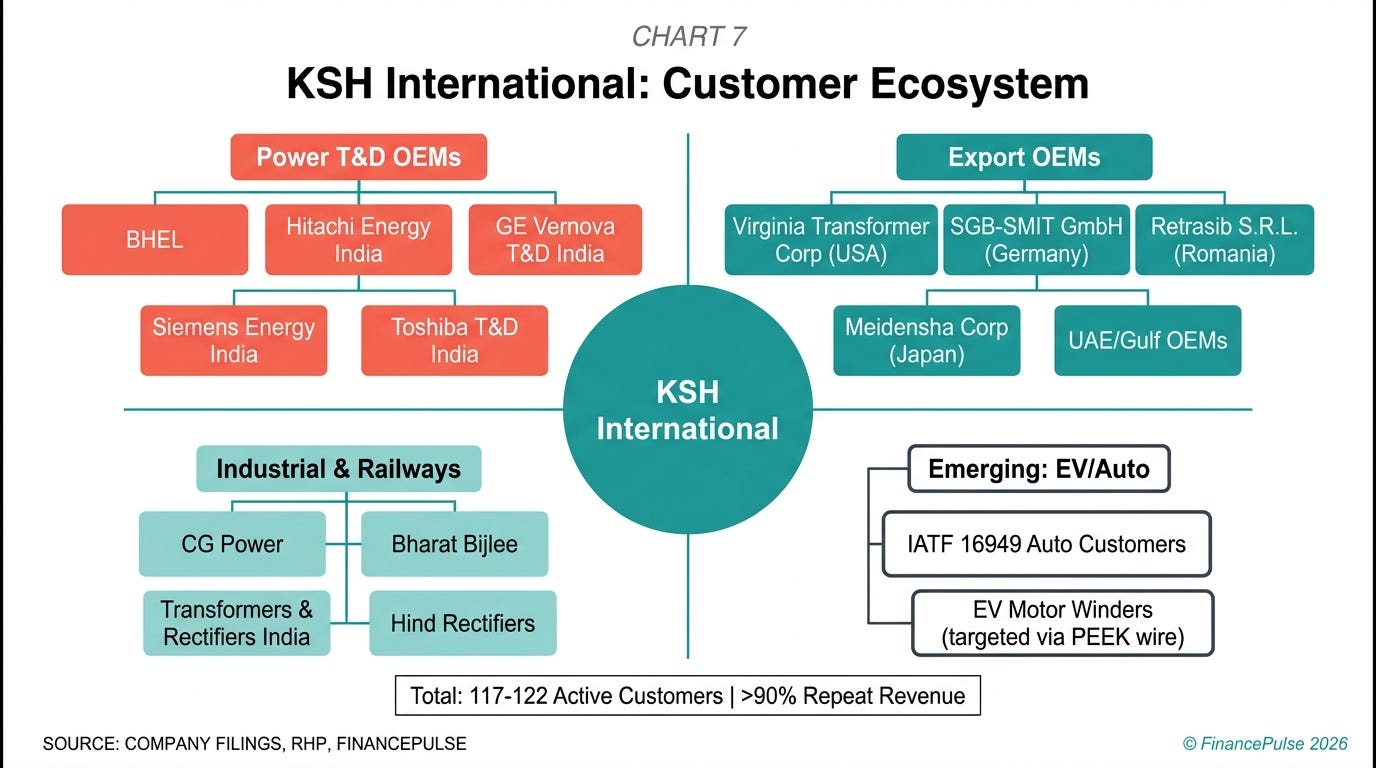

Customers

ksh serves oem customers - companies that build the electrical equipment into which the wire is wound. it does not sell to distributors or to end-users of electrical equipment.

The customer base numbered 122 in fy25 and 117 in fy24 and fy23. over 90% of revenue comes from repeat customers - buyers who have been sourcing from ksh across multiple years. The company served approximately 120 domestic and global oem customers as of q3 fy26.

Export mechanics: exports represented 27-30% of revenue. ksh exports to 24 countries as of june 2025, including the usa, uae, kuwait, romania, saudi arabia, germany, oman, spain, bangladesh, and japan. The export business predominantly consists of ctc and picc - the specialty products that indian wire makers can actually compete with on quality at a cost advantage. Standard round wire exports are smaller because the cost advantage narrows for commodity-grade products. In q3 fy26, export revenue grew 37% year-on-year.

Competitive Landscape

The indian magnet winding wire industry is a concentrated oligopoly with meaningful differentiation at the top end and commoditization at the bottom.

Precision Wires India limited (pwil): The largest manufacturer in india and south asia by production capacity, headquartered at silvassa with facilities in silvassa and overseas. PWIL makes the full range from standard round copper wires to ctc and picc. It has a larger absolute capacity than ksh and serves a similar customer set. pwil competes directly with ksh in every product category. pwil’s advantage is scale and the breadth of its product range - it makes the widest gauge range of enamelled round copper wire in india. ksh’s counter-advantage is its ctc leadership for the hvdc segment specifically, where ksh’s approvals go further (400kv hvdc transformer applications vs. pwil’s standard ctc range).

Ram Ratna Wires limited: The second-largest winding wire manufacturer in south asia by volume. Focused primarily on enamelled round copper wires with a broader product mix that has expanded into copper tubes and bunching/compacting products. Ram ratna competes with ksh on standard round wire but does not have the same depth in specialized transformer conductors. Ram ratna’s strategy has been geographic diversification and product category expansion rather than going deeper in complexity.

Vidya wires limited and Sh haryana wires limited: Smaller players in standard round wire. not meaningful competitors in the specialized ctc/picc space where approvals and technical capability are the barriers.

What actually differentiates ksh

The barriers to entry in specialized wire - particularly ctc for hvdc applications - are formidable. There are three layers:

First, the technical capability to manufacture ctc consistently at specified dimensions requires dedicated machinery and process knowledge. The ctc machine is not off-the-shelf capital equipment; it requires calibration and process development. ksh spent years developing its ctc manufacturing process after starting in 2006.

Second, the regulatory approvals from pgcil, ntpc, npcil, and rdso are not transferable and are not granted quickly. They require sample submissions, destructive testing, factory inspections, and in some cases performance monitoring on actual transformer deployments. a new entrant cannot simply buy a machine and start competing in hvdc-grade ctc; it needs 3-5 years of approval process even if the manufacturing capability is in place.

Third, the global oem approvals from hitachi, ge, siemens, toshiba, and others are equally slow to obtain. These companies run their own vendor qualification programmes with multi-year timelines. a wire manufacturer that wants to supply to hitachi energy’s hvdc transformers needs to pass hitachi’s own qualification, which involves detailed testing at hitachi’s facilities.

ksh is the only indian company approved to supply wire for 400kv hvdc transformers. This is a monopolistic position in a segment that is growing rapidly. The next competitor to challenge it would need to get pgcil avl approval for this specific product category, which starts the clock on a multi-year process.

On the standard wire side, competition is more intense. precision wires, ram ratna, and numerous smaller regional players compete on price, delivery, and service. margins are thin. ksh’s standard wire business competes primarily on the strength of relationships that come from being a one-stop supplier for both specialized and standard wires - a transformer oem that already buys ctc from ksh is more likely to also consolidate its round wire sourcing with ksh.

Industry

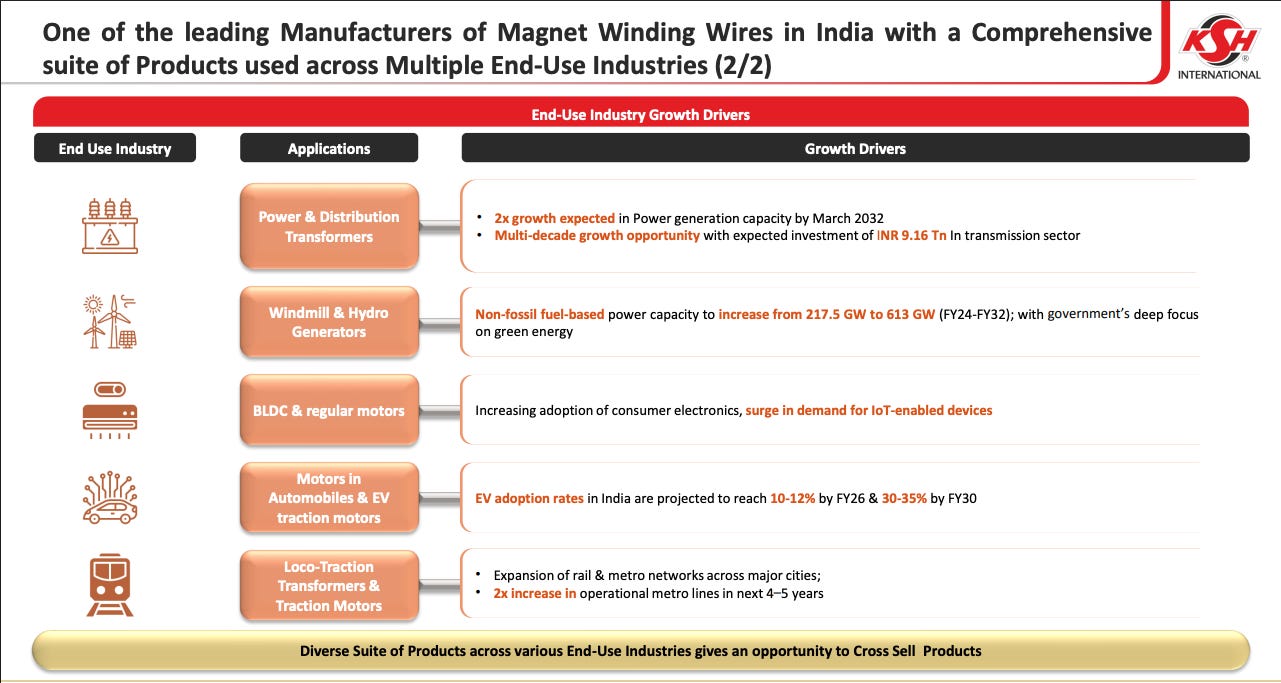

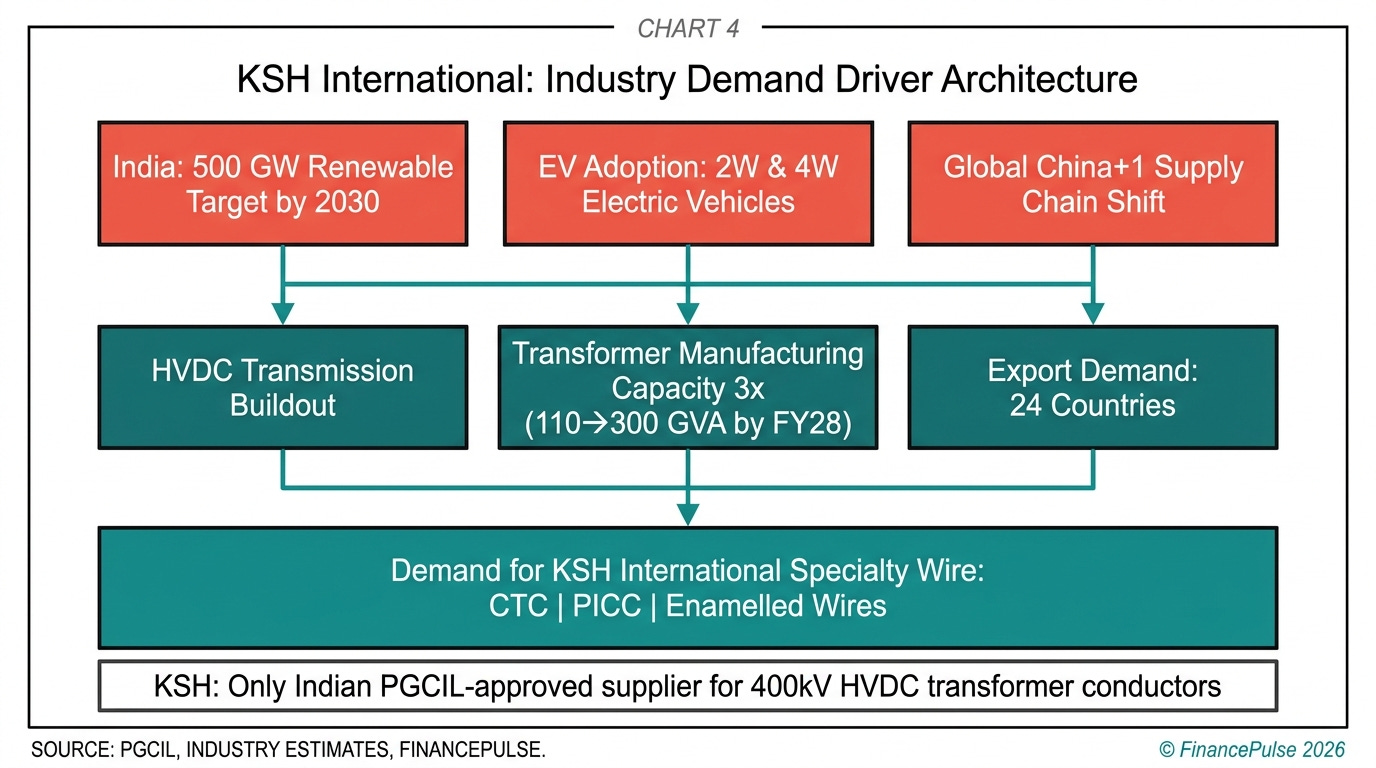

Magnet winding wire is an input to the electrical equipment industry. Its demand is a direct function of how much electrical equipment is being built. Understanding ksh’s demand environment requires understanding what is driving electrical equipment production.

India’s power sector investment cycle: India has committed to 500 gw of renewable energy capacity by 2030. Solar and wind generation is inherently located far from load centres - solar in rajasthan and gujarat, wind along coastlines - which means every megawatt of renewable capacity added requires transmission infrastructure to bring the power to cities. Each kilometer of high-voltage transmission line requires transformers at both ends. India’s transmission buildout is running at multiple times the historical rate. The central transmission utility (ctu, which pgcil operates) and state transmission utilities are placing large transformer orders, and transformer manufacturers are at near-capacity utilisation. According to icici securities, india’s transformer manufacturing capacity is set to triple from approximately 110 gva to 300 gva by fy28. Every single transformer in this expansion requires ctc, picc, and winding wire.

HVDC specifically: India is building its first hvdc corridors - long-distance direct current transmission lines that transmit power at much higher voltages than conventional ac transmission, enabling power flows of thousands of megawatts over distances of 1000+ kilometres. Each hvdc project uses converter transformers at both ends - massive, complex, high-value machines that require hvdc-grade ctc. The current pipeline includes projects connecting rajasthan solar zones to the north and east. KSH is the only approved indian supplier for this specific conductor category.

Growth Triggers

Supa facility full ramp to 59,045 mt capacity: Total capacity was 43,445 mt as of december 2025. Management guided reaching 59,045 mt within 14 months - approximately february 2027. Q4 fy26 was characterised as the first full quarter of supa phase 1 operations. The supa facility is specifically designed for specialized winding wires, targeting the ctc and specialty markets.

HVDC order pipeline execution: KSH has received cumulative orders for 37 hvdc transformer winding wire packages as of q3 fy26. All 37 orders are to be executed over 12-18 months. These are high-margin, high-value-addition orders with no domestic competition. The hvdc pipeline in india is multi-year in nature - the national transmission plan calls for multiple hvdc corridors, so new orders are expected to continue as projects move from planning to procurement.

Only approved indian supplier for 400kv hvdc transformers: This approval gives ksh exclusive access to every new hvdc converter transformer order placed by indian oems. As india’s renewable energy evacuation buildout accelerates, this position becomes more valuable with each new project announcement.

EV traction motor wire development via hpw metallwerk: Through an exclusive licensing agreement with hpw metallwerk, announced january 2026, ksh is developing peek-insulated round wires for 800v ev traction motors. Management guided entry into the 4-wheeler ev traction motor market within 12-18 months from q3 fy26. 2-wheeler ev motors are already being supplied. PEEK wire for 800v applications commands substantially higher per-ton pricing than standard enamel.

India transformer manufacturing capacity tripling: External data point cited by icici securities, consistent with industry sources - India’s transformer manufacturing capacity is targeting a scale from approximately 110 gva to 300 gva by fy28. KSH as the approved ctc supplier to the transformer oems at the core of this expansion is directly positioned to benefit.

Copper payables normalisation improving working capital: As of q3 fy26, ksh was paying copper suppliers on advance payment terms because of its relatively small scale. Management indicated that as volumes grow, they expect to shift to credit-based procurement, lengthening payable days from the current 5 days to a more normal range. This would release significant working capital tied up in prepayments and reduce the cash cycle.

key Risks

Copper price volatility and working capital trap: Copper accounts for approximately 85-90% of raw material cost. Copper prices can move 20-30% in a year. While ksh passes through copper price changes to customers, the mechanics create a working capital trap: KSH buys copper at spot or near-spot, processes it, and invoices at the processed price after a 30-45 day manufacturing and delivery cycle. If copper prices rise sharply, ksh needs more cash to fund the inventory build before the revenue is collected. As of q3 fy26, working capital days were approximately 75-80, partly inflated by inventory stocking of critical insulating materials. KSH currently pays suppliers in advance (payable days of approximately 5), meaning it funds its entire inventory before any credit from suppliers. A sustained copper price spike combined with customer payment delays would compress liquidity rapidly. The company had rs 519 crore of debt as of october 2025, partially paid down to approximately rs 293 crore (rs 226 crore repaid) by december 2025.

Customer concentration in the power t&d sector: While ksh has 117-122 active customers, the dominant revenue share comes from transformer oems supplying the power t&d sector. A slowdown in india’s transmission capex - which is fundamentally a government spending decision - would directly hit demand for ctc and picc. India’s t&d capex has historically been lumpy; planned transmission additions have been delayed by land acquisition issues, financing constraints, and bureaucratic timelines. If the hvdc pipeline is delayed by 12-18 months relative to current expectations, ksh’s 37-order hvdc backlog would still be executed but the next wave would slow. This would affect the supa facility utilisation since it is being built to capture exactly this demand.

Scenarios & Valuation

Bull Case

India’s transformer manufacturing capacity expansion plays out faster than the historical pace. PGCIL and state utilities accelerate procurement to catch up with delayed projects, and the hvdc pipeline - which currently has 37 orders in backlog - continues generating new orders as three or four new hvdc corridors are tendered over the next 18 months. KSH executes the full supa ramp to 59,045 mt on schedule by early 2027, giving it the capacity to absorb the demand without turning away orders.

In this world, the supa facility runs at high utilisation in specialized wire from the start because the demand is already there in the form of hvdc orders. Export growth continues at 30%+ as western transformer manufacturers accelerate their india sourcing following the us tariff changes. The peek-wire licensing bears fruit and ksh becomes a qualified supplier for one or two 4-wheeler ev oems by late fy27, opening an entirely new margin accretive revenue stream. the shift from advance payment to credit-based copper procurement happens more quickly than expected as ksh’s volumes give it bargaining leverage with copper rod suppliers, releasing working capital and reducing the cash cycle. care ratings upgrades ksh’s credit profile further, reducing borrowing costs on the large working capital facility needed for a business at this scale.

The new ceo brings operational discipline and helps ksh scale up its commercial team to match its manufacturing capability. the company deepens its customer relationships with international oems - adding one or two new global transformer manufacturers to its export base who are specifically qualifying non-chinese ctc sources. Management builds on the monopoly position in hvdc-grade ctc to extend into 1200kv uhv transformer applications, which india is beginning to plan for its next-generation transmission network.

Base case

The supa facility ramps on approximately the guided timeline, reaching full capacity somewhere in fy27-28. hvdc orders continue at the current pace - roughly matching execution of the existing backlog with modest additions as new hvdc projects reach procurement stage. Exports grow at 20-30% annually as the china+1 shift plays out gradually rather than rapidly. The standard wire business grows broadly in line with india’s electrical equipment production, which benefits from manufacturing capex and the government’s infrastructure push.

The peek wire opportunity develops but takes longer than 12-18 months to generate material revenue - qualifying for 4-wheeler ev traction motors involves extensive testing and the 800v platform rollout in india is gradual. The working capital situation improves modestly as copper payment terms normalise over fy27. The new ceo settles into the role without major disruption.

ebitda per ton improves gradually from the current rs 65,000-67,000 range as the product mix shifts further toward specialized wires and operating leverage from the supa facility kicks in. The company emerges from the supa capex cycle as a substantially larger business - roughly double the fy25 scale by fy28 - with a stronger balance sheet having eliminated most of its term debt.

Bear Case

The hvdc order pipeline stalls. India’s renewable energy buildout is slower than planned, as it frequently has been historically. Land acquisition delays, grid integration challenges, and state utility financing constraints push hvdc commissioning timelines to the right. the 37 orders in backlog are executed, but the next wave of orders is delayed by 18-24 months. The supa facility, specifically built to serve the specialized wire market, runs at low utilisation. The fixed cost base from the new facility creates margin pressure during the under-utilisation period.

Simultaneously, copper prices spike sharply - which has happened before - compressing the cash cycle and straining the working capital facility. KSH finds it difficult to shift to credit-based copper procurement faster than anticipated because copper suppliers demand advance payment from any customer whose volumes are not yet established at the new supa-level scale. The balance sheet, though improved post-debt repayment, gets stretched again as working capital requirements grow with revenue but payable terms do not improve.

The peek wire opportunity does not materialise within the guided timeline - ev oem qualification takes longer than 18 months, and the 800v architecture rollout in india is pushed to fy28-29. A competitor - potentially precision wires, which has a larger manufacturing base and relationships with the same oem customers - obtains a competing hvdc qualification from pgcil, eliminating ksh’s monopoly position in this segment.

The management transition - the new ceo installed in april 2026 - proves disruptive to a business that has historically operated as a closely held family enterprise. execution slows during the transition. meanwhile, the ipos of fy25-26 in the capital goods sector have set high bar expectations, and ksh’s muted listing premium means there is little goodwill cushion if results disappoint even modestly.

Thanks for reading!