Sterlite Technologies

How India's Optical Fiber Manufacturer Is Positioned for the AI Data Centre Supercycle

Before we begin - check out Growth Triggers & for more of me follow on X (Twitter)

Sterlite Technologies (stl) makes the physical infrastructure that carries the world’s data. The core product is glass - specifically, optical fibre drawn from pure silicon dioxide, turned into cables, and shipped to telecom operators, data centre operators, and internet service providers across more than 100 countries. When a british telecom engineer cables a street cabinet for fibre-to-the-home, or when a hyperscaler in virginia connects two server racks, the glass they are pulling through ducts is very likely made in aurangabad or silvassa.

The company was founded in 1988 as a copper cable manufacturer in aurangabad by the agarwal family - the same family that controls vedanta resources. The telecom division was formally demerged from sterlite industries in 2001 and relisted as sterlite technologies. The pivot from copper to optical fibre happened incrementally through the 1990s as stl built an optical fibre plant in aurangabad in 1995 and an optical fibre cable unit in silvassa in 1993. The critical transformation happened in 2016 when stl divested its power transmission segment entirely to focus purely on optical networking and digital infrastructure.

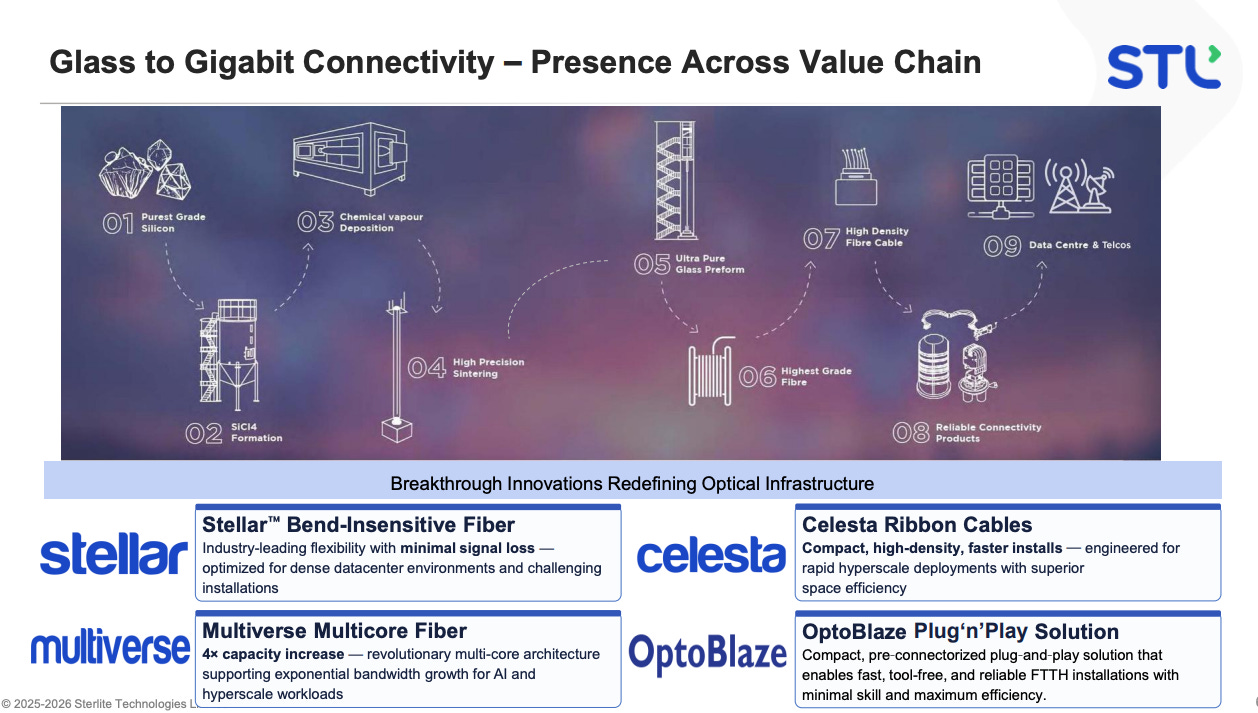

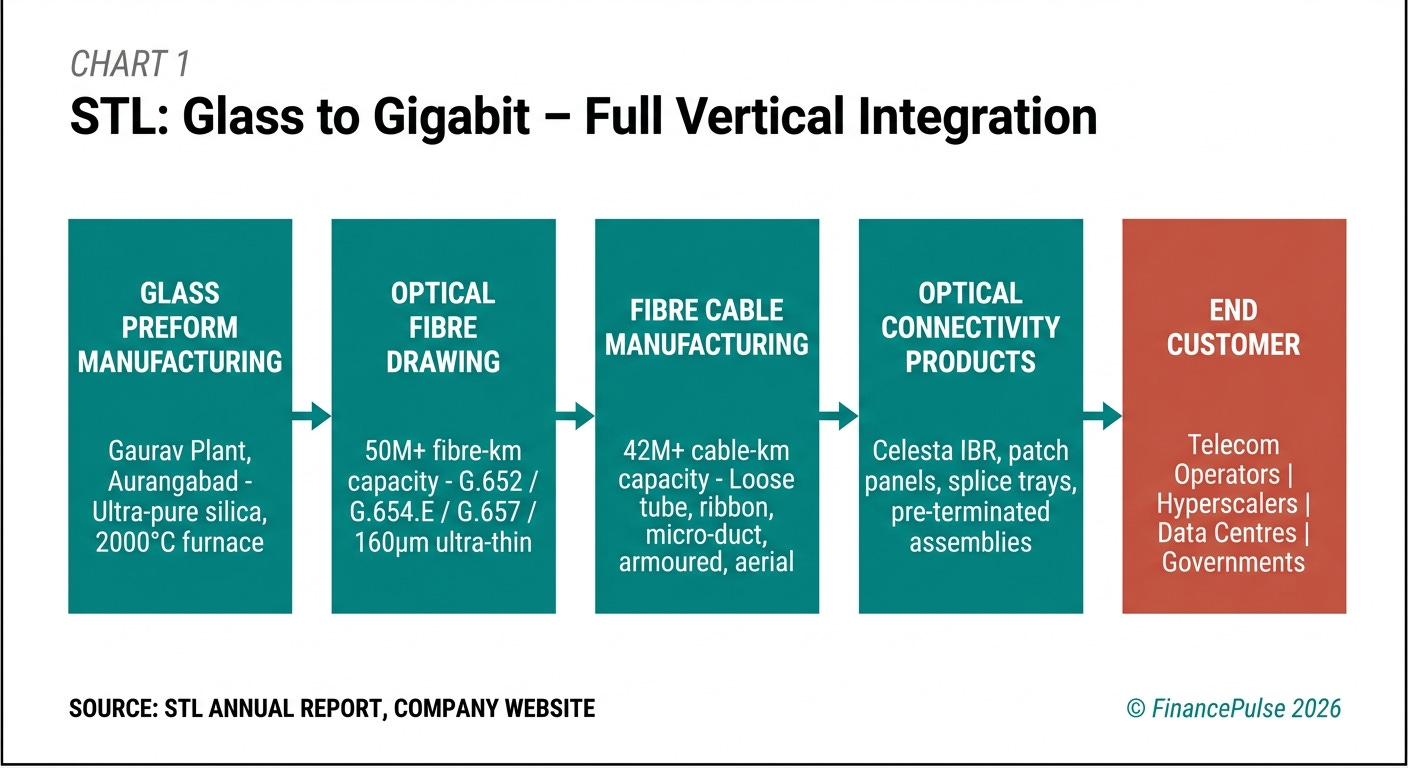

What makes stl structurally different from a pure cable reseller is backward integration. most optical fibre cable companies buy optical fibre from suppliers and cable it up. stl starts one step earlier - it manufactures optical fibre from glass preforms, the cylindrical slugs of ultra-pure silica from which fibre is drawn. The preform plant “gaurav” in aurangabad is one of the largest greenfield semiconductor-grade preform facilities in the world. Drawing fibre from preform requires extremely precise furnace control - the glass must be heated to approximately 2000 degrees celsius and drawn at speeds of up to 2000 metres per minute, with the resulting strand thinner than a human hair. stl has mastered this process and owns it end-to-end from raw glass to finished cable. This “glass to gigabit” vertical stack is the source of its cost leadership in india and its margin structure globally.

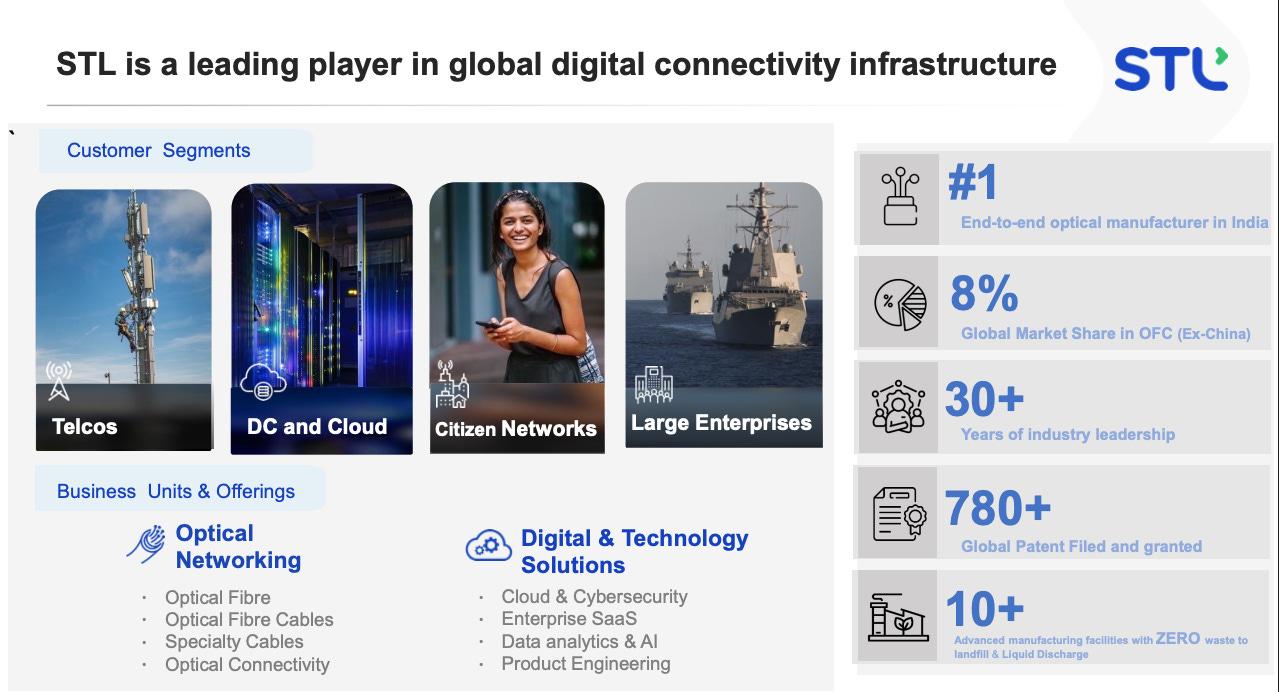

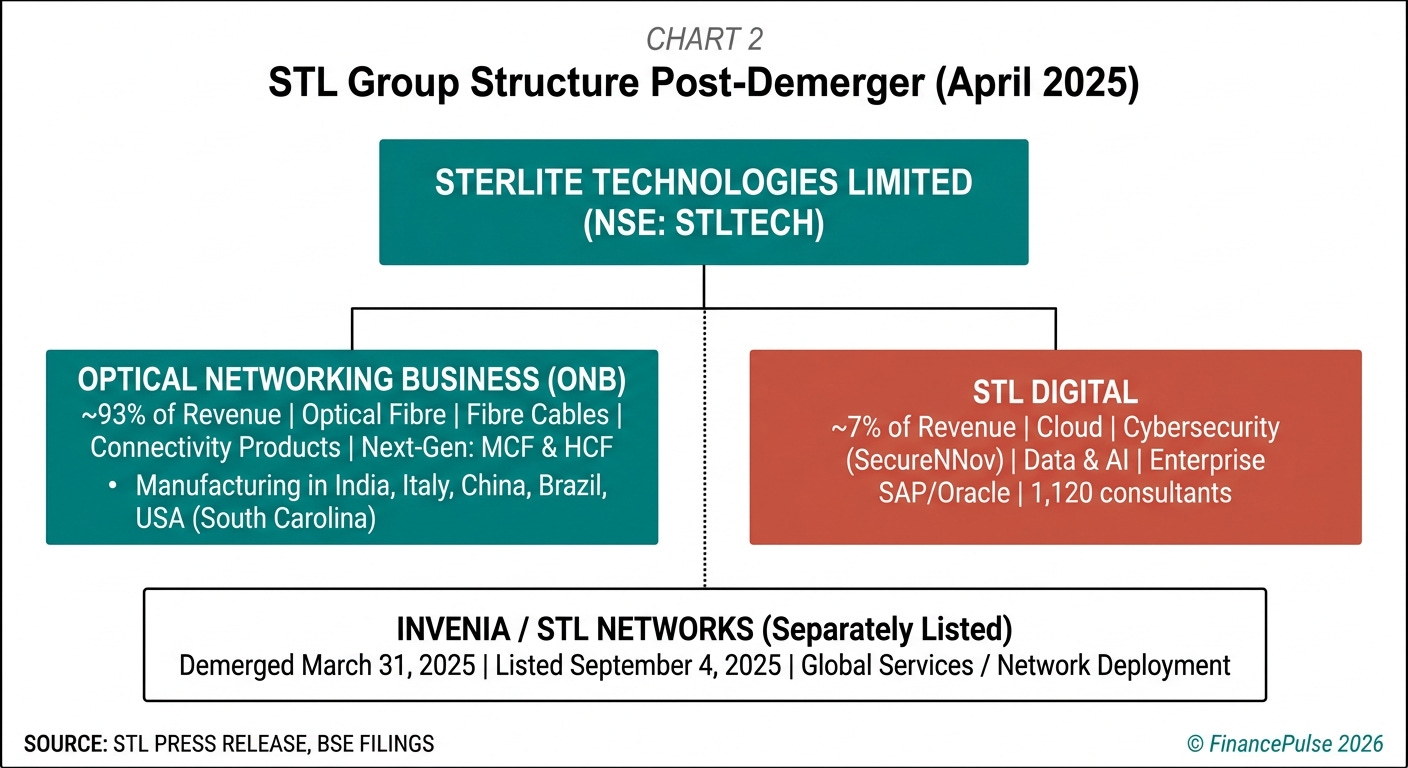

Post the april 2025 demerger of its global services business (now listed as invenia - stl networks), stl today operates as a focused optical networking and digital solutions company. The global services business - which built bharatnet middle-mile infrastructure and deployed fibre networks for telcos - has been separated into a distinct listed entity. What remains in stl is the manufacturing and technology business, supplemented by stl digital, a small IT services arm.

Business Segments

Optical networking business (ONB)

The optical networking business is the core of stl. it accounts for roughly 93% of revenues post-demerger and encompasses everything from optical fibre and fibre cables to specialty cables and optical connectivity products.

What it does: the onb designs and manufactures optical fibre, optical fibre cables of every configuration (loose-tube, ribbon, tight-buffered, aerial, armoured, micro-duct), specialty cables (ultra-thin 160-micron fibre for high-density applications, ribbon cables like the celesta ibr that packs 864 fibres in an 11.7mm diameter), and optical connectivity hardware (patch panels, splice trays, pre-terminated assemblies, fibre management systems). It also makes multiverse multi-core fibre (mcf) - a next-generation product where multiple cores are embedded in the same cladding as a standard fibre, multiplying capacity without multiplying cable count.

The core capability: making optical fibre at scale with consistent quality is harder than it looks. The preform-to-fibre process involves thousands of variables - draw speed, tension, coating thickness, refractive index profile, attenuation - and any deviation means scrap or quality rejection. stl has invested in machine learning models to optimise preform-to-fibre matching (a documented collaboration with mathworks). the result is lower scrap rates, lower cost per fibre-kilometre, and consistent compliance with itut standards that tier-1 operators like british telecom demand.

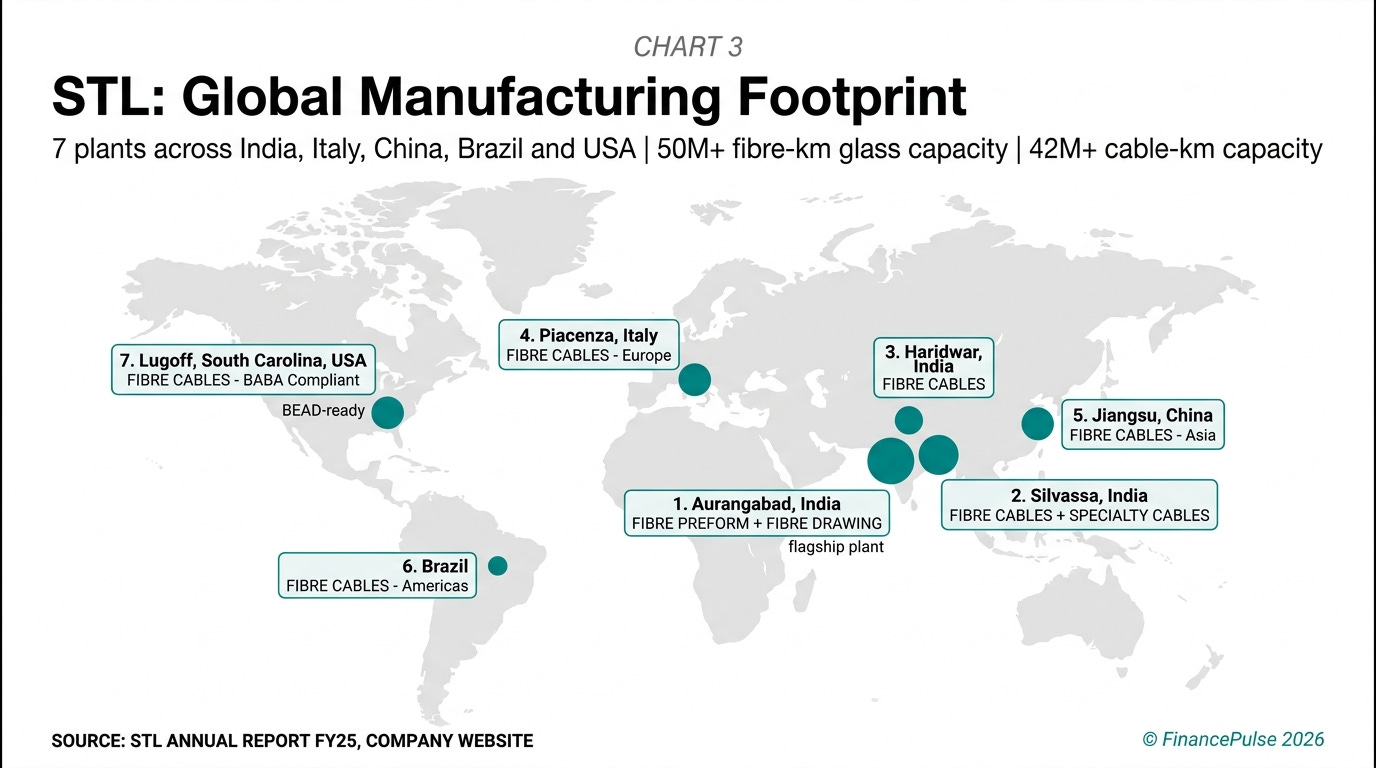

Why it exists as the primary segment: Optical networking is the reason stl exists. After the 2016 power segment divestiture and the 2025 global services demerger, this is the business. It has over 10 global manufacturing plants - india (aurangabad, silvassa), italy (acquired optotec spa), china (jiangsu sterlite tongguang fiber, fully acquired in 2022), brazil, and a manufacturing facility in lugoff, south carolina (sterlite technologies inc., or sti). The south carolina plant was specifically built to comply with the us “build america, buy america” (baba) provisions required for eligibility in the federal bead broadband infrastructure programme.

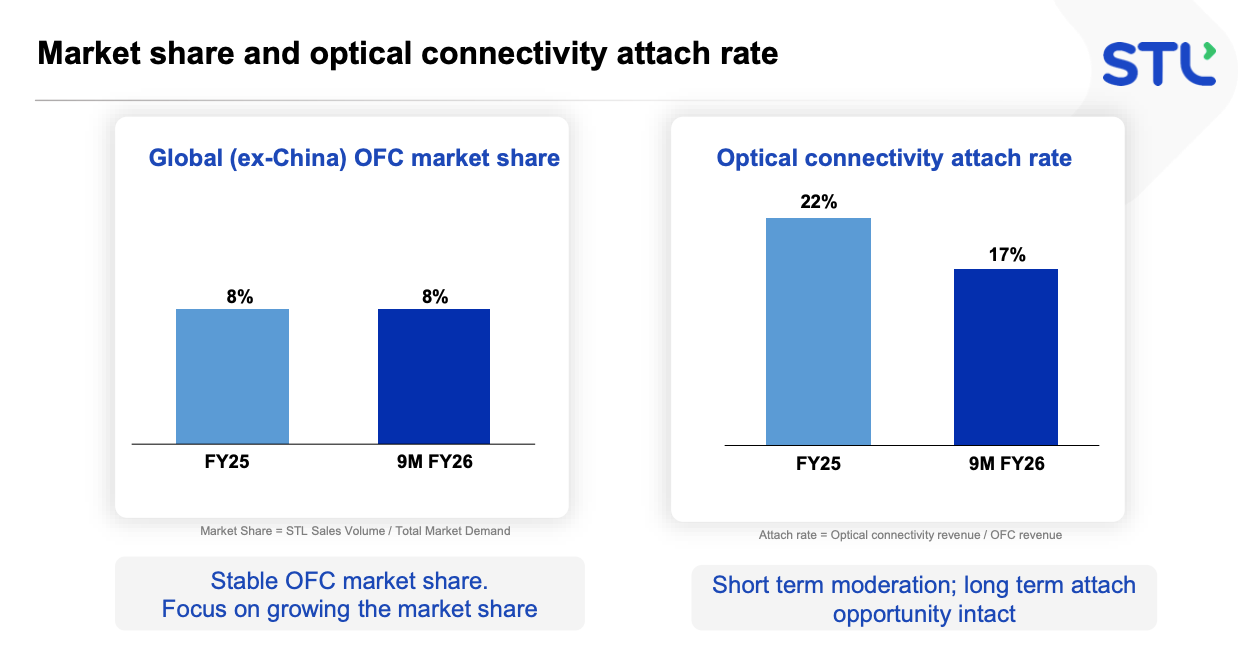

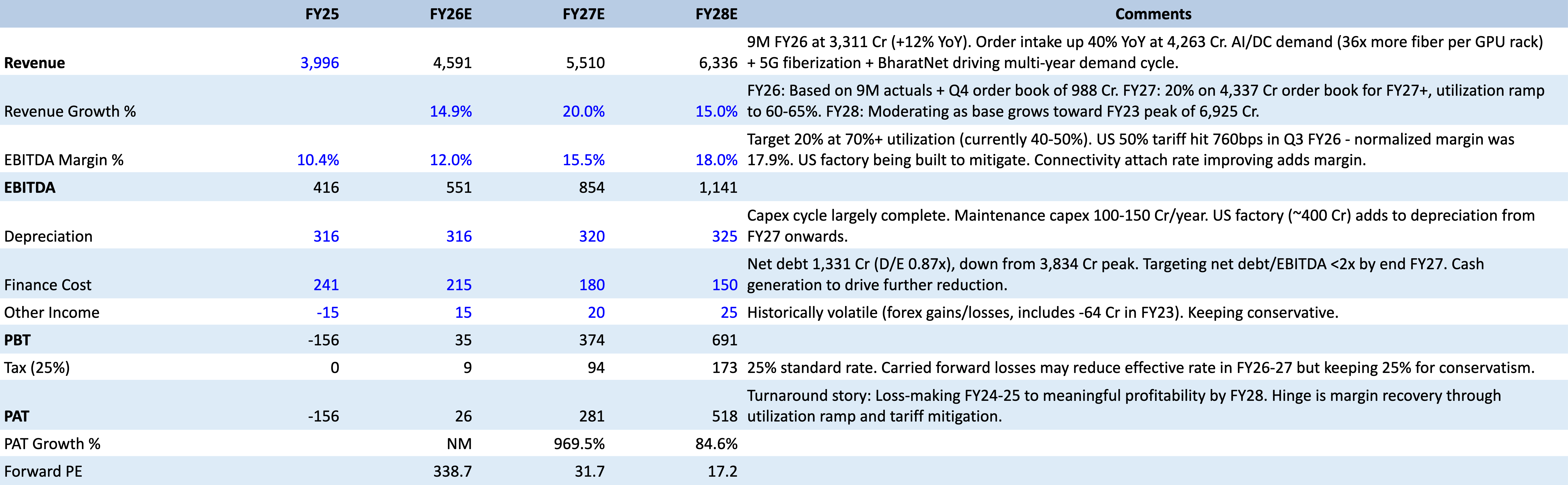

Competitive position: stl claims 8% market share in the global ex-china optical fibre cable market (per q4 fy25 concall, may 2025), down from 12% in fy23. The market share decline reflects the 2022-2024 global inventory correction where north american carriers drew down existing stock before placing new orders - a systemic issue, not specific to stl. The company operates at roughly 50% utilisation of its 50+ million fibre-km glass/fibre capacity and 42+ million fibre-km cable capacity (per q3 fy25 concall, january 2025). As the global upcycle begins, utilisation recovery is the primary margin driver.

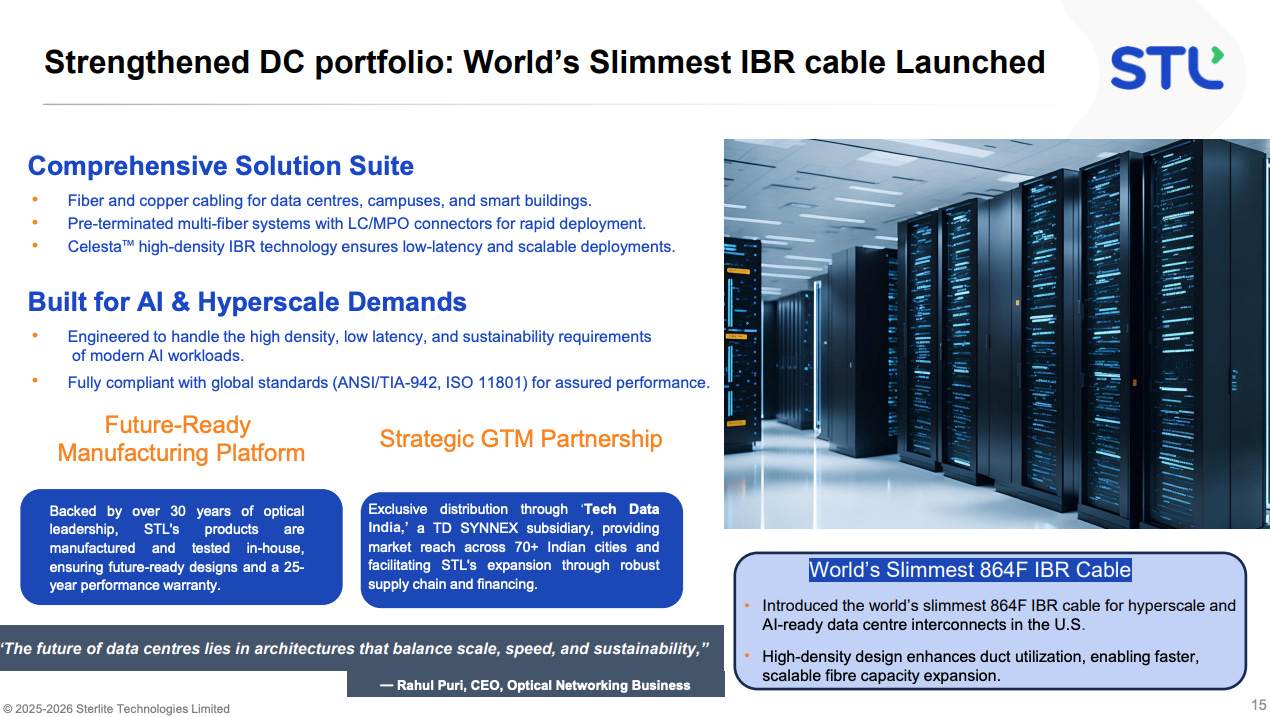

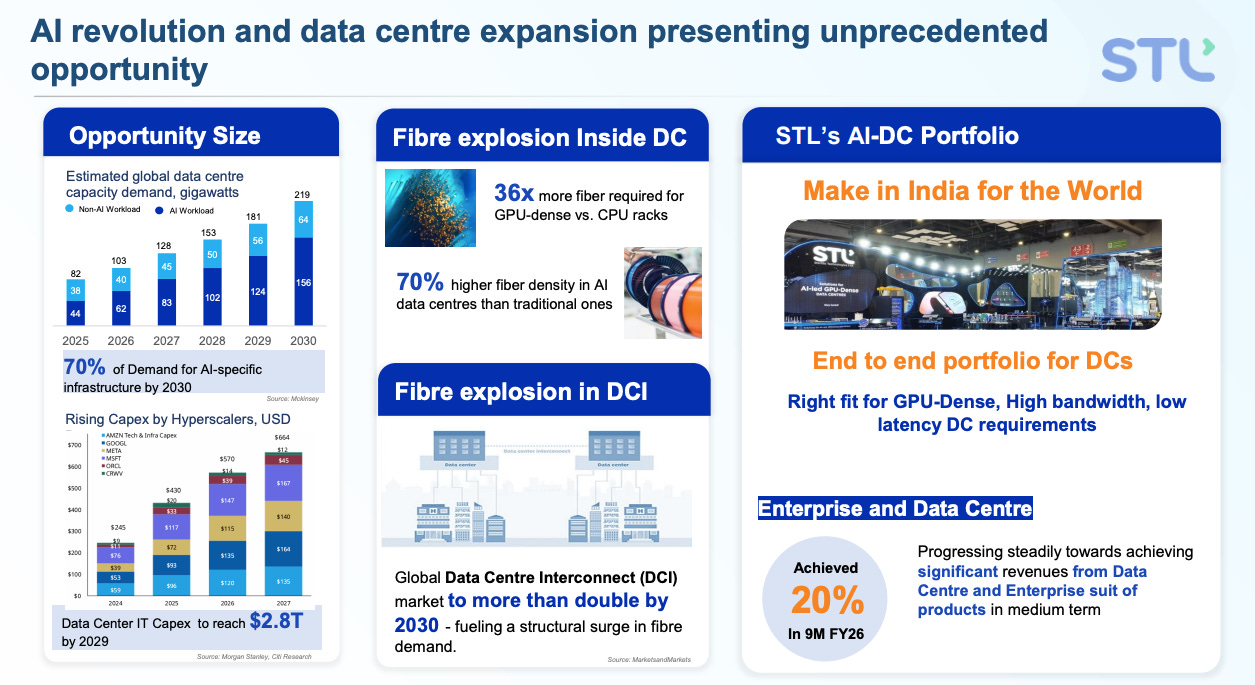

The data centre sub-segment within onb has become the growth story within the segment. Enterprise and data centre revenue contributed 20% of stl’s ytd fy26 revenues, and management has guided for this to reach 30% over the next 12-18 months. The reason is an ai data centre uses significantly more fibre per rack than a conventional cloud data centre - gpu-dense compute clusters require high-bandwidth, low-latency intra-facility connectivity that demands high-density fibre solutions. stl’s celesta ibr cable, launched in q2 fy26, is specifically engineered for this environment - 864 fibres in a sub-12mm diameter, optimised for jetting in micro-ducts inside data halls.

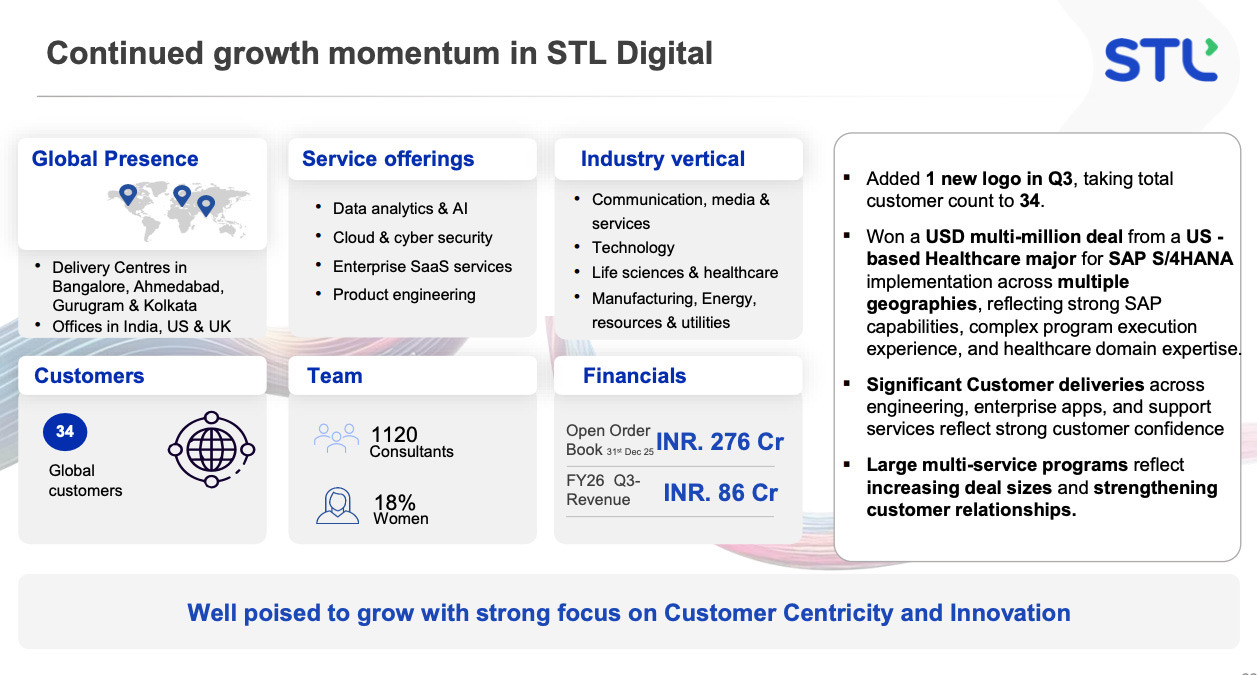

STL Digital

STL digital is a wholly owned it services and consulting subsidiary. It provides cloud migration, cybersecurity, data analytics, ai services, and enterprise saas (sap and oracle implementations) to enterprises across communications/media, healthcare, life sciences, energy, and manufacturing sectors. It has delivery centres in india, the us, and the uk, and a team of 1,120 consultants as of q3 fy26.

What it does: It is not a pure telecom IT shop. it does traditional enterprise IT - sap s/4hana implementations, oracle erp, cloud migration on aws/azure/gcp, cybersecurity managed services. March 2026 launch of securennov, an ai-driven cybersecurity portfolio, signals a push toward a differentiated product-led offering rather than purely staff augmentation.

The core capability: The connection to stl’s optical networking heritage gives stl digital a specific niche in communications and media technology - building bss/oss systems and digital transformation programmes for telecom operators. That is genuinely differentiated versus a generalist IT firm. but the healthcare and life sciences vertical is a pure enterprise it play with no natural stl advantage.

Products and Business Detailed

Optical fibre is the most upstream product. stl draws single-mode fibre from preform at its aurangabad facilities, compliant with itut g.652 (standard singlemode), g.654.e (ultra-low loss, long-distance), and g.657.a1 nova (bend-insensitive, access networks). Each fibre type solves a different problem: g.652 is the workhorse for backbone networks, g.654.e is used in submarine and long-haul routes where every 0.1db of attenuation matters, and g.657 bends around tight corners in homes and offices. stl also makes ultra-thin 160-micron and 180-micron fibre - 37% thinner than standard 250-micron fibre - which allows cable manufacturers to pack more fibre into smaller ducts, critical for dense urban deployments where duct space is exhausted.

Optical fibre cables (ofc) convert raw fibre into deployable products. stl makes loose tube cables (the standard outdoor backbone cable), ribbon cables (stacks of flat fibre ribbons for high-density applications), tight-buffered cables (for indoor use), micro-duct cables (ultra-slim for blowing through ducts with compressed air), armoured cables (for direct burial), and aerial cables (self-supporting with integrated messenger wire). the celesta ibr (intermittent bonded ribbon) launched in q2 fy26 packs 864 fibres in an 11.7mm diameter - described by management as “the world’s slimmest” at that fibre count - which is specifically for ai data centre intra-building high-density deployments.

Specialty cables include military-grade, subsea-armoured, and industrial variants. stl’s dadra facility produces specialty cables and has received near-zero waste to landfill intertek certification.

Optical connectivity products include pre-terminated assemblies, patch cords, fibre management systems, splice trays, and high-density celesta ibr technology enclosures. the “optical connectivity attach rate” - the percentage of stl’s fibre cable revenue that also carries connectivity product revenue - hit 22% in fy25 (per q4 fy25 concall, may 2025) before moderating to 17% in ytd fy26, primarily due to project timing and product mix shifts. management wants to grow this attach rate to 30%+ over time because connectivity products carry meaningfully higher margins than bulk cable.

Next-generation products include:

multi-core fibre (mcf): stl’s “multiverse” mcf embeds 4 cores in the same cladding diameter as standard single-mode fibre. it successfully trialled with colt technology services on the london metro network in january 2026, carrying 800 gbps line rate over 9km and 63km segments.

hollow core fibre (hcf): announced in march 2026, this is india’s first hollow core fibre hybrid cable. light travels through an air-filled core rather than solid glass, enabling speeds 46% faster than standard fibre with dramatically lower latency. badri gomatam, stl’s cto, described it as “the speed-of-light infrastructure required for the ai revolution.” hcf is commercially nascent but positions stl for hyperscaler and ai data centre applications where latency is the primary constraint.

Manufacturing footprint:

aurangabad, maharashtra: optical fibre preform and optical fibre manufacturing (the core of the glass-to-gigabit chain)

silvassa, dadra and nagar haveli: optical fibre cable and specialty cable manufacturing

haridwar, uttarakhand: additional cable manufacturing

piacenza, italy: acquired via optotec spa - serves european market proximity requirements

jiangsu, china: fully acquired joint venture, serves asian customers

brazil: cable manufacturing

lugoff, south carolina, usa: optical fibre cable manufacturing, baba compliant for us federal programmes

The us plant at lugoff was strategically invested ahead of the us bead broadband funding programme and is directly relevant to stl’s north american market share ambitions. It also provides a natural hedge against us import tariffs - stl can supply us customers locally for projects requiring american-made content.

Customers

stl’s customer base cuts across four distinct buyer types, each with different purchasing logic, switching costs, and relationship dynamics.

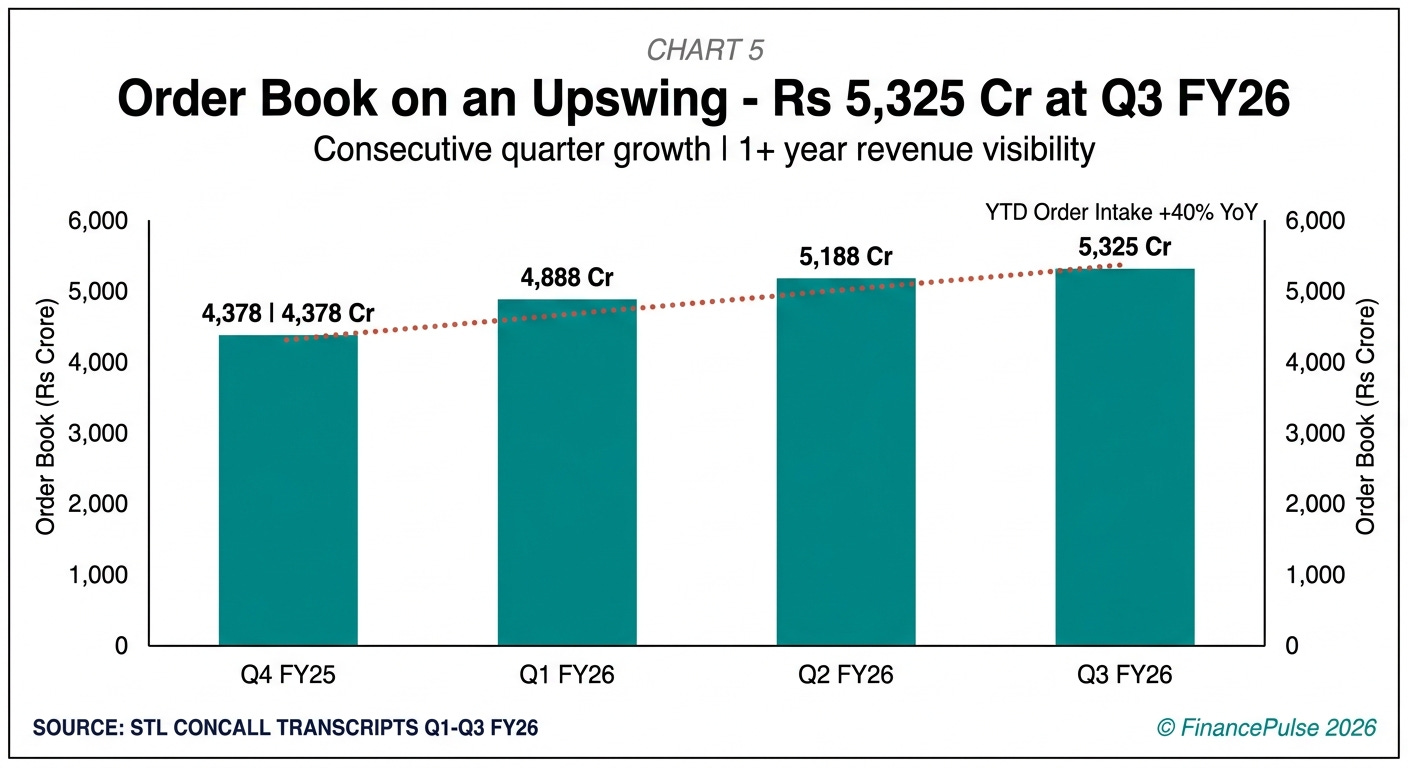

Telecom operators are the largest and most strategically important customers. these are companies like british telecom, vocus (australia), netomnia (uk), archtop fiber (us), connexin (uk), wyre (belgium), and du telecom (uae). They buy optical fibre cables in large volumes to build fibre-to-the-home, 5g fronthaul, and backbone networks. The buying decision sits with the head of network procurement or cto office, and the sales cycle is typically 6-18 months - it involves technical qualification (the fibre must meet itut standards and the operator’s specific network design parameters), commercial negotiation, and often multi-year framework agreements. stl has secured “multi-year supply agreements with leading european operators” and “regained strong order inflows from top-tier us telecom players after a year’s pause”. Switching costs for a contracted operator are moderate - the fibre is fungible once qualified, but switching mid-project creates logistics complexity and risks certification issues.

Hyperscalers and data centre operators are the growth frontier. Companies like aws, microsoft, google, and meta are building ai-optimised data centres at an extraordinary pace. Global dc capex is expected to approach $600 billion by 2027 (per cru data cited by management). Each ai data centre requires substantially more fibre per rack than a conventional cloud facility - gpu clusters need high-bandwidth, low-latency intra-facility connectivity. STL has built a specific portfolio for this segment including the celesta ibr cable and pre-terminated high-density assemblies. Hyperscaler procurement is typically done through a vendor-approved list process, and getting onto that list requires significant qualification effort - once in, volumes are large and relationships tend to be sticky.

Citizen networks / government - before the demerger of invenia, stl had a large presence in bharat net and government broadband programmes. Post-demerger, this work has moved to invenia. However, stl still serves as the optical fibre cable supplier to such projects - the march 2025 rs 2,631 crore bharatnet contract in jammu and kashmir/ladakh was technically awarded to stl networks (the demerged entity) in consortium with dilip buildcon, but stl still supplies the cable. Government segment is characterised by long project timelines, payment delays, and working capital intensity - which is partly why stl chose to separate it.

Enterprise customers for stl digital - these are medium-to-large enterprises in healthcare, communications, life sciences, and manufacturing that need digital transformation programmes. given stl digital’s scale (rs 64 crore quarterly revenue), these are predominantly mid-market accounts rather than global fortune 500 engagements. Two healthcare providers in the middle east were signed on multi-year contracts in q1 fy26.

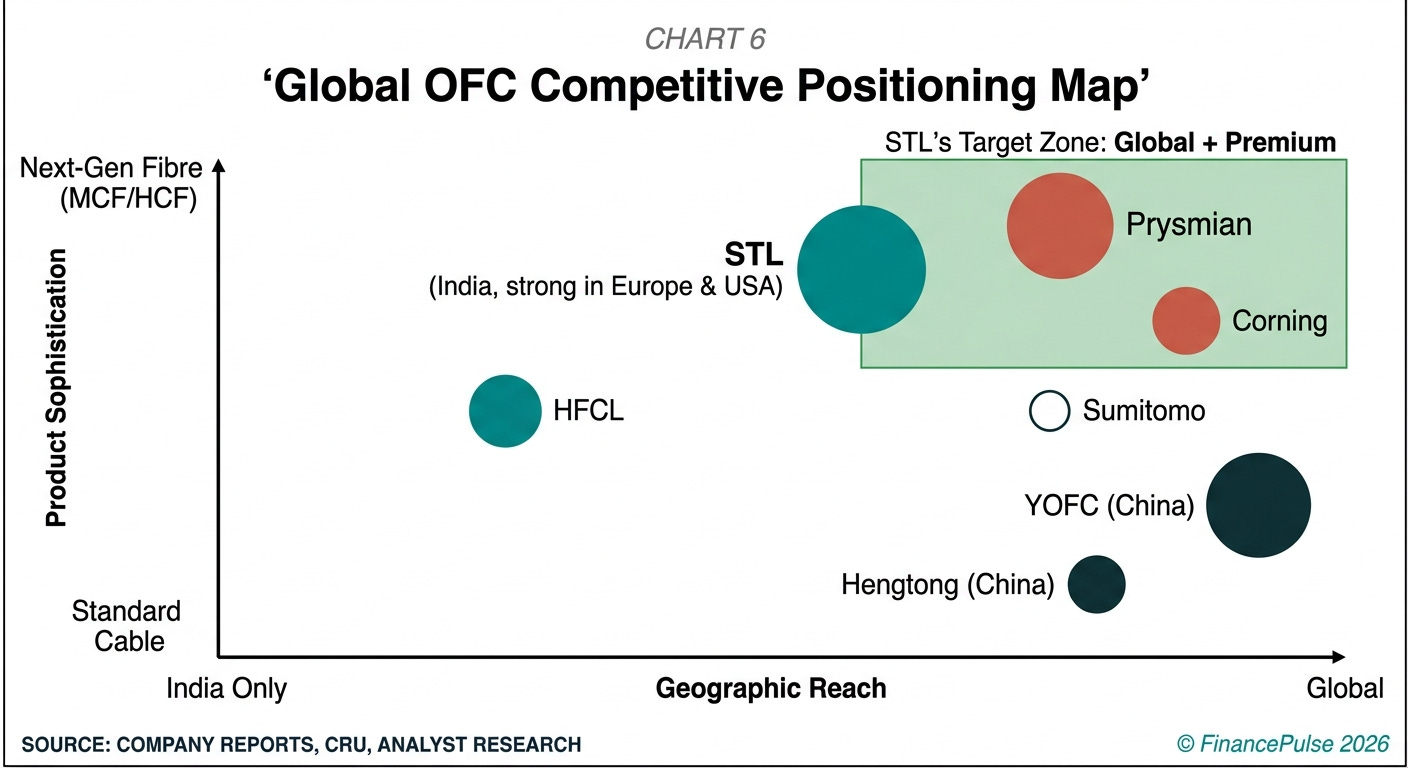

Competitive Landscape

The optical fibre cable market has a specific three-tier structure that is important to understand: at the top sit the chinese manufacturers (yangtze optical fibre / yofc, hengtong, zhongtian), who dominate volume but face increasing trade restrictions in western markets. In the middle sit the western integrated players (prysmian, corning, ofs/furukawa, sumitomo electric). and then there is stl, which competes as the primary indian player with a cost structure anchored in india but a western-qualified product.

Prysmian (italy/usa): the largest fibre cable manufacturer outside china. It has filed a lawsuit against stl’s us subsidiary for trade secrets violation (see risks section). prysmian has a clear market interest in slowing stl’s north american expansion. it has invested heavily in us manufacturing (a $50 million modernisation at claremont, nc and a $56 million palmetto plant in south carolina). It is stl’s most dangerous competitor in the north american market.

Corning (usa): the inventor of modern optical fibre. Corning does not manufacture finished cables but sells optical fibre to cable makers and operates its own cable business. It has a premium positioning and deep relationships with tier-1 north american carriers. STL competes with corning’s cable business on cost.

Sumitomo electric (japan): strong in asia and selectively in europe. Not a primary competitor in stl’s core european market.

HFCL (india): The second-largest indian optical fibre cable manufacturer. hfcl has also backward-integrated into fibre drawing and is a direct competitor for indian telecom operator contracts. However, hfcl does not have stl’s international scale or the italy/usa manufacturing presence.

Yangtze optical fibre (yofc) and Hengtong (china): Massive volume manufacturers whose export pricing creates structural pressure on the market. However, us and european tariffs on chinese optical cable have been increasing, reducing the competitive threat in stl’s two primary western export markets. This is a genuine tailwind for stl.

Growth triggers

North america revenue scaling on bead and hyperscaler demand: Management guided that enterprise and data centre business contributed 20% of ytd fy26 revenues and they “remain on track to scale this to 30% and expect it to be a key growth driver in the medium term”. North america’s revenue share rose from 25% in fy25 to 36% in ytd fy26, driven by data centre connectivity wins and breakthroughs with tier-1 north american telecom customers.

“our enterprise and data center business is gaining traction with 20% revenue contribution in year to date fy26 and we remain on track to scale this to 30% and expect it to be a key growth driver in the medium term.”

- ankit agarwal, managing director (q3 fy26 concall, january 23, 2026)

Utilisation recovery to 70%+ improving ebitda margins toward 18-20% target: stl is currently operating at approximately 50% utilisation on its 50+ million fkm glass/fibre and 42+ million fkm cable capacity. Management has guided that increasing utilisation from 50% to 70% “should improve ebitda margins from 14% to 20%”. The upcycle in global fiber demand starting 2025 is the primary mechanism for this utilisation recovery.

“as demand returns, they aim to increase utilization from 50% to 70%, which should improve ebitda margins from 14% to 20%.”

- ankit agarwal, managing director (q4 fy25 concall, may 2025)

Optical connectivity attach rate expansion: The attach rate (the percentage of cable revenue that includes connectivity hardware) rose from 13% in fy24 to 22% in fy25. Management aims to grow this toward 30%+. Each percentage point of attach rate improvement carries margin expansion because connectivity products are higher-margin than bulk cable. The celesta ibr launch in q2 fy26 is a specific product driving this.

Bead programme us demand commencing in earnest: Management in q3 fy25 (january 2025) guided bead-driven demand to begin in calendar year 2026, with benefits in stl’s q3-q4 fy26. ankit agarwal in q4 fy25: “sterlite expects the bead programme to progress, potentially starting in q4 this year or q1 next year.” north america’s revenue share growth to 36% in ytd fy26 suggests this is materialising. full bead implementation could sustain north american demand through 2030.

India tariff barriers against chinese optical cable: stl management has noted that tariff and non-tariff barriers on chinese optical cable imports have tightened in india, benefiting domestic manufacturers. The government’s preference for domestic supply in bharatnet and 5g-related procurement reinforces this.

Multi-year european supply agreements locking in volume: “we have secured multi-year supply agreements with leading european operators, and regained strong order inflows from top-tier us telecom players”. These multi-year agreements provide revenue visibility and reduce the lumpiness that characterised stl’s order book during the inventory correction.

Hollow core fibre and multiverse mcf as premium product lines: The colt technology services multi-core fibre trial on the london metro network (announced january 22, 2026) and the hollow core fibre hybrid cable launch (march 25, 2026) represent stl’s entry into premium-priced next-generation fibre products. If hyperscalers and tier-1 operators adopt these at scale, the average selling price for stl’s fibre mix improves.

Scenarios & Valuation

Bull case

The global fibre upcycle that CRU is projecting develops into a multi-year super-cycle driven by the convergence of three forces: ai data centre buildout, bead-funded rural broadband in the us, and european fttx programmes. Stl’s order book, which has already crossed rs 5,325 crore with 40% yoy intake growth, accelerates further. North america scales to 40-45% of revenues as tier-1 us telecom carriers commit to multi-year supply agreements and hyperscalers source from stl’s south carolina facility for domestic supply chain security. Utilisation climbs from 50% toward 75-80%, and ebitda margins push toward the guided 18-20% range. The optical connectivity attach rate reaches 30%+ as the celesta ibr cable gains traction in ai data centre deployments. The prysmian litigation is settled or overturned on appeal, removing the contingent liability overhang. STL digital finds its footing in communications-vertical cybersecurity through the securennov platform, growing to rs 400-500 crore in annual revenue. The demerger of invenia has simplified the capital story, and with net debt declining below 2x ebitda, the balance sheet no longer constrains investments.

Base case

Demand in 2025-2026 recovers to historical trend levels rather than a super-cycle. bead provides a steady north american uplift but execution is state-by-state and lumpy. stl’s revenues grow at a mid-teens cagr from fy26 onward, driven by north america and india. Utilisation improves to 60-65% by fy27, pushing ebitda margins to 14-16% - an improvement from the current trough but short of the 18-20% target. The connectivity attach rate recovers to 22-25% as data centre orders ramp. stl digital stays subscale but profitable, contributing a small but growing earnings stream. The prysmian litigation drains capital (either through settlement or eventual payment) but does not threaten the parent’s operational continuity. Net debt trends below 2x ebitda as free cash flow improves on better margins. Europe remains the largest market at 38-40% of revenues. In this scenario, stl is a better business than it was in fy24-fy25, but it has not yet translated its capacity and global footprint into the dominance it has aspired to.

Bear case

The prysmian appeal fails, forcing a rs 810 crore payment through sti that requires capital infusion from the parent. China eases its export controls on germanium, but also resumes aggressive optical cable pricing in global markets as it seeks to capture the ai data centre opportunity. stl’s market share recovery in the ex-china global market does not happen because chinese manufacturers find ways around tariff barriers or europeans source locally. Utilisation plateaus at 55-60% because bead execution in the us is slower than projected and india’s 5g fiberisation pace is disappointing (telcos delay capex due to arpu pressure). Ebitda margins stay in the 10-13% range with no path to the 18-20% target. stl digital continues to consume capital without scale. Debt stays above 2x ebitda. in this scenario, stl remains a structurally important company in global optical infrastructure but with economics that do not justify its capacity investments, and the period of building for growth extends further without a clear payoff horizon.

Thanks for reading!