Nykaa: India’s Beauty Platform Playbook

A deep dive into India’s leading beauty retailer and its multi-engine growth model

Before we begin - a quick note. I recently launched my first product, Growth Triggers. It started as a personal system to track earnings calls and growth drivers and has now turned into a live database covering 1000+ Indian companies, with growth catalysts, guidance filters, and relative strength scans.

If you want to see what I’ve been building, you can check it out here ( since launching, i have been constantly adding features to keep adding value)

What does Nykaa do?

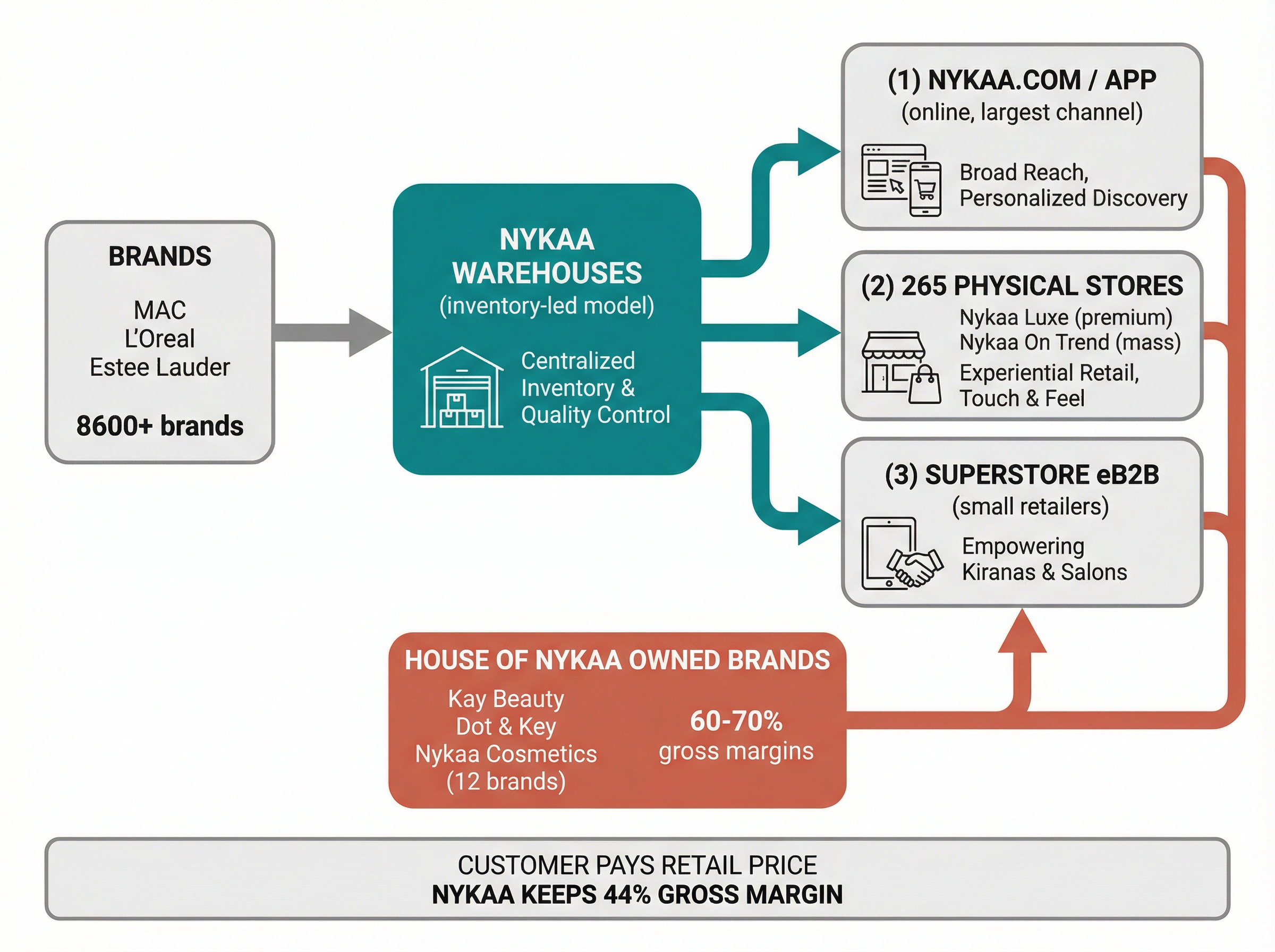

Nykaa sells beauty products and fashion to Indian consumers, primarily through its website and app, but increasingly through a growing network of physical stores. The simplest way to understand the business: say a woman in Pune wants to buy a MAC lipstick. She could go to a department store (if one exists nearby), but the selection is limited. She could try Amazon, but counterfeits are rampant in Indian beauty e-commerce. Or she goes to Nykaa, where the product is guaranteed genuine. Nykaa buys that lipstick directly from MAC (or its authorized distributor), warehouses it, and ships it to her. Nykaa keeps the difference between what it paid for the lipstick and what it charged the customer.

This “buy first, sell second” structure is how Nykaa makes money in beauty. The company purchases inventory from over 8,600 beauty brands (as of Q3 FY26), stores it in its own warehouses, and sells it to consumers at a markup. For a ₹1,000 MAC lipstick, Nykaa might have paid ₹550-600 to MAC’s distributor, meaning it pockets ₹400-450 in gross margin before fulfillment, marketing, and overhead. The beauty business runs 44-45% gross margins, excellent for a retailer and a reflection of the fat markups inherent in cosmetics globally (U.S. retail cosmetics markups run 50-60%).

Nykaa was founded in 2012 by Falguni Nayar, a former Managing Director at Kotak Mahindra Capital Company. She saw an obvious gap: India’s beauty and personal care market was large and growing with rising incomes, but offline retail was fragmented and unreliable. No credible online player existed. Nykaa filled that gap by guaranteeing authenticity. That sounds trivial, but it mattered in a market where consumers had been burned by fakes on horizontal platforms.

The business model

Nykaa runs two verticals on fundamentally different economic models.

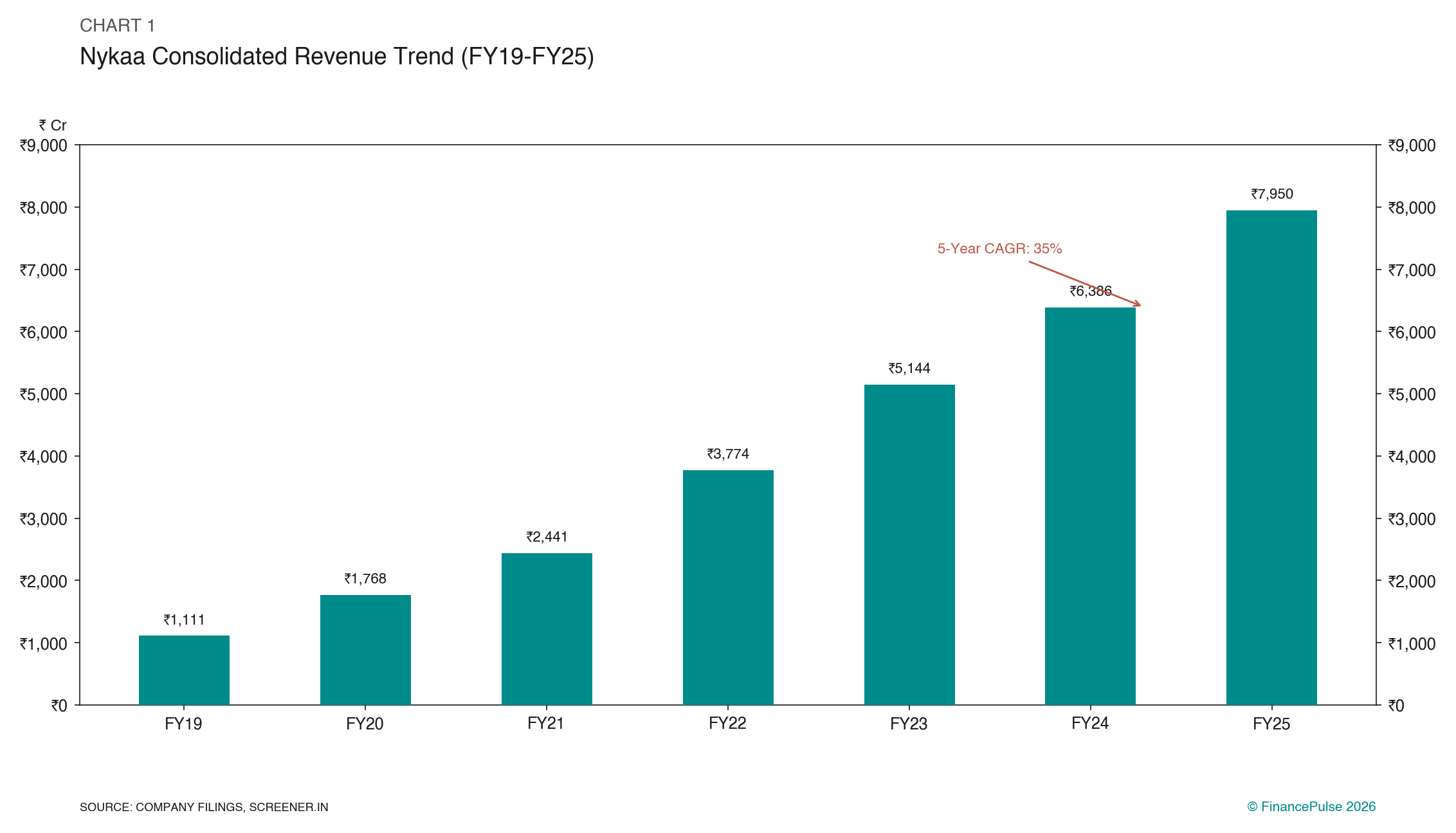

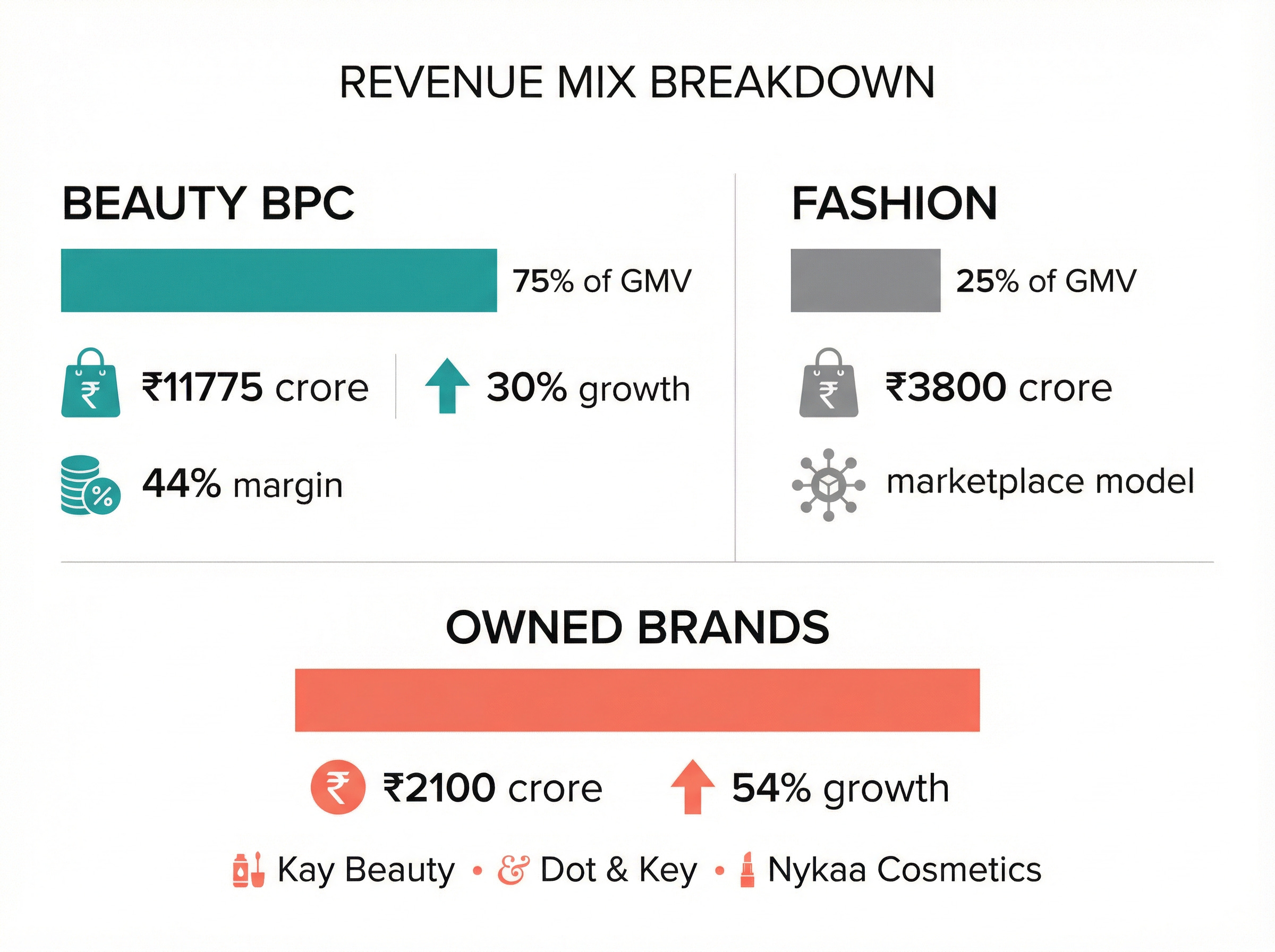

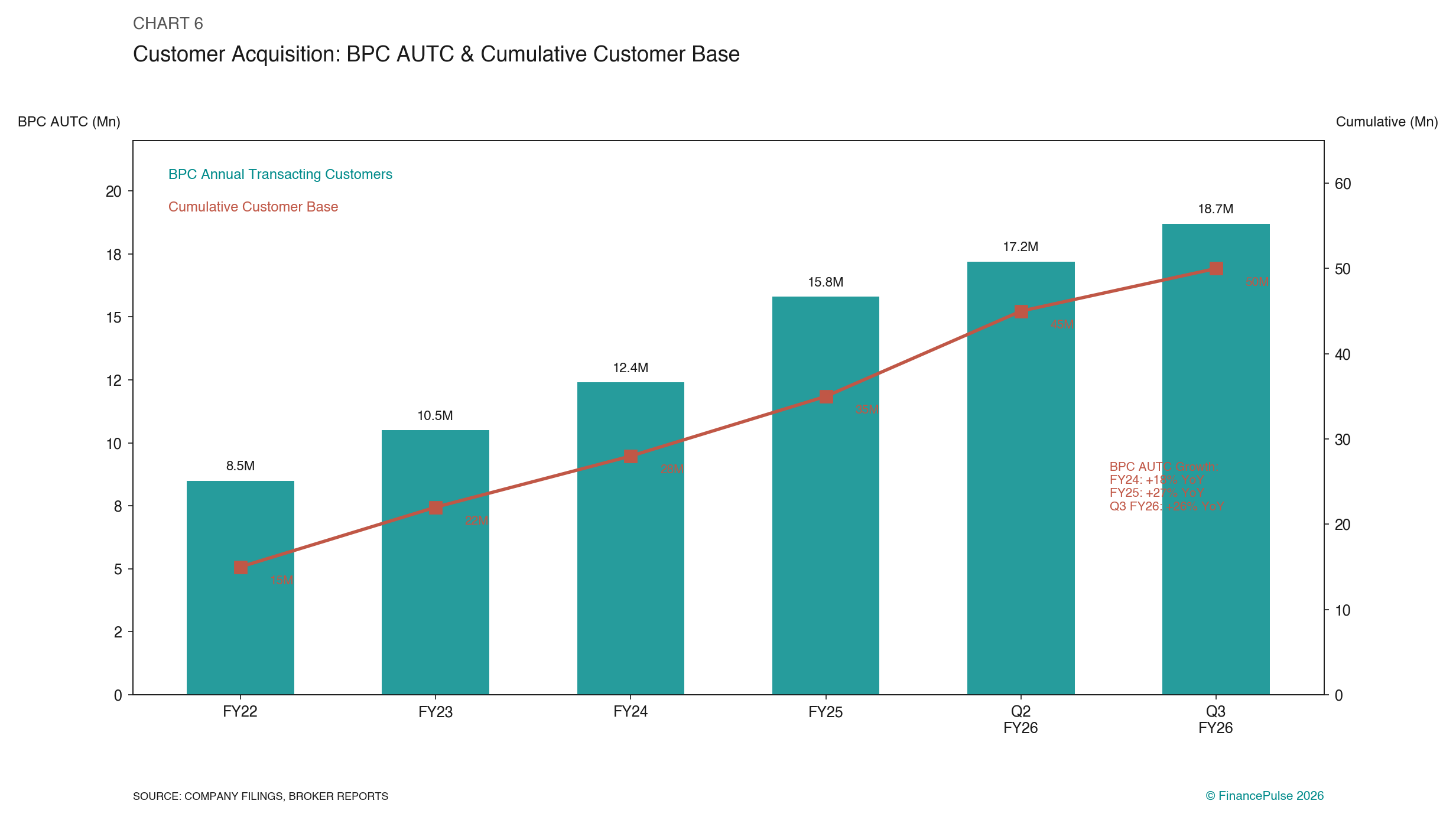

Beauty and Personal Care (BPC) accounts for about 75-76% of GMV. This runs on an inventory led model. Nykaa buys products from brands, holds them in warehouses, and sells to consumers. The company earns the retail margin between its purchase price and selling price. In FY25, the beauty segment generated GMV of ₹11,775 crore (growing 30% year-over-year) with gross margins around 44%. The beauty customer base has scaled to over 34 million (as of FY25), expanding to 49 million cumulatively by Q2 FY26.

The beauty business sells through multiple channels. Online (nykaa.com and the Nykaa app) is the largest and most profitable. Physical retail (265 stores as of Q2 FY26) operates three formats: Nykaa Luxe stores carry premium and luxury brands (Estee Lauder, Chanel, Charlotte Tilbury), Nykaa On Trend stores target the mass-premium segment, and standard Nykaa stores bridge the two. These stores serve two purposes: they drive discovery and trust (customers can try products before buying), and they function as micro-fulfillment hubs for Nykaa Now, the company’s rapid delivery service (30-120 minute delivery across 7 cities using 53 rapid stores).

There is also Superstore by Nykaa, an eB2B distribution arm that sells beauty products to small, unorganized retailers. A local kirana shop wants to stock branded beauty products but cannot deal directly with L’Oreal or Maybelline. Superstore by Nykaa aggregates demand from these small retailers, giving them access to Nykaa’s brand assortment. This vertical has tripled its GMV in last two years.

Fashion accounts for 24-25% of GMV and runs on a marketplace model, the opposite of beauty. Nykaa Fashion does not buy or hold fashion inventory. Brands list products on the platform, Nykaa takes a commission (take-rate) on each sale, and the brand handles fulfillment or uses Nykaa’s logistics. The fashion segment had GMV of approximately ₹3,800 crore in FY25 and has been growing around 25-37% depending on the quarter. Why a marketplace model for fashion? Fashion has far more SKUs, higher return rates, and faster trend cycles than beauty. Holding fashion inventory would be capital-destructive. Beauty products, by contrast, have long shelf lives, low return rates, and concentrated brand loyalty, making inventory ownership sensible.

Fashion still loses money at the EBITDA level, but losses are narrowing fast. The EBITDA margin went from -9% in Q2 FY25 to -3.5% in Q2 FY26, and -2% by Q3 FY26. Management has guided for fashion EBITDA break-even by FY26 (March 2026), and the trajectory suggests this is achievable.

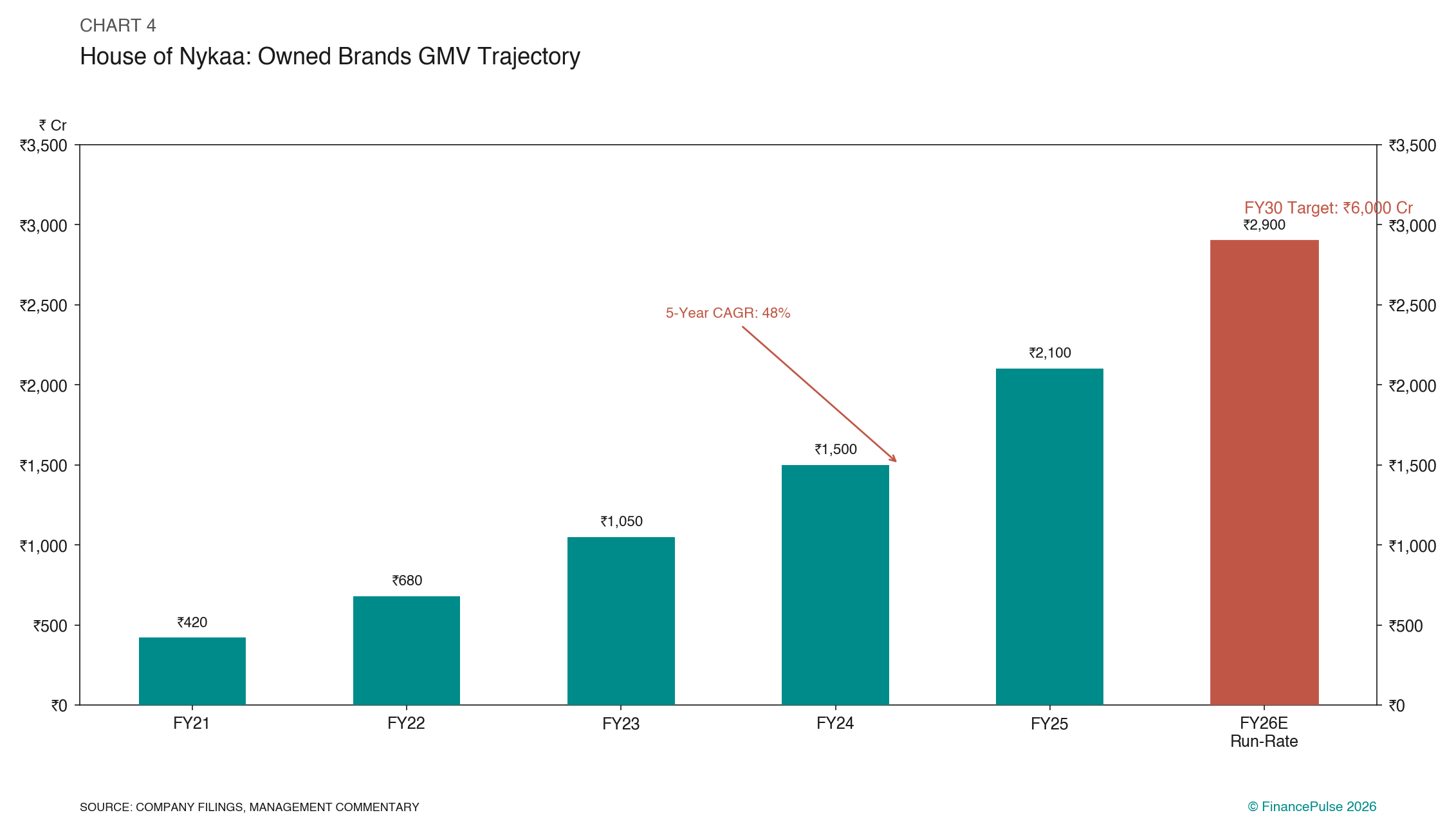

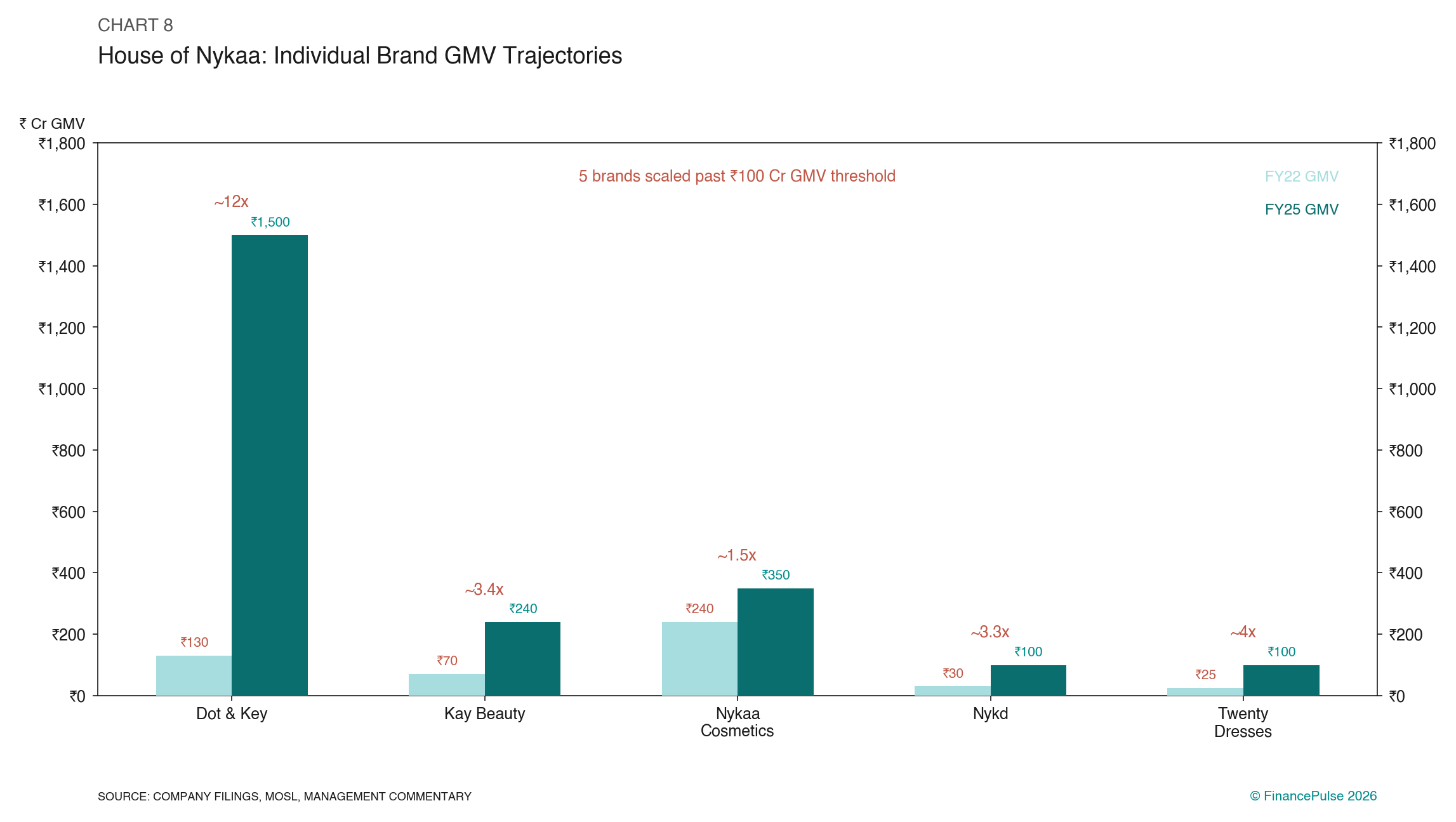

Owned brands (House of Nykaa) are the key margin lever across both verticals. Nykaa now operates 12 proprietary brands, including Nykaa Cosmetics (makeup), Nykaa Naturals (personal care), Kay Beauty (co-founded with Bollywood actress Katrina Kaif), Dot & Key (acquired skincare brand), Earth Rhythm (acquired clean beauty brand), and KICA (activewear). The House of Nykaa portfolio achieved a GMV run-rate of ₹2,100 crore in FY25, growing at a 48% five-year CAGR. In Q2 FY26, owned brands GMV grew 54% year-over-year. Kay Beauty alone crossed ₹500 crore in annual GMV and has launched internationally in the UK and Middle East.

The owned brands mix has been climbing steadily as a proportion of Nykaa’s total GMV. In the BPC vertical, owned beauty brands rose from 12.1% of BPC GMV in FY24 to 14.4% in FY25, a gain of 230 basis points in a single year. In fashion, owned brands (led by Twenty Dresses and Nykd) contributed approximately 11% of Fashion GMV in FY25. By Q2 FY26, the total House of Nykaa portfolio had reached an annual GMV rate of approximately ₹2,900 crore. Five owned brands have crossed the ₹100 crore GMV threshold (Dot & Key, Nykaa Cosmetics, Kay Beauty, Nykd, and Twenty Dresses), demonstrating a repeatable ability to incubate, acquire, and scale consumer brands. The portfolio spans a deliberate mix of acquired-and-scaled brands (Dot & Key, Twenty Dresses, Earth Rhythm, Nudge Wellness) and in-house incubated brands (Nykaa Cosmetics, Nykd, Kay Beauty), each benefiting from Nykaa’s data on price points, shade ranges, formats, and consumer trends.

Why owned brands matter: a third-party MAC lipstick earns 44% gross margin. A Nykaa Cosmetics lipstick earns 60-70% gross margin because there is no middleman brand to pay. Production cost for a private-label cosmetic sits far below retail price, and Nykaa controls the entire value chain from formulation to shelf. Owned brands also give Nykaa pricing power, shelf space control (they can promote their own products preferentially on the platform), and brand equity that transcends the marketplace. a higher owned-brand mix “structurally improves gross margins and LTV/CAC ratio, supporting long-term operating leverage.” The owned brands are also increasingly present outside the Nykaa ecosystem: approximately 44% of owned beauty brand revenue already comes from channels outside Nykaa’s own platform, including general trade, modern trade, and third-party e-commerce. Nykaa Cosmetics alone has 14,000+ dedicated GT/MT retail doors.

Unit economics

Nykaa’s beauty margins are attractive because of a simple truth: cosmetics are one of the highest markup consumer products in the world. A lipstick that costs ₹50-100 to manufacture (including packaging) retails for ₹500-1,500. A foundation that costs ₹80 to produce retails for ₹1,000-3,000. The entire beauty supply chain runs on 50-60% retail markups in mature markets, and India’s growing premiumisation is pushing that higher. Nykaa, as the dominant specialty retailer, captures a large portion of this markup.

Consolidated gross margins were 43.7% in FY25, improving to 44.6-44.9% in recent quarters (Q1-Q2 FY26). Two dynamics drive this expansion: rising owned brand contribution (60-70%+ gross margins) and premiumisation in the beauty mix, with premium customers spending 9x more than average customers and the top 10% spending roughly $395 annually.

The BPC cost structure in detail

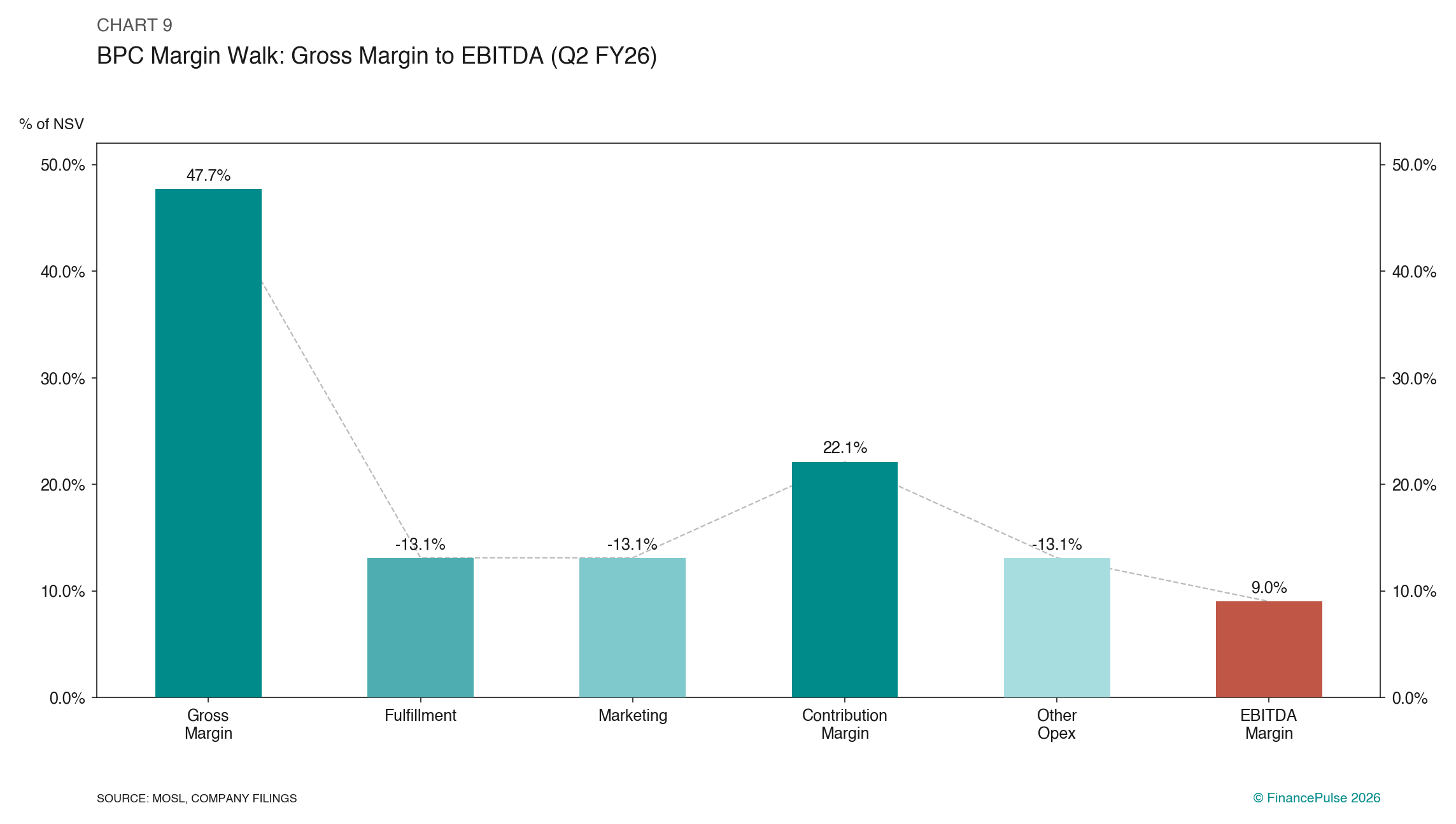

The Q2 FY26 BPC margin walk shows how the 47.7% gross margin gets consumed before reaching EBITDA. Fulfillment costs (warehousing, packaging, delivery) absorb approximately 13.1% of net sales value, and marketing and advertising takes another 13.1%. These two buckets alone eat over 26 percentage points of gross margin. After fulfillment and marketing, the contribution margin sits at roughly 22.1% of NSV. Other operating expenses (technology, corporate overhead, store operations, employee costs) then consume an additional 13 percentage points, leaving the BPC segment with a 9.0% EBITDA margin in Q2 FY26. BPC contribution margin has held between 21% and 23% across the last eight quarters, indicating Nykaa is not buying growth through margin sacrifice.

Fashion tells a different story. Gross margin sits around 44.6%, comparable to beauty, but fulfillment costs are heavier at 11.2% of NSV because of higher return driven reverse logistics. Marketing spending at 9.5% is actually lower than beauty (fashion benefits from cross-sell from Nykaa’s beauty base), producing a contribution margin of 26.9%. The problem lies in the “other expenses” bucket at 13% of NSV, which, combined with the higher fulfillment burden, drags fashion to a -3.4% EBITDA margin. The core difference: beauty returns run 3-6% of orders. Fashion apparel returns run 30-35%, and even luxury fashion sees 15-20% return rates. Reverse logistics in fashion cost disproportionately more per unit than forward logistics, and every returned item erases the contribution margin of that sale entirely.

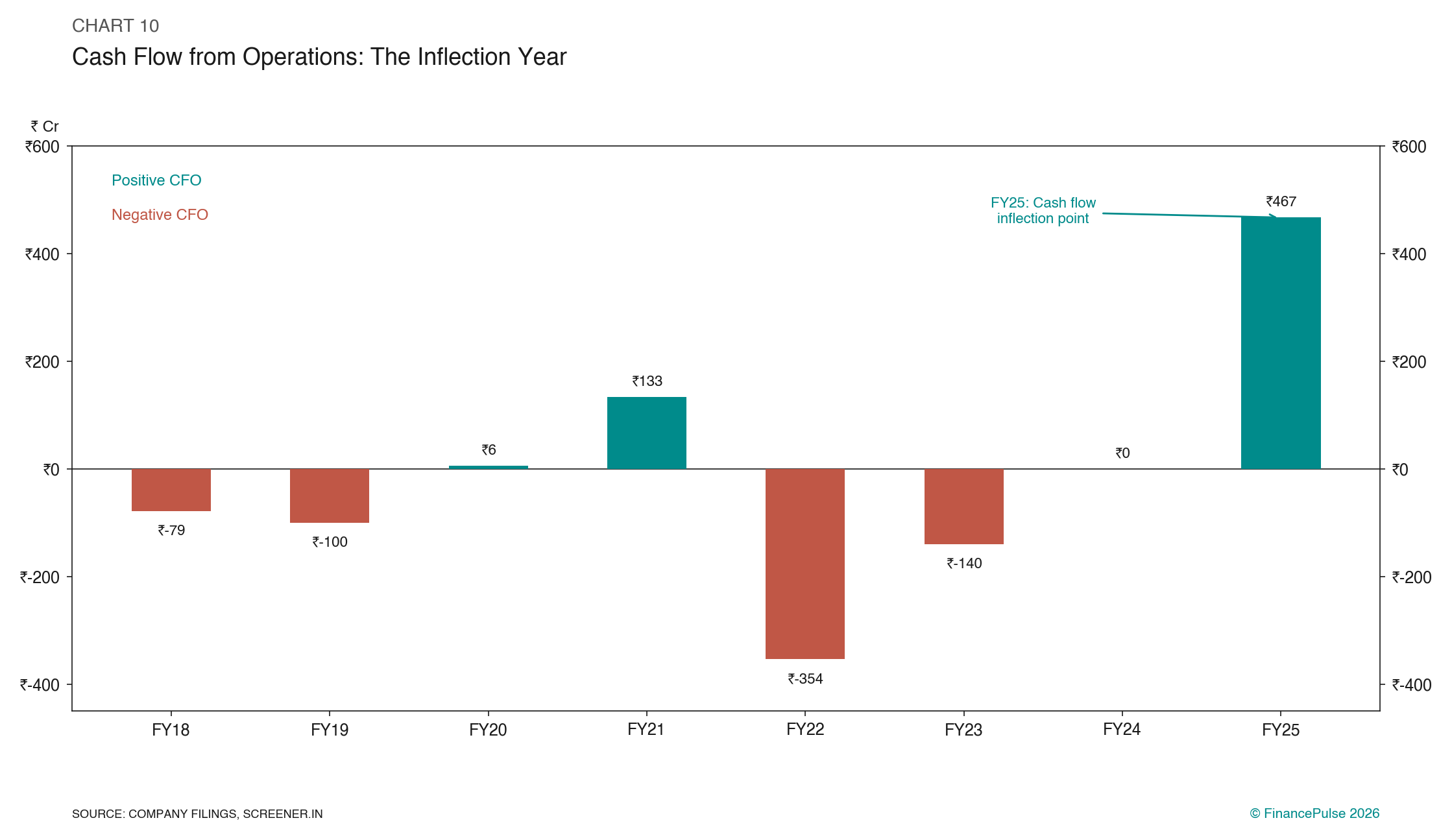

Cash flow has been improving. FY25 was the first year Nykaa generated meaningful operating cash flow (₹467 crore), compared to near-zero the prior year. Improving profitability, better working capital management (days fell from 94 in FY24 to 75 in FY25), and operating leverage as revenue scales drove the inflection.

Scale advantages & moat

Brand assortment and trust as a competitive moat. Nykaa carries over 8,600 beauty brands and 5,000+ fashion brands. Many premium and luxury beauty brands (Chanel Beauty, Estee Lauder, Charlotte Tilbury, Bobbi Brown, MAC) choose to work with Nykaa as their primary online retail partner in India, sometimes exclusively. Luxury brands are obsessive about distribution control and brand presentation. They will not sell on a horizontal marketplace where a ₹5,000 foundation sits next to ₹50 shampoo sachets and grey-market sellers undercut prices. Nykaa’s curated, beauty-specific environment, combined with its inventory-led model that eliminates counterfeit risk, makes it the “safe” choice for prestige brands. Falguni Nayar’s personal relationships with global beauty conglomerates (L’Oreal Group, Estee Lauder Companies, LVMH) further cement these partnerships.

This creates a self-reinforcing cycle. Luxury brands need a trustworthy channel in India. Nykaa is the only scaled specialty beauty platform. Brands list on Nykaa. Consumers come because Nykaa has the best selection. More consumers attract more brands. This is a curated retailer advantage (like Sephora globally) rather than a network effect in the traditional sense.

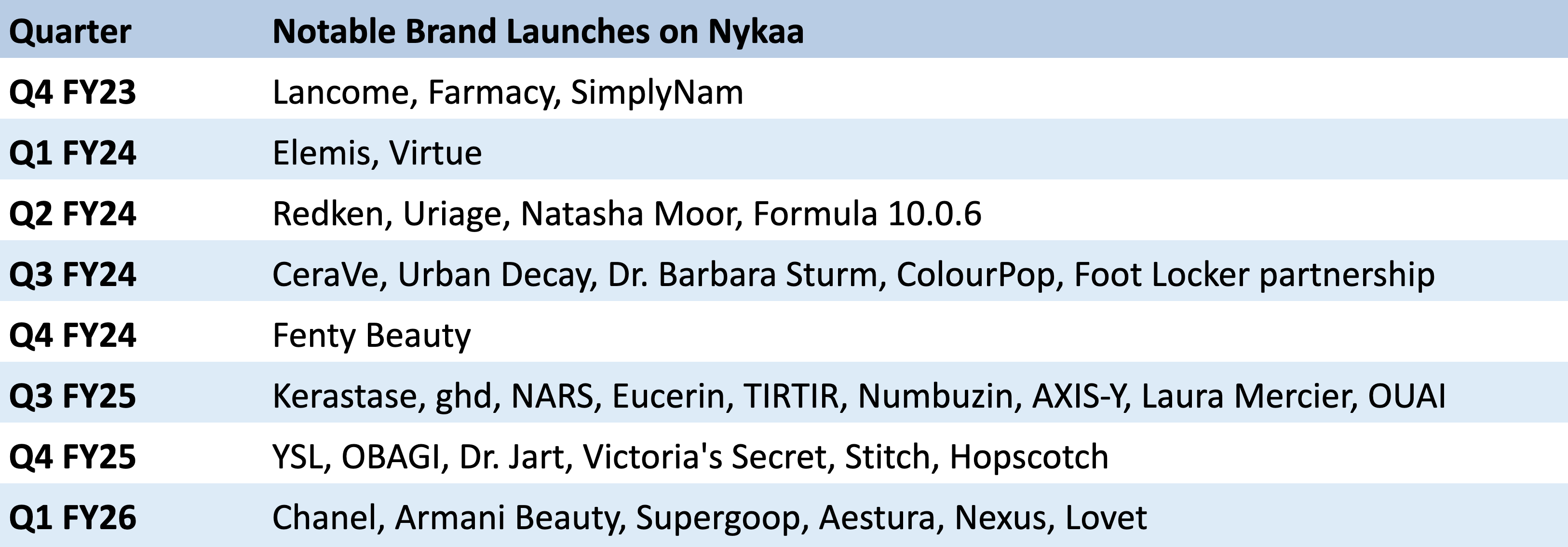

The depth of Nykaa’s brand relationships shows in the steady cadence of premium launches. In Q4 FY23, Lancôme and Farmacy launched on the platform. Q2 FY24 brought Redken and Uriage. Q3 FY24 saw CeraVe, Urban Decay, Dr. Barbara Sturm, and ColourPop. Q4 FY24 brought Fenty Beauty’s India entry through Nykaa. The pace accelerated through FY25 and into FY26: Q3 FY25 added Kérastase, ghd, NARS, Eucerin, TIRTIR, Numbuzin, Laura Mercier, and OUAI in a single quarter. Q4 FY25 brought YSL, Dr. Jart, and Victoria’s Secret. Q1 FY26 was the biggest quarter yet, with Chanel, Armani Beauty, Supergoop, and Aestura choosing Nykaa as their India entry point. Many of these brands launched on Nykaa as an exclusive or first-to-market partner, giving the platform an early-mover advantage that compounds over time.

Switching costs are moderate but exists. A Nykaa customer builds purchase history, product wishlists, a beauty profile, and loyalty rewards on the platform. The Nykaa app remembers their skin type, shade preferences, and past purchases. No single product is exclusive to Nykaa. But the convenience of finding all preferred beauty brands in one place, combined with the authenticity guarantee, creates real stickiness. The premium customer cohort (top 10% by spending) has high repeat purchase rates and represents a disproportionate share of revenue, which suggests genuine loyalty rather than just transactional convenience.

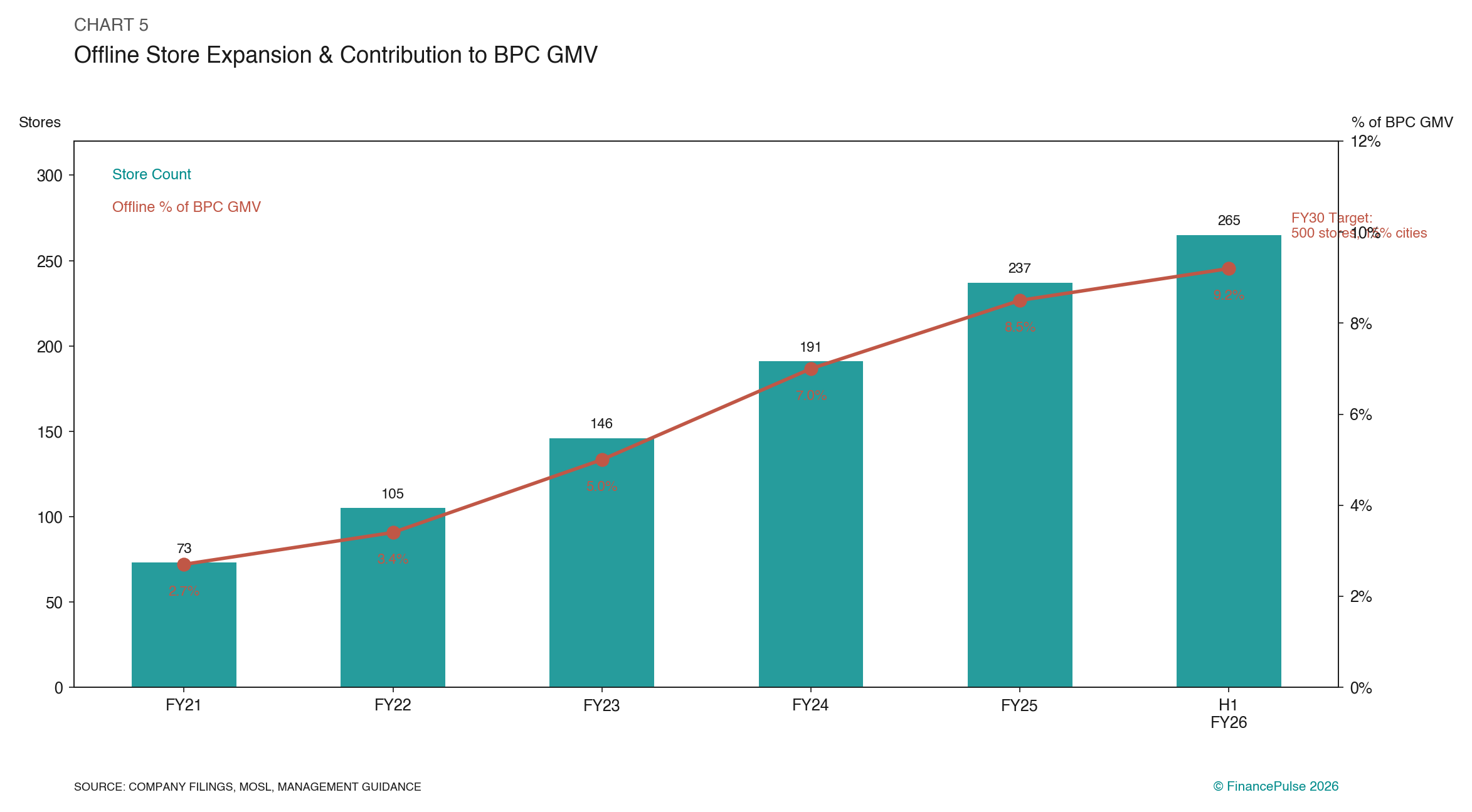

Offline store network as a physical moat. Nykaa has 265 beauty stores across 90 cities (as of Q2 FY26) and plans to reach 500 stores in 100+ cities by FY30. This would be India’s largest specialty beauty retail network. The network is difficult to replicate quickly. Each store requires a lease, build-out, trained beauty advisors, premium brand partnerships (luxury brands often approve store locations individually), and time to reach profitability. Amazon and Flipkart cannot easily build this. Beauty retail requires tactile product trial, expert consultation, and a premium physical environment, none of which horizontal e-commerce players are designed to deliver.

The offline channel’s contribution to overall BPC GMV has grown steadily, from 3.4% in Q1 FY22 to 9.0% by Q3 FY25, and the store count expanded from 73 stores at the end of FY21 to 265 by H1 FY26. Two-thirds of store GMV comes from premium brands, positioning Nykaa’s physical network as the preferred destination for prestige beauty discovery and conversion. The stores function as a premiumisation engine. The in-store experience (shade trials, makeovers, fragrance testing, skin diagnostics) drives conversion on high-value items that consumers would not buy sight-unseen online. Beauty is one of the few e-commerce categories where offline discovery converts systematically into online replenishment, creating a flywheel that strengthens as the store network grows.

Content ecosystem. Nykaa’s content strategy (Nykaa TV, beauty blogs, YouTube Shopping partnership, creator affiliate programs with 10,000+ creators) generates organic traffic and builds authority in beauty advice. Because Nykaa has the largest beauty-focused content library in India, the cost of content creation per customer acquired falls as the customer base grows. A beauty tutorial video costs the same to produce whether 10,000 or 10 million people watch it, but the customer acquisition payoff scales with every viewer.

Owned brands as a structural advantage. The House of Nykaa portfolio (₹2,100+ crore GMV, growing 54%) means Nykaa is simultaneously the platform and the brand. When a customer visits Nykaa to buy a competitor’s moisturizer, Nykaa can place its own Dot & Key moisturizer alongside it, at a competitive price and with platform-native endorsements. The conversion advantage of selling owned brands on your own platform is large, and the margin uplift (from ~44% gross margin on third-party to 60-70% on owned brands) compounds as owned brands grow as a share of mix.

Customers

Nykaa’s cumulative customer base reached over 49 million by Q2 FY26 (September 2025), with 34+ million in beauty alone as of FY25. The base grew 30% year-over-year in Q1 FY26. Acquisition momentum remains strong. Annual unique transacting customers (AUTC) for BPC hit 18.7 million in Q3 FY26, growing 26% year-over-year, up from 15.8 million at Q4 FY25 exit. Customer additions have been accelerating: 18.1% growth in FY24, 27.4% in FY25, with Q3 FY26 tracking at 26% year-over-year.

The customer base skews female (beauty is the core), urban, and increasingly spans income segments. Gen Z consumers account for 44% of BPC spending on Nykaa, reflecting the demographic tailwind behind this business: India’s young population is beauty-conscious, digitally native, and brand-aware.

Premium customers (top 10% by spend) account for a disproportionate share of revenue, spending approximately $395 annually (~₹33,000). The average customer spends much less. Nykaa’s economics improve as it converts casual buyers into premium, repeat customers.

On the supply side, Nykaa’s “customers” are the 8,600+ brands that sell through the platform. Key brand partners include the L’Oreal Group (L’Oreal Paris, Maybelline, NYX, Lancome, Kiehl’s), Estee Lauder Companies (Estee Lauder, MAC, Clinique, Bobbi Brown, Too Faced), LVMH (Sephora Collection, Dior, Givenchy), Chanel Beauty, Charlotte Tilbury, Huda Beauty, The Ordinary (DECIEM), Korean beauty brands (Innisfree, Laneige, COSRX), and domestic brands like Forest Essentials and Mamaearth. Nykaa has been launching 200-400 new brands per quarter, including global entrants using Nykaa as their India launch platform.

The Superstore by Nykaa B2B arm serves thousands of small retailers across India, giving them access to branded beauty inventory that they previously could not source directly.

Nykaa delivers to approximately 98% of India’s pin codes for online orders. Its 265 physical stores span 90 cities, from metros like Mumbai, Delhi, and Bangalore to tier-2 and tier-3 cities.

Products & services

Beauty and Personal Care (BPC) Products: The core business. Nykaa sells across the full spectrum of beauty: color cosmetics (lipsticks, foundations, mascaras), skincare (moisturizers, serums, sunscreens), haircare, fragrances, bath and body, personal care, and beauty tools and accessories. The platform carries mass market brands (Maybelline, Lakme, Nivea), premium brands (MAC, Clinique, The Ordinary), and luxury brands (Chanel, Dior, Estee Lauder). The beauty category contributes 75-76% of total GMV and is the most profitable segment.

House of Nykaa Owned Brands: Twelve proprietary brands, including Nykaa Cosmetics (color cosmetics and nail lacquers, one of the early owned brands), Kay Beauty (celebrity-backed, makeup and skincare co-created with Katrina Kaif, crossed ₹500 Cr annual GMV), Nykaa Naturals (personal care), Dot & Key (acquired skincare brand focused on vitamin C and hydration), Earth Rhythm (acquired clean/sustainable beauty brand), Wanderlust (bath and body), KICA (activewear), and fashion brands like Twenty Dresses and Gajra Gang. Owned brands collectively generate ₹2,100+ crore GMV at a run-rate and are the fastest-growing category (54% YoY in Q2 FY26).

The individual brand trajectories show Nykaa’s ability to scale owned brands rapidly. Dot & Key is the portfolio anchor, contributing roughly 60% of all owned BPC GMV with an annualized run-rate near ₹1,500 crore. GMV grew from ₹130 crore in FY22 to ₹450 crore in FY23, ₹900 crore in FY24, and approximately ₹1,500 crore by FY25. A ninefold increase in three years, with high-teens EBITDA margins throughout. Nykaa Cosmetics, the first owned brand launched in 2015, scaled from ₹110 crore in FY19 to ₹350 crore by FY25, reaching a ₹400 crore annualized rate by H2 FY26 (approximately 17-18% of owned BPC GMV). Kay Beauty moved from ₹70 crore in FY22 to ₹240 crore in FY25 and is now among the top five makeup brands sold on Nykaa.com. In the fashion vertical, both Twenty Dresses and Nykd have crossed the ₹100 crore GMV mark. Nykaa has scaled five owned brands to ₹100 crore+ GMV, demonstrating that the brand-building playbook is repeatable.

Nykaa Fashion: An online marketplace for apparel, footwear, and accessories, carrying over 5,000 brands and more than 12 million SKUs spanning women, men, kids, and home categories. This is a marketplace model (Nykaa does not hold fashion inventory). Fashion GMV was approximately ₹3,800 crore in FY25 (approximately ₹1,100 crore NSV), growing at a 55% GMV CAGR over FY21-25. Management’s stated ambition, is to grow fashion NSV 3-4x over the next five years, implying ₹3,300-4,400 crore in fashion NSV by FY30. On profitability, management guided for fashion EBITDA to reach breakeven in FY26, then improve to mid-to-high single digit margins by FY28, eventually reaching a steady-state of approximately 10%. A defining metric: at ₹4,651 AOV in Q2 FY26, Nykaa Fashion commands among the highest average order values in India’s online fashion space, reflecting premium curation rather than discount-driven volume. GMV from existing customers accounted for 57% of Fashion GMV (compared to 76% in Beauty), reflecting the relative nascency of the fashion customer base.

The H&M partnership, which launched in Q2 FY26, is specifically an online only arrangement (not offline retailing). Nykaa carries the entire H&M India assortment on its fashion platform, at pricing parity with H&M’s own website and offline stores. H&M became the #1 brand on Nykaa Fashion immediately upon launch, and served as the headline sponsor of Nykaa land. The partnership structure (Nykaa as H&M’s online marketplace partner, H&M retains its own offline stores and website) is a template management believes can be replicated with other large fashion brands. The Nike D2C arrangement follows a different, deeper model: Nykaa exclusively runs Nike.in and Nike’s iOS/Android commerce apps in India, handling on-site experience, digital marketing, fulfillment, and customer experience, with unit economics comparable to Nykaa’s core e-commerce business.

Nykaa Man: A dedicated vertical for men’s grooming products (skincare, haircare, shaving, fragrances), operating as a sub-brand within the beauty vertical.

Nykaa Now: A rapid delivery service (30 minutes to 2 hours) operating across 7 cities using 53 rapid store locations, including fulfillment from Nykaa Luxe stores. This competes with the growing quick-commerce trend in India. As of Q2 FY26, Nykaa Now had delivered over 2 million cumulative orders and offers 500+ brands, including luxury brands, making it the deepest beauty and personal care assortment among quick delivery platforms in India. Management plans to expand the service to 10 large cities and stop there, focusing only on metros with the highest beauty demand density rather than chasing national coverage.

Superstore by Nykaa: An eB2B distribution platform that sells beauty products to small, unorganized retailers across India. This has tripled GMV in two years and grew 53% in Q3 FY25. Management expects EBITDA break-even at approximately 4x the current scale, driven primarily by geographic expansion into lower-tier cities where retailers are most under-served by existing distribution infrastructure.

Nykaa Pro: Products and tools targeted at beauty professionals (makeup artists, salon owners).

Content Platform: Nykaa TV (video content), beauty blog, beauty book (editorial content), product reviews, and community features. This drives customer acquisition and engagement rather than direct revenue.

Brand Operations Services: An emerging revenue stream where Nykaa runs end-to-end operations for international brands in India. Recent examples include operating all of Kiehl’s India operations (digital, physical retail, and online sales) and managing Nike’s D2C platforms in India.

Industry overview

India’s beauty and personal care market is worth approximately $24 billion in FY25 (Redseer) and is expected to reach $40-45 billion by FY30, a ~12% CAGR. India is the fourth-largest BPC market globally, and its 10-12% CAGR dwarfs developed markets: UK at 1-3%, South Korea at 2-3%, Japan at 2-3%, US at 2-4%, China at 4-5%. Per capita spending on beauty remains a fraction of comparable economies. An Indian consumer spends around $22-23 per year on beauty products. A Chinese consumer spends roughly $55. An American spends over $300. That gap, combined with India’s demographics (median age of 28, 66% of the population under 35, 500 million women), is the foundational thesis behind every beauty investment in the country.

India’s e-retail market reached $60 billion in FY25, with 270-280 million online shoppers (the second-largest digital consumer base globally after China’s 920 million), and is projected to expand to $170-190 billion by FY30 at an 18% CAGR. India’s e-commerce penetration remains just 6-7%, compared to 25-30% in other Asian markets, providing meaningful headroom. Within this, Beauty + Fashion combined accounted for roughly 13% of the e-retail mix ($23 billion in FY25), projected to grow to $70-75 billion by FY30. The e-commerce shopper base is expected to expand at 20% CAGR to 400 million+ shoppers by FY30.

The market’s origins trace to a handful of multinational conglomerates. Hindustan Unilever (HUL) has dominated Indian personal care since the 1930s, building mass brands like Fair & Lovely (now Glow & Lovely), Lakme, Dove, and Pond’s through the deepest distribution network in the country, reaching millions of kirana stores across every village and town. Colgate-Palmolive captured oral care. Procter & Gamble brought Pantene and Olay. L’Oreal entered India in 1994, initially through salon channels, and gradually built a consumer business through brands like L’Oreal Paris, Garnier, and Maybelline. Dabur, Godrej Consumer, and Emami represented the domestic FMCG contingent, mostly in hair oils, soaps, and ayurvedic personal care.

For decades, the distribution structure was simple and resistant to disruption. India has approximately 13 million retail outlets (more than any country on earth), of which roughly 10-12 million are tiny kirana stores, many smaller than a parking space. These general trade (GT) stores account for 70-80% of all FMCG sales in India, including beauty and personal care. A woman in a tier-3 town buying Lakme kajal or Pond’s cold cream would walk to her nearest kirana, pick from the 3-5 brands the store stocked, and pay cash. There was no discovery, no comparison, no trial of new brands. The kirana owner stocked whatever the HUL or L’Oreal distributor pushed, and consumer choice was dictated by whatever happened to be on the shelf.

Modern trade (organized retail chains like Reliance Retail, DMart, Big Bazaar, Shoppers Stop) began making inroads in the 2000s and now represents roughly 18-20% of FMCG distribution. The organized vs. unorganized split tells a story of ongoing formalization: in FY24, organized players held 48% of the beauty market and just 34% of fashion, with the balance controlled by unbranded, regional, and unorganized players. By FY30, organized share is projected to reach 61% in beauty and 40% in fashion, according to Redseer, driven by D2C brand proliferation, e-commerce expansion, and modern retail growth. But modern trade’s relevance for beauty is uneven. Supermarkets and hypermarkets (Big Bazaar, DMart) sell mass personal care (shampoos, soaps, body lotions) well enough, but they are poor at selling premium color cosmetics, luxury skincare, or fragrances. These categories require a different retail environment: trained beauty advisors, testers, proper merchandising, and a curated brand assortment. Department stores like Shoppers Stop tried to fill this gap with dedicated beauty counters, and Sephora entered India in 2012 through a franchise with Arvind Fashions, but neither managed to build a large-scale specialty beauty retail network. Sephora reached only 26 stores in eleven years before Reliance Retail acquired its India operations in late 2023.

The BPC channel distribution is shifting decisively toward online. In FY25, unorganized offline (primarily general trade/kirana) still commanded 52% of the market, organized offline held 28%, and online accounted for 20%. By FY30, Redseer project unorganized offline will shrink to 34%, organized offline will hold 32%, and online will grow to 34% of the total BPC market. Convenience, selection breadth, and content-led discovery drive the shift.

The structural deficiency in India’s beauty distribution, the absence of a scaled specialty beauty retailer comparable to Sephora in the US (2,700 stores), Watsons in Asia (16,000+ stores), or even Boots in the UK, is precisely the gap Nykaa was founded to fill. When Falguni Nayar launched Nykaa in 2012, beauty e-commerce in India did not exist as a category. Amazon India had not yet launched (it started in June 2013). Flipkart was focused on electronics and books. Nobody was building a curated, beauty-specific online destination with authentic product guarantees.

Online penetration of BPC in India has risen from under 3% in 2015 to approximately 20-22% by FY25 according to Redseer, and is expected to approach 34-35% by FY30. The online BPC market itself is projected to reach $14-15 billion by FY30 (from $5 billion in FY25), representing a 23-25% CAGR, roughly 2x faster than the underlying industry growth rate. Compare this to China, where online accounts for 35-40% of beauty sales, or the US at 25-30%, or South Korea at over 40%. India’s online beauty penetration has quadrupled in under a decade, yet remains less than half of what mature markets have achieved. The Redseer report from February 2026 projects that new business models (quick commerce, value commerce) will capture 50% of e-commerce BPC market share by 2030, suggesting the channel mix will keep evolving rapidly.

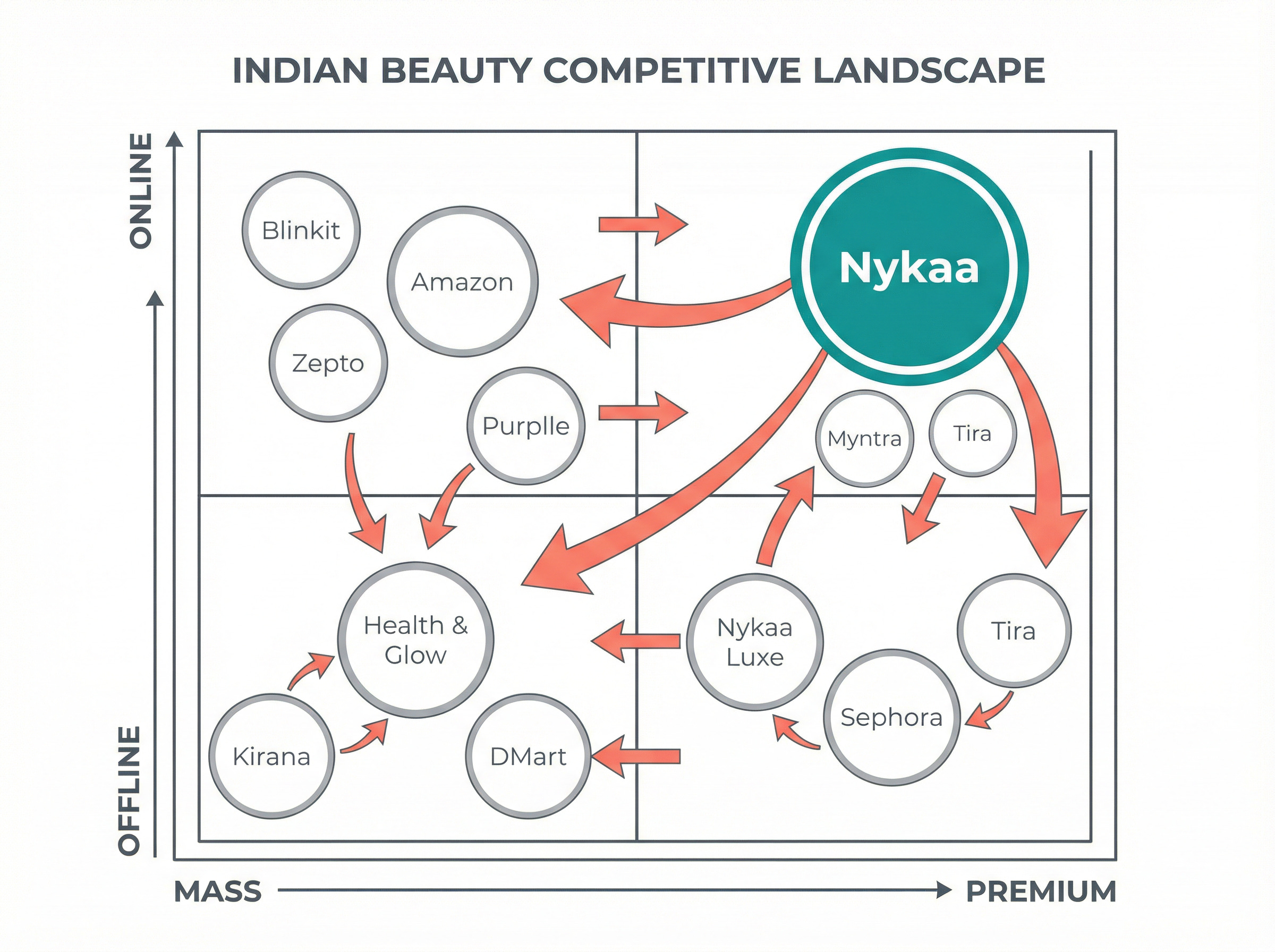

Competitive Landscape

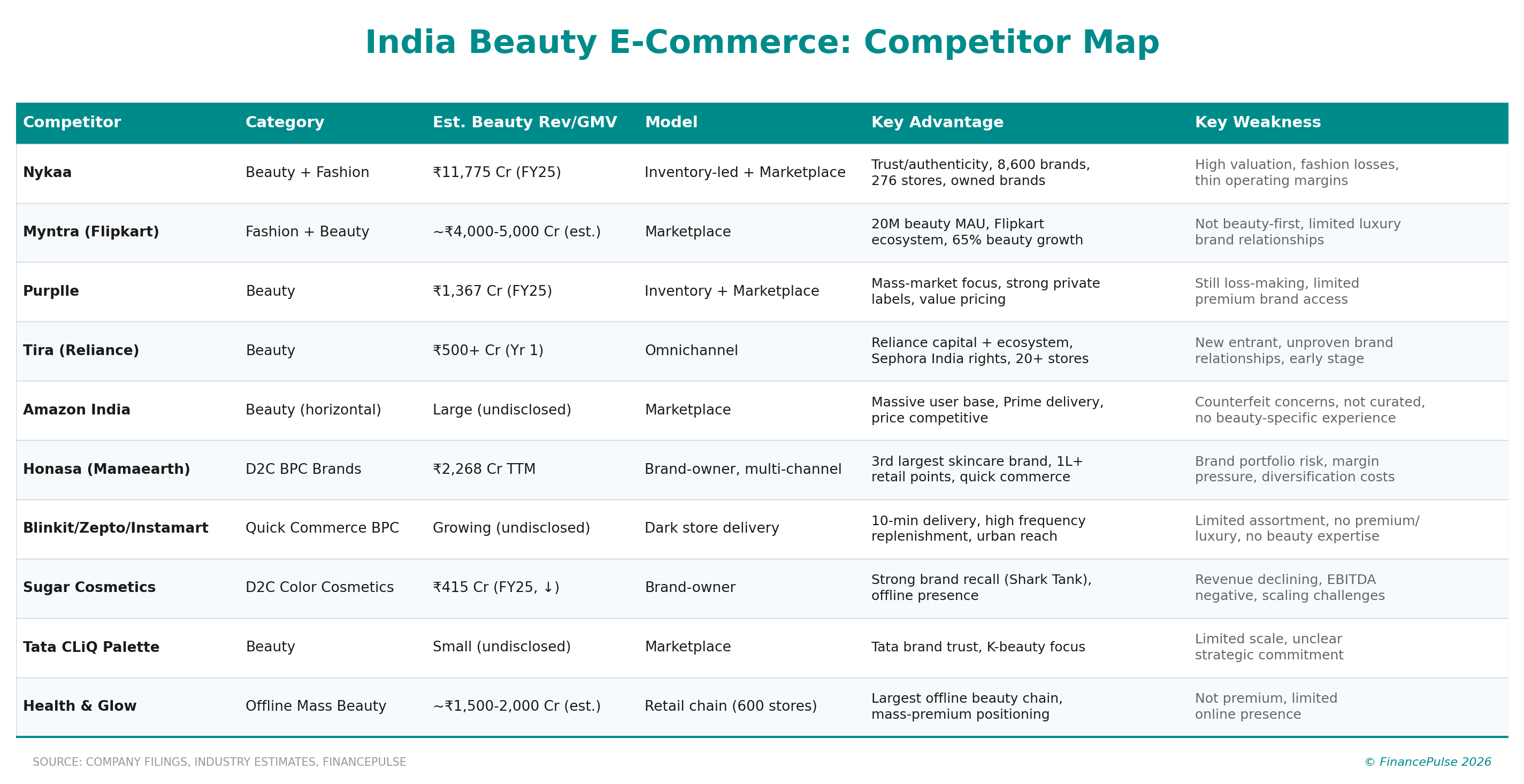

The competitive landscape for Indian beauty and personal care has transformed from a two-player story (Nykaa vs. everyone else online) into a multi front war involving horizontal e-commerce giants, well-funded vertical players, conglomerate-backed challengers, quick commerce disruptors, D2C brands building their own channels, and offline specialty retailers.

Nykaa’s online beauty dominance and who is chipping away at it. Nykaa holds approximately 27-28% of India’s online BPC market as of FY25 according to Redseer data, a share that peaked higher during the post-pandemic surge (reaching 31-32% in FY22) before normalizing as competition intensified and quick commerce emerged. The company retains a commanding lead over Amazon and Flipkart in online beauty, which together hold roughly 20%. Nykaa built this dominance on a simple insight that horizontal platforms struggled to replicate: beauty consumers care about authenticity, curation, and expert guidance, none of which Amazon or Flipkart are designed to deliver. When a consumer buys a ₹3,500 Estee Lauder foundation on Amazon, she cannot be certain whether the product is genuine, because Amazon’s marketplace model allows third party sellers to list products without the same authentication controls that Nykaa’s inventory-led model provides. Reddit threads on Indian skincare forums are filled with stories of consumers receiving expired, opened, or suspected-counterfeit beauty products from Amazon and Flipkart. Nykaa’s zero-counterfeit guarantee, backed by direct purchasing from brands or authorized distributors, created a trust moat that horizontal platforms have spent years trying to crack.

Amazon India has invested heavily in beauty, launching the Amazon Beauty category with dedicated storefronts, the Amazon Premium Beauty section for luxury brands, and programs like Brand Registry to combat counterfeits. Amazon offers faster delivery through Prime and often undercuts Nykaa on price. Flipkart’s beauty efforts have been more muted on the mainline platform, but Flipkart-owned Myntra has emerged as a formidable beauty competitor. Myntra’s beauty segment now attracts 20 million monthly active users, representing 30% of Myntra’s total user base, and beauty accounts for 20% of Myntra’s new customer acquisition. Myntra’s beauty category grew at 65% year-over-year through 2025, with skincare and fragrance sales increasing 60% and 50% respectively. Myntra CEO Nandita Sinha has publicly framed beauty as a strategic acquisition tool, using beauty’s high purchase frequency to draw consumers into Myntra’s fashion ecosystem.

Purplle: the scrappy challenger. Purplle, founded in 2011 (a year before Nykaa), took a different path. While Nykaa targeted the premium and aspirational consumer from the start, Purplle focused on mass market and value conscious beauty buyers. Purplle’s revenue doubled to ₹1,367 crore in FY25 (from ₹650 crore in FY24), and it has raised $560 million in total funding at a $1.3 billion valuation. Purplle’s strategy centers on private labels. Brands like Faces Canada (acquired), Carmesi, and Purplle-exclusive labels generate higher margins than third-party brands. Purplle is not trying to out-Nykaa Nykaa on luxury. It is building a mass beauty platform targeting Indian consumers who want good quality beauty products at accessible price points.

Reliance Retail’s Tira: the conglomerate assault. Reliance Retail, India’s largest retailer with $35 billion+ in annual revenue and 18,000+ stores, launched Tira in April 2023, a dedicated beauty platform that directly targets Nykaa’s core positioning. Tira achieved ₹500+ crore GMV in its first year, opened over 20 experiential stores, and partnered with 50+ luxury brands including MAC, Dior, and Charlotte Tilbury. Reliance also acquired Sephora India’s 26 stores and operating rights from Arvind Fashions in late 2023 for ₹99 crore, giving it an instant footprint in luxury beauty retail. Reliance’s Tira strategy uses the company’s ecosystem: integration with Jio (India’s largest telecom network, 450 million subscribers), Ajio (Reliance’s fashion platform), and the physical retail network. Tira uses AI-powered tools (fragrance finder, skin analyzer) and emphasizes “phygital” experiences that connect online browsing with in-store trial. Tira also launched private labels (Tira Tools, Nails Our Way) in its first year, mimicking the private label playbook that Nykaa has used to expand margins.

The quick commerce front. The most disruptive competitive force in Indian beauty today may not be another beauty platform at all. Blinkit (Zomato-owned), Zepto, and Swiggy Instamart collectively represent India’s quick commerce revolution, delivering products in 10-30 minutes through networks of “dark stores” (small urban warehouses). The quick commerce market exploded from $300 million in 2022 to $7.1 billion in 2025, growing roughly 40% annually, and is projected to reach $35 billion by 2030. Blinkit holds approximately 45-50% quick commerce market share, with Zepto at 25-30% and Swiggy Instamart at 20-25%.

Beauty and personal care is one of the fastest growing categories on quick commerce platforms. When a consumer needs to replenish her face wash, shampoo, or sunscreen, the 10-minute delivery promise from Blinkit is more compelling than waiting a day or two for Nykaa to ship. A Redseer study from February 2026 projected that quick commerce and value commerce will account for 50% of e-commerce BPC market share by 2030, a dramatic shift from the current landscape where specialized platforms like Nykaa dominate. Quick commerce is strongest in replenishment purchases (the everyday shampoos, body washes, moisturizers, and deodorants that consumers buy regularly at known price points). It is weaker in discovery driven purchases (trying a new Korean serum, choosing a lipstick shade, buying a luxury fragrance), which require the curation, reviews, and visual merchandising that Nykaa excels at. Nykaa’s response has been Nykaa Now, its own rapid delivery service operating in 7 metros with 53 rapid stores and 30-120 minute delivery. The service carries a broader beauty assortment than any quick commerce platform can stock in a dark store, but it cannot match Blinkit’s 10-minute speed or ubiquitous presence.

The real question is where the boundary lies between “beauty as commodity” (replenishment, mass personal care, quick commerce territory) and “beauty as experience” (discovery, premium, luxury, Nykaa territory). If quick commerce creeps upmarket into premium brands, Nykaa’s mass-beauty business faces genuine pressure. If it stays focused on shampoo-and-body-wash replenishment, Nykaa’s core premium positioning remains insulated.

D2C brands: partners and competitors simultaneously. India’s direct-to-consumer beauty brand explosion created a paradoxical dynamic for Nykaa. Brands like Mamaearth (Honasa Consumer, listed on NSE, ₹2,268 crore TTM revenue), Sugar Cosmetics (₹415 crore revenue in FY25, down 17.8% year-over-year), Minimalist, Plum, mCaffeine, Dot & Key (acquired by Nykaa), Pilgrim, and The Derma Co (owned by Honasa) built their initial followings through Nykaa’s platform, benefiting from Nykaa’s traffic, discovery tools, and authenticity guarantee. Many then expanded into their own D2C websites, Amazon, Myntra, quick commerce, and offline distribution, reducing their dependency on Nykaa.

Honasa Consumer (Mamaearth’s parent) is the most instructive case. Founded in 2016, Honasa built Mamaearth into India’s third-largest skincare brand by 2023 (per Euromonitor) through an aggressive online-first strategy, expanding to ₹2,067 crore revenue in FY25. But Honasa has been diversifying away from Nykaa-dependency: building its own D2C channels, expanding into 1,00,000+ offline retail points, acquiring brands (BBlunt, Dr. Sheth’s, The Derma Co), and growing on quick commerce. Honasa’s Q2 FY26 concall revealed that offline channels now contribute over 40% of revenue, and quick commerce is growing rapidly as a channel. Honasa’s EBITDA margins have recovered to 8-11% after a rocky FY25 (which included an inventory write-down quarter), and the company trades at a ₹9,756 crore market cap with a 61x P/E.

For Nykaa, the D2C explosion is a double-edged sword. Brands that grow on Nykaa and then diversify away weaken Nykaa’s bargaining power. But brands that grow anywhere ultimately need Nykaa for discovery and premium positioning. Nykaa’s response has been to acquire high-potential brands (Dot & Key, now a ₹1,900 crore GMV brand growing 100%+, Earth Rhythm), build proprietary brands (Kay Beauty, Nykaa Cosmetics), and position itself as the indispensable “brand-building” platform that D2C brands cannot afford to ignore even as they diversify.

Tata CLiQ Palette launched as Tata Group’s answer to Nykaa, a dedicated beauty vertical within the Tata CLiQ e-commerce ecosystem. Backed by Tata’s consumer trust (one of India’s most trusted conglomerate brands) and using Tata’s retail network (Westside, Zudio, Croma), Palette offered curated premium beauty with a focus on K-beauty and niche international brands. In practice, Palette has struggled to gain meaningful scale against Nykaa’s first-mover advantage and comprehensive brand assortment. Tata Group has not publicly disclosed Palette-specific financials, but industry observers note that it remains a small player relative to Nykaa and Tira.

Offline competition. The offline beauty landscape in India is fragmented and underserved, which is both a risk and an opportunity for Nykaa’s physical retail expansion. Shoppers Stop, India’s leading department store chain (approximately 100 stores), has dedicated beauty departments carrying premium brands, but its format is built around apparel, not beauty. Shoppers Stop’s beauty business cannot replicate the depth of assortment or the beauty focused experience that Nykaa Luxe stores provide. Health & Glow, a Chennai-based chain owned by A.S. Watson Group (the world’s largest health and beauty retailer, with 16,000+ stores globally), operates around 600 stores focused on mass and mass premium beauty and personal care. Health & Glow is the closest analog to a scaled offline beauty specialty retailer in India, but it positions itself lower on the price spectrum than Nykaa and lacks the premium brand relationships that define Nykaa’s retail experience.

Nykaa’s 276 stores across 94 cities (as of Q3 FY26) make it India’s largest specialty beauty retail network by a wide margin. No competitor has comparable scale in dedicated beauty retail. The store formats, ranging from Nykaa Luxe (premium/luxury brands, beauty advisors, makeover services) to Nykaa On Trend (mass-premium) to new concepts like Nykaa Perfumery (fragrance-only stores) and Kay Kafe (beauty-meets-coffee experiential format), are specifically designed for beauty, unlike department store counters or general trade shelves. Management targets 500 stores across 100+ cities by FY30, adding roughly 50 stores per year, all profitable or breakeven within the first year.

The fashion war. Nykaa Fashion competes in India’s online fashion market. The total fashion market is approximately $100 billion in FY25, with online fashion at roughly $18 billion (18% online penetration), projected to reach $55-60 billion by FY30 (30% online penetration) at a 22-25% CAGR. India’s online premium fashion market specifically is expected to grow at a 25-30% CAGR over FY25-30, with the premium segment expected to triple from $3.3 billion (FY25) to $10 billion (FY30). The fashion market remains over 60% unorganized and unbranded, compared to roughly 40% in beauty, meaning the formalization opportunity in fashion is even larger than in BPC. This is a vastly more competitive arena than beauty. Myntra (Flipkart-owned) is the clear leader in online fashion, with strong brand partnerships, a 20 million+ MAU beauty vertical on top of its fashion core, and a recently profitable business (roughly $62 million net profit in FY25). Ajio (Reliance-owned) has grown aggressively on the back of deep discounting and curated international brand selection. Flipkart’s mainline fashion vertical, Amazon Fashion, and Meesho (focused on value fashion for Tier 2-3 cities) round out a crowded field.

Nykaa Fashion’s competitive positioning is it targets the premium, fashion-forward woman who is already a Nykaa beauty customer. But fashion e-commerce in India is notoriously unprofitable, margins are thin, return rates are high (30-40% in apparel versus under 5% in beauty), and customer acquisition requires constant spending. Nykaa Fashion’s EBITDA loss narrowed from -9.2% in Q1 FY25 to -2.0% in Q3 FY26, and management guided for breakeven by March 2026. The H&M launch on Nykaa Fashion (H&M became the #1 brand on the platform immediately) and the Nike D2C partnership (Nykaa exclusively running Nike.in and Nike’s commerce apps in India) validate the platform’s premium positioning but do not resolve the fundamental question of whether a beauty led platform can build a sustainably profitable fashion business against Myntra’s scale advantages.

Growth triggers

Beauty platform - penetration & premiumisation flywheel

India remains one of the most under penetrated beauty markets globally; management repeatedly frames this as multi year runway for mid-20s+ GMV growth.

Premium beauty categories (cosmetics, fragrances) expanding at 13-15% CAGR, outpacing mass personal care; Nykaa’s owned BPC brands now contribute 18% of BPC GMV, providing a structural margin tailwind.

Owned brands (house of nykaa) - the margin engine

Owned brands have structurally higher gross margins than marketplace retail, improving overall beauty vertical profitability as mix tilts toward them. Currently 44% of beauty brands revenue comes from outside nykaa ecosystem.

Nykaa plans to focus the next wave of owned brand growth on three emerging categories: fragrances (Moi by Nykaa), bath and body (Wanderlust), and clean beauty (Earth Rhythm), all of which have large TAMs and fit the premiumisation trend.

Nykaa now (quick commerce) - expanding share of wallet

Live in all 7 tier 1 metros with 53+ rapid stores; largest beauty & personal care assortment across quick delivery platforms (30min to 2hr promise)

“significant percentage” of orders in live cities now fulfilled through Nykaa Now; plan to expand operational hours and number of cities

physical retail - the omnichannel moat

276 stores across 94 cities as of Q3FY26 (vs 237 stores in 79 cities at Q4FY25 exit); targeting 100+ cities; adding 50 stores/year, all profitable/breakeven within first year.

healthy double digit like-for-like growth; 2.8 lakh sq ft retail space; stores serve as premiumisation engines (2/3 of store GMV from premium brands)

kay kafe: beauty + coffee + community lifestyle concept targeting younger audiences; brand experiential format

key Risks

Competition from horizontal e-commerce platforms. Amazon India and Flipkart are investing heavily in beauty. They lack the curated experience and brand trust Nykaa has built, but they have far larger user bases and deeper pockets for customer acquisition. If they successfully address counterfeits (through programs like Amazon’s Brand Registry) and improve the beauty shopping experience, they could erode Nykaa’s share of mass market beauty purchases. Tata CLiQ and Reliance-backed platforms also represent well funded threats.

Quick commerce threat. Blinkit (Zomato), Zepto, Swiggy Instamart, and BigBasket are expanding into beauty and personal care. For replenishment purchases (shampoos, face wash, moisturizers), 10-minute delivery is a compelling value proposition that Nykaa’s 30-120 minute Nykaa Now cannot fully match. If quick commerce platforms successfully move up the beauty value chain into premium products, this could pressure Nykaa’s mass-beauty business.

Nykaa Fashion profitability. The fashion vertical has been loss-making since inception and still runs at -2% EBITDA margin. Management has guided for breakeven by FY26, but fashion e-commerce in India is brutally competitive (Myntra, Ajio, Flipkart Fashion) and heavily discount-driven. If fashion fails to reach profitability and requires continued investment, it drains capital that could be deployed in the high-return beauty business. Beauty’s return rates run 3-6%, keeping reverse logistics costs trivial. Fashion apparel returns typically run 30-35%, and even luxury fashion sees 15-20% return rates. Each returned fashion item eliminates the entire contribution margin of that sale and adds reverse logistics cost. The fashion segment also lacks Nykaa’s authenticity moat, because the marketplace model (where brands list and fulfill their own inventory) does not provide the same product guarantee differentiation that the inventory led beauty model delivers.

Founder concentration. Falguni Nayar and family (son Anchit runs Beauty, daughter Adwaita runs Fashion) hold 52.1% of the company. This is a family run business with professional management, but key person risk exists. Falguni Nayar’s personal relationships with global beauty conglomerates are a genuine competitive asset. How portable those relationships are remains unclear.

Discount dependency and ad load risk. Nykaa periodically runs sale events (Nykaa Pink Friday, Hot Pink Sale) to drive order volumes. If the industry moves toward heavier discounting (driven by well-funded competitors), it would compress Nykaa’s margins. Management says it is reducing discounting dependency, but competitive pressure may force their hand.

Valuations